Pro Tip: Listen to the podcast below and while you’re listening follow along with the charts below. Then, when you’re done, copy the  Scenario

Scenario

Welcome to the Real Estate Financial Planner™ Podcast. I am your host, James Orr. This is Episode 21.

Today we’re going to continue with  Norm and Norma’s

Norm and Norma’s

In the last few episodes, Norm and Norma

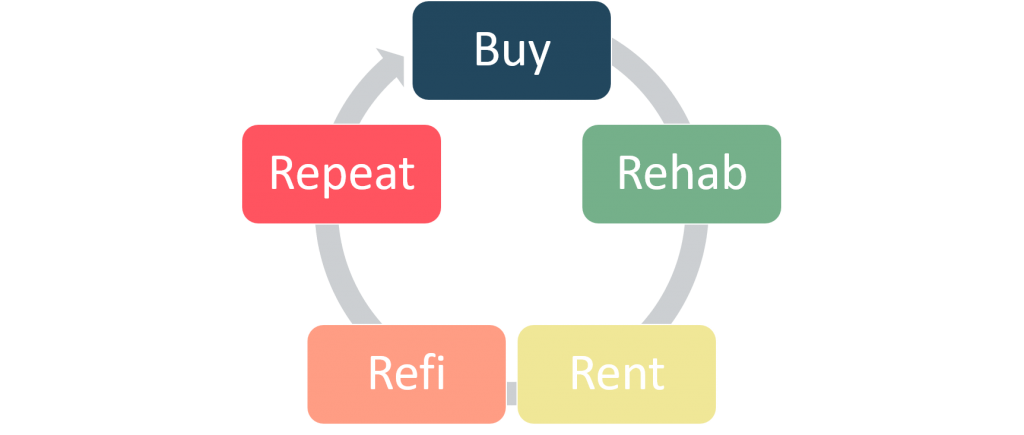

In this episode they’re going to consider the BRRRR method. BRRRR stands for:

- Buy

- Rehab

- Rent

- Refi, and

- Repeat

In other words:

- What if they could find a property that needs work and one where they can buy it at a substantial discount?

- What if they do the work and get a tenant in that property, then refinance the property to leave little or no money in the deal?

- Then, what if they repeat this process until they’ve acquired as many properties as they desire?

Some Assumptions

First, let’s talk about the assumptions we used for Norm and Norma

In order to be able to utilize the BRRRR method they need to find a property that needs work that they can buy at a big enough discount to make the economics work.

Ultimately, the need a big enough discount to be able:

- Buy the property with the costs associated with the temporary financing

- Pay for the rehab to increase the value of the property

- Put a tenant in the property

- Refinance the property with the costs associated with more permanent financing and the holding costs while the did the rehab

In many real estate markets, it is extremely difficult to find these types of deals where you’re able to get a big enough discount and leave nothing in the deal.

It is easier to find these types of deals where you leave some in the deal… what might look like 15% down or 10% down or even 5% down.

With that in mind, we modeled Norm and Norma

So, we’re really comparing 4 variations of the BRRRR method to how it might compare to them utilizing the plain vanilla Nomad™ strategy.

In all cases… whether they’re doing BRRRR or Nomad™ they’re ultimately buying 10 properties.

Don’t Have To Invest Local

In previous episodes when they utilized the Nomad™ real estate investing strategy, in order to owner-occupy the property and get owner-occupant 5% down payment financing, they had to invest locally. They could not Nomad™—unless they were doing Nomad™ by Proxy—in a non-local real estate market.

But, one of the advantages of the BRRRR method is that they do not need to invest in their local real estate market. If they can’t quite find properties that they can buy at a big enough discount to BRRRR them, they could research and become experts at another real estate market where they can find properties at the discounts they need.

Slightly Higher Interest Rates

Since these are non-owner-occupant properties, we’re using a higher interest rate for the loans than what they can get as owner-occupants when Nomading™.

We opted to use the same interest rate they could get if they put 20% down to buy non-owner-occupant investment properties.

However, in the real world, some lenders may add a small premium to your mortgage interest rate if you’re doing a refinance using the BRRRR method. We did not model it this way.

I’d consider this be a less conservative way to model this.

Slightly Worse Rents

Way back in Episode 8 when Norm and Norma

In other words, they were probably trying to find the best cash flowing deal they could that still had a strong probability for long-term appreciation.

By putting cash flow as a top selection criteria they probably could find deals that had better rent to price ratios that gave them maximum cash flow.

However, when trying to find a BRRRR property—because the ability to find a property where you can buy it and leave minimal in the deal is often the most important characteristic—often the cash flow and long-term appreciation criteria takes a backseat to whether they can get the property at a big enough discount or not.

In other words: “can I leave little or nothing in the deal” becomes more important than “will this have amazing cash flow”.

With that being said, when Norm and Norma

I’d consider this be a less conservative way to model this.

Left in the Deal

Out of an abundance of clarity, when we say they left nothing or 5% or 10% or 15% of the ARV in the deal when using the BRRRR method, I mean that’s the total amount left in after all the costs to acquire the property to begin with.

That includes the closing costs to buy the property and the costs to get the financing for the initial purchase.

Plus, all the costs for any repairs that the property needs.

Plus, all the holding costs for the property while they are doing the repairs, finding a tenant and refinancing the property into the long-term, permanent financing.

Plus, the costs to get the long-term, permanent financing.

So, really… the amount they left in the deal is the total amount it cost Norm and Norma

Timing

For our modeling, we also assume that the time we say they bought the property is really the time they put long-term, permanent financing on it. So, really, they bought it… probably several months earlier, did the rehab, put a tenant in and refinanced the property.

It might be much harder and take a lot more time to find a deal that fits their investment criteria when using BRRRR. But, we assume they’ve got plenty of deal flow and their limitation for buying the next property is only limited by how much they have saved and their debt-to-income for qualifying for the loans.

Extra Work

Doing Nomad where you need to move into 10 properties is a lot of work.

But, finding BRRRR properties, overseeing or doing the rehab yourself to save money and financing each property twice is a lot of work too.

It will ultimately be up to Norm and Norma

Financial Independence

Now that we’ve got some of the assumptions out of the way, how does using the BRRRR method compare to Nomading™ in terms of achieving financial independence?

Well, I’ll get to that in a moment, but might I recommend a little mental exercise first.

If you’re able to buy essentially the same properties you’re Nomading™ into, but get them for a 20% discount or a 15% discount or a 10% discount or a 5% discount… isn’t that likely to be better than buying the same properties and not getting a discount?

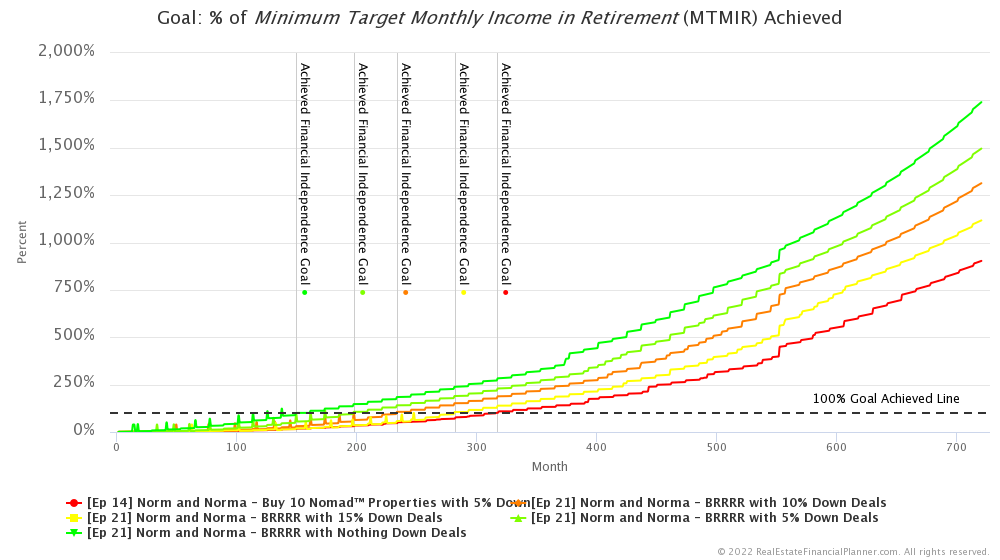

Yes… well, that’s what’s happening here. We have Norm and Norma

So, we would expect these to perform better than just doing traditional Nomad™. The real question is: how much better is it to do this extra work?

It turns out that it is significantly better.

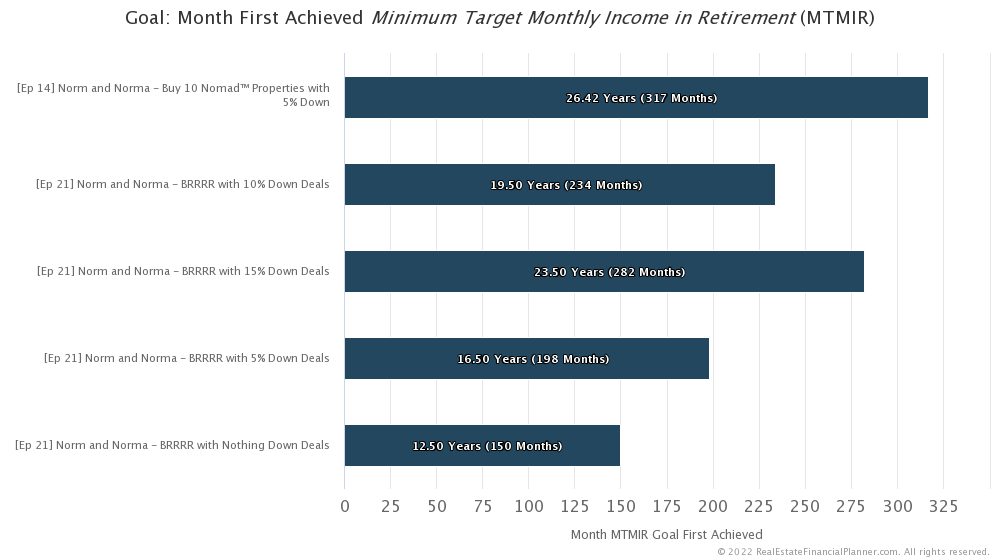

If Norm and Norma

- But, buying BRRRR properties and leaving 15% in the deal is about 3 years faster than Nomading™.

- Buying BRRRR properties and leaving 10% in the deal is about 7 years faster than Nomading™.

- Leaving only 5% in the deal is about 10 years faster than Nomading™.

- And, if they’re fortunate enough to find BRRRR deals that they can buy and leave no money in the deal, that’s about 14 years faster than Nomading™. If they can find 10 nothing down BRRRR deals, they can be financially independent in as little as 12.5 years.

In addition, as you might have expected, the less they have to leave in the deal, the higher their standard of living can be as well.

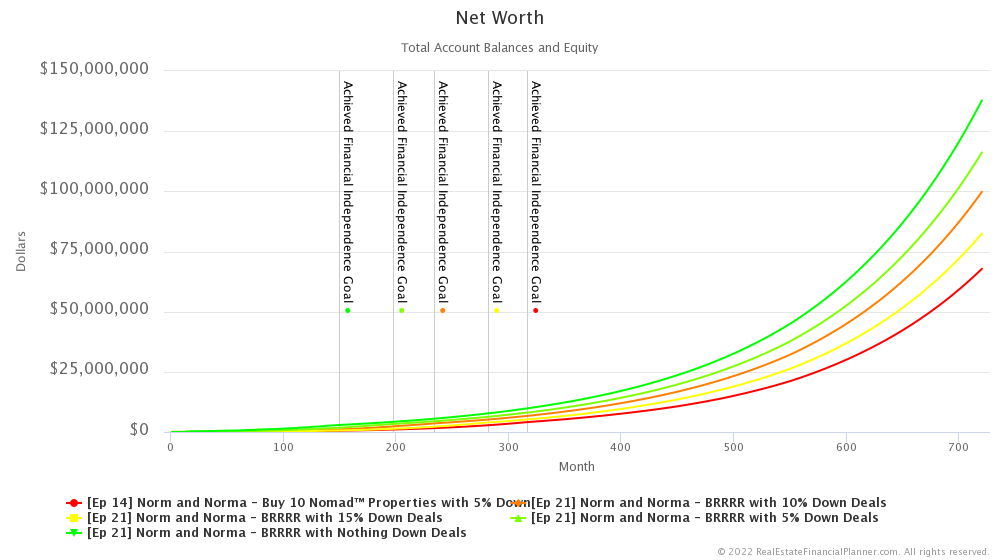

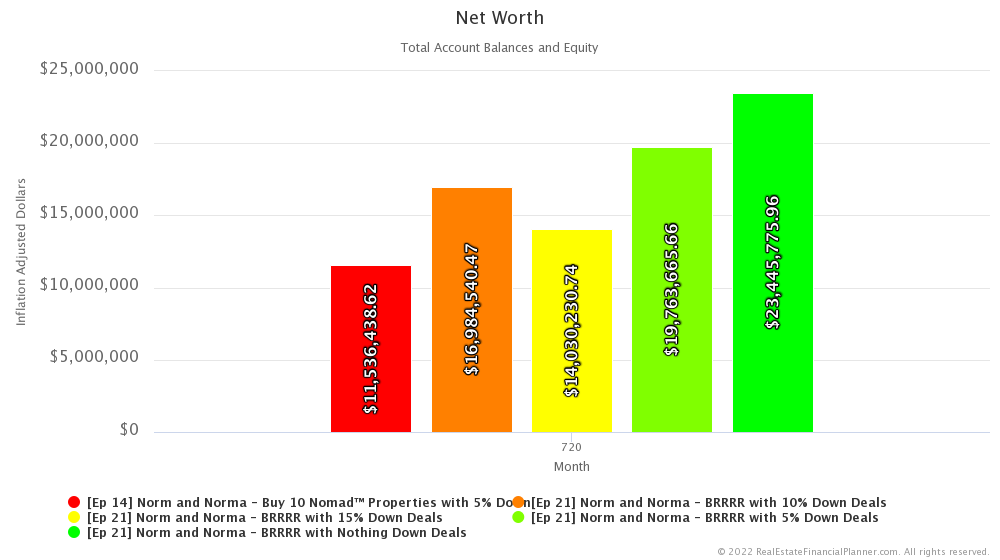

Net Worth

Let’s switch gears now and talk about Net Worth.

The less they put down the higher their net worth too.

If we look at their final net worth at the end of the modeling in year 60… that’s month 720… and if we adjust back to today’s dollars:

- Their net worth if they do traditional Nomad™ is about $11.5 million.

- Their net worth if they BRRRR and they need to leave 15% in the deal is about $2.5 million more… or about $14 million total.

- If they leave 10% in their BRRRR deals, it is about $5.5 million more than Nomading™ with about $17 million.

- If they find amazing BRRRR deals that only require leaving 5% in them, their net worth is about $19.75 million or about $8.25 million more than Nomading™.

- And, if they’re able to find the best BRRRR deals where they leave nothing in them, they have a net worth of about $23.5 million or more than double than Nomading™. That’s about $12 million dollars more.

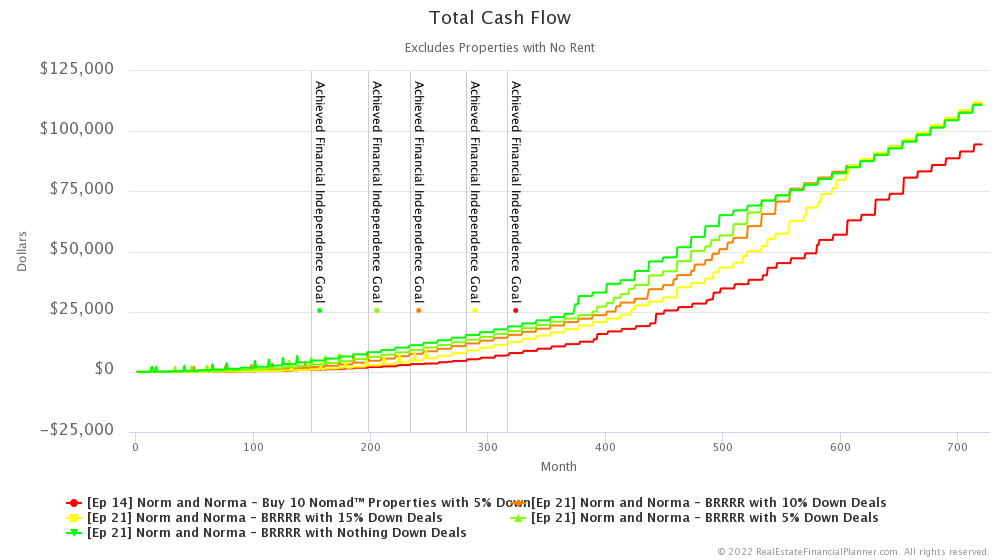

Cash Flow

But, as I like to say: net worth isn’t everything. What about cash flow?

As you’d expect, of the 5 scenarios we’re comparing, Nomad™ has the worst cash flow.

You tend to get better overall cash flow with the less you leave in the deal when doing the BRRRR method.

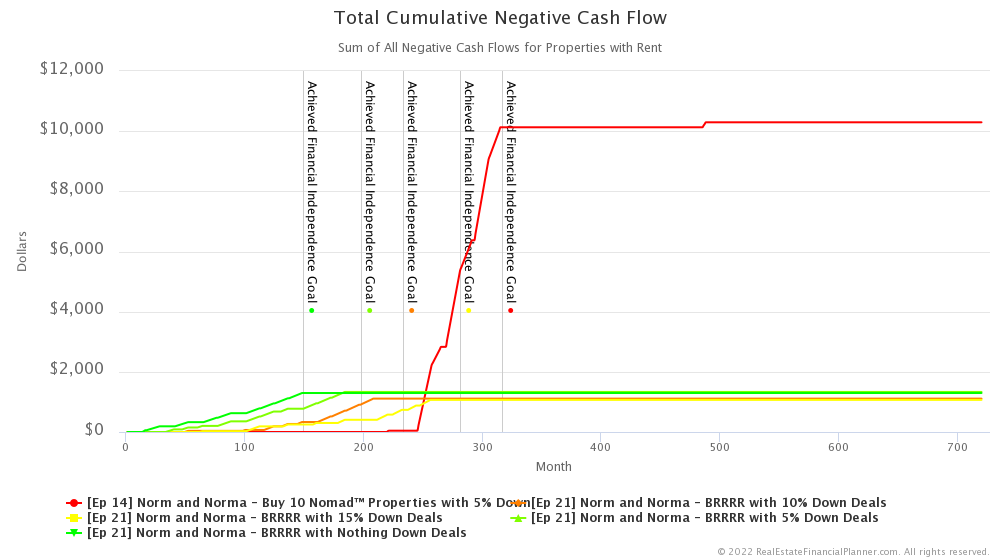

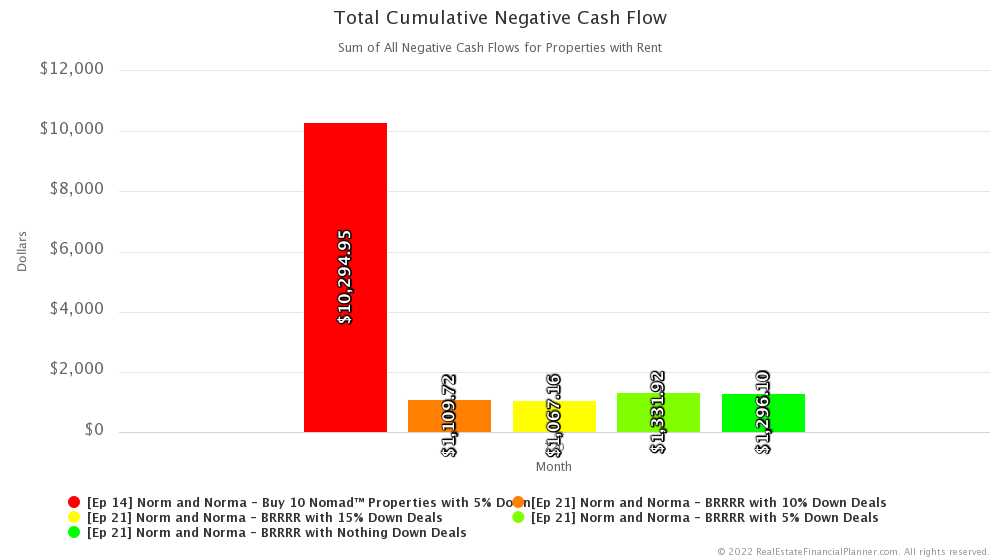

Negative Cash Flow

You’re more likely to have some negative cash flow and more of it when Nomading™ too.

In fact, with our modeling, the most Norm and Norma

That’s a lot less than the over $10,000 total for all properties over the entire 60-year modeling period when doing Nomad™.

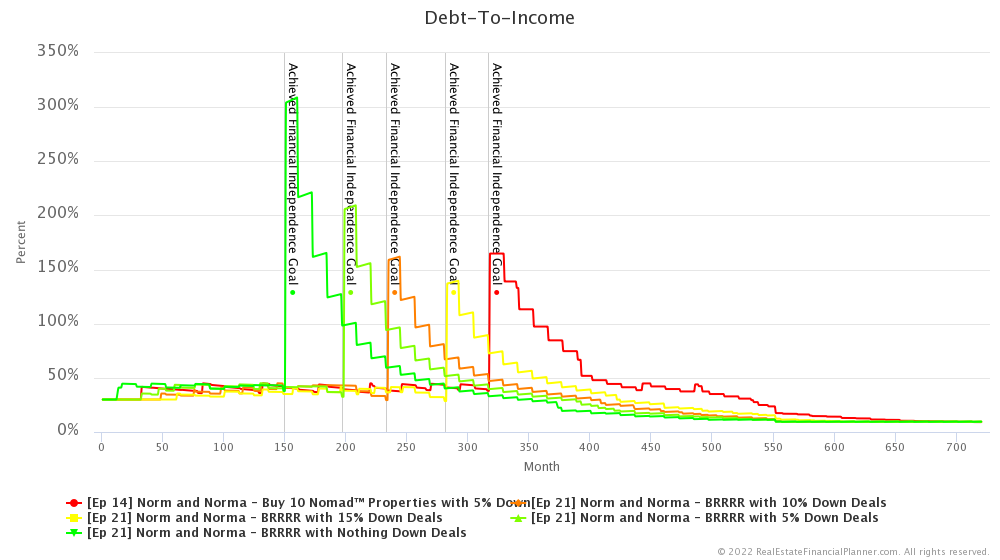

Debt-To-Income

Let’s finish up by looking at a few measures of risk and let’s start with debt-to-income which we sometimes abbreviate as DTI.

If we take the average of the debt-to-income for the entire 60-year modeling period:

- Buying 10 Nomad™ properties with 5% down gives them an average DTI of 40%.

- BRRRR with leaving nothing in the deals is the next highest risk in terms of DTI at about 39%.

- Then, BRRRR with 5% left in the deal gives an average DTI of 34%.

- BRRRR with 10% left in the deals is slightly less risky with just 32% average DTI.

- And, finally, BRRRR with leaving 15% in the deal has the same low DTI of 32% on average.

In general, Nomad™ is slightly riskier than all the BRRRR scenarios, but the more they leave in the deal, the lower their risk is in terms of debt-to-income.

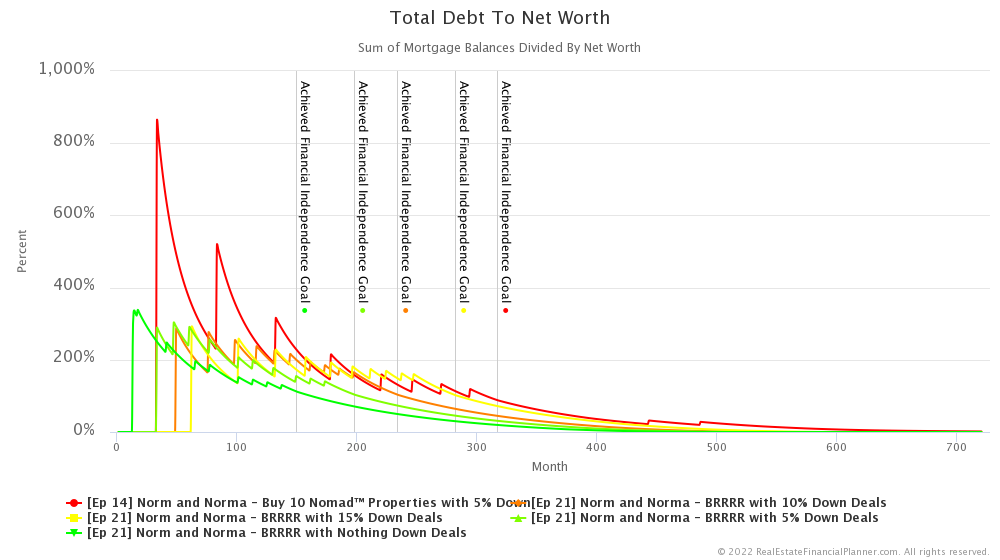

Total Debt to Net Worth

Another way to measure risk is to look at their total debt compared to their total net worth. We call this total debt to net worth.

If we take the average total debt to net worth for the entire 60-year modeling period:

- Buying Nomad™ properties with 5% down payments has the highest risk with this measure at 104%.

- The next highest, but significantly lower than Nomading™ is doing BRRRR and leaving 15% in the deal at an average total debt to net worth of 65%.

- As we leave less in the BRRRR deal the risk goes down. For example, with 10% left in the BRRRR deal, the risk is 61% on average for the entire 60-year period.

- For 5% left in the BRRRR deal, it is 56%.

- And, if they’re able to find deals where they get all their money back out and leave nothing in the BRRRR deal, it is just 49% for total debt to net worth.

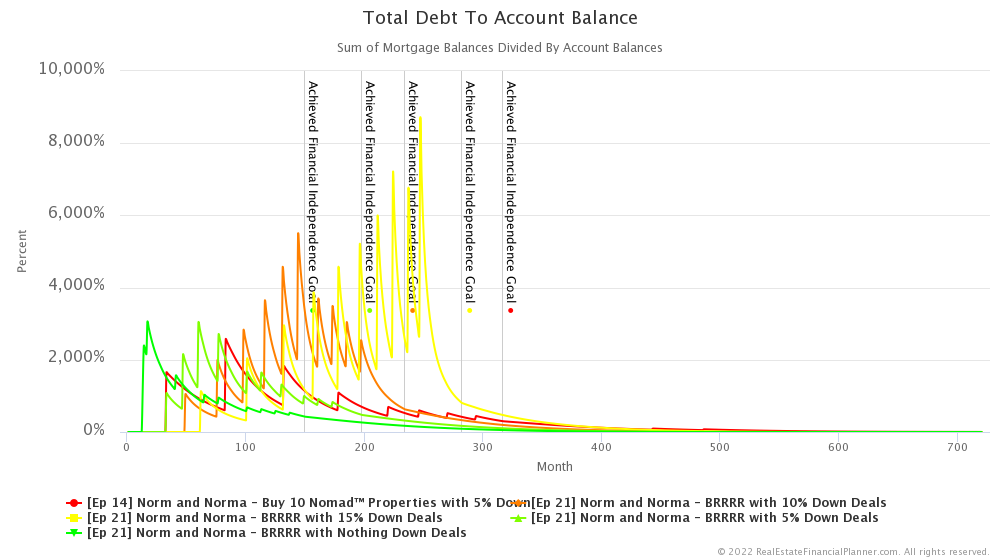

Total Debt to Account Balance

Another way to measure risk is to measure how much debt they have compared to their liquid net worth. What we might call total debt to account balance.

If we look at the average total debt to account balance for the entire 60-year modeling period, the riskiest is to do BRRRR and leave 15% in the deal.

That has an average total debt to account balance of 704%.

The next riskiest is to leave 10% in their BRRRR deals. That has an average total debt to account balance of 536%.

The third riskiest is to Nomad™. That has an average total debt to account balance of 381%.

Then, 5% left in the BRRRR deals… that measures 331%.

And finally, the least risky… at least in terms of total debt to account balance is to leave nothing in your BRRRR deals and that has an average total debt to account balance of a mere 238%.

Conclusion

In conclusion, whenever you’re able to buy the same price and rent property and get them at a discount—sometimes a very significant discount—the numbers are going to look better than buying the same properties, at full price with just 5% down payment.

And, that was true when Norm and Norma

They can achieve financial independence faster with a higher net worth and, for the most part, with less risk.

They must ultimately decide if they’re willing and able to put in the time and energy to find enough deeply discounted deals to be able to implement the BRRRR method for their own investing strategy.

Next Episode

It does beg the question though, if they’re willing to go through the effort to find these deeply discounted properties—properties that might not be ideal properties to hold in their rental portfolio long-term—maybe they should consider buying them, fixing them up and reselling them.

Then, with the proceeds from the flips maybe they invest in stocks or maybe they buy rentals.

In the next episode, Norm and Norma

Also, be sure to check out the Advanced Real Estate Financial Planner™ Podcast to see how having variable property appreciation rates and rent appreciation rates, variable mortgage interest rates, variable inflation rate and variable stock market rates of return impacts Norm and Norma

I hope you have enjoyed this episode about Norm and Norma

Get unprecedented insight into Norm Norma’s Scenario with dozens of detailed, interactive charts.

Compare traditional Nomading™ to four variations of the BRRRR Method of real estate investing:

- Nomading™ to BRRRR with Nothing Down

- Nomading™ to BRRRR with 5% Left In Deal

- Nomading™ to BRRRR with 10% Left In Deal

- Nomading™ to BRRRR with 15% Left In Deal

Compare Nomading™ to all 4 variations of the BRRRR Method. This can be a little cluttered showing all 5 on the same charts.

Inside the Numbers

Watch the Inside the Numbers video to see exactly how we set up their Scenario

Nomad™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 14 Norm and Norma - Buy 10 Nomad™ Properties with 5% Down with 2  Accounts, 1

Accounts, 1  Property, and 6

Property, and 6  Rules.

Rules.

Or, read the detailed, computer-generated, narrated  Blueprint™

Blueprint™

BRRRR Method Leaving Nothing in the Deal

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 21 Norm and Norma - BRRRR with Nothing Down Deals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

BRRRR Method Leaving 5% in the Deal

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 21 Norm and Norma - BRRRR with 5% Down Deals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

BRRRR Method Leaving 10% in the Deal

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 21 Norm and Norma - BRRRR with 10% Down Deals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

BRRRR Method Leaving 15% in the Deal

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 21 Norm and Norma - BRRRR with 15% Down Deals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Podcast Episodes

The following are the podcast episodes for variations of Norm Norma’s

More posts: Norm Episode