Pro Tip: Listen to the podcast below and while you’re listening follow along with the charts below. Then, when you’re done, copy the  Scenario

Scenario

Welcome to the Real Estate Financial Planner™ Podcast. I am your host, James Orr. This is Episode 12.

Today we’re going to continue with  Norm and Norma’s

Norm and Norma’s

But before we do that I have some good news.

The famous statistician George Box said:

“All models are wrong, but some are useful.”

And, that’s been true with all models done by financial planning software. No model can truly account for EVERYTHING… but they can still be useful for us and help us make better decisions.

Even though we do some pretty sophisticated modeling with the Real Estate Financial Planner™ software, they’re still wrong. They don’t *perfectly* model everything… two big examples are taxes or debts other than mortgages. But, over time we do improve the software and the modeling it does and that’s the good news.

Over the last week we made an improvement to how we calculate debt-to-income for people that are renting. Before this update, we did not include the rent they were paying for their own place to live as an expense so the DTI for renters was showing up as lower than it should have been.

Now it does include rent in the calculation making the model even better than it was before.

Since Norm and Norma

Also, since debt-to-income was used to determine if Norm and Norma

So, if you’re looking at previous episodes and the numbers don’t match the new numbers, that’s why.

We will continue to make improvements to the Real Estate Financial Planner™ software to make our models better over time. But, for now, back to Norm and Norma

Short-Term Rentals

In this episode, Episode 12, Norm and Norm have gone through our workshop on How to Improve Cash Flow and latched on to the possibility of doing short-term rentals instead of traditional year-long leases.

If instead of focusing on buying properties that would make great long-term rentals, what if they instead decided to try to find properties that would make great short-term rentals?

What if they could get more rent from their properties each month? Would that speed up how quickly they could be financially independent? And, if so, by how much?

And, by doing a short-term rental, will the expenses of operating their rental go up? And how will that impact their net cash flow and their ability to achieve financial independence?

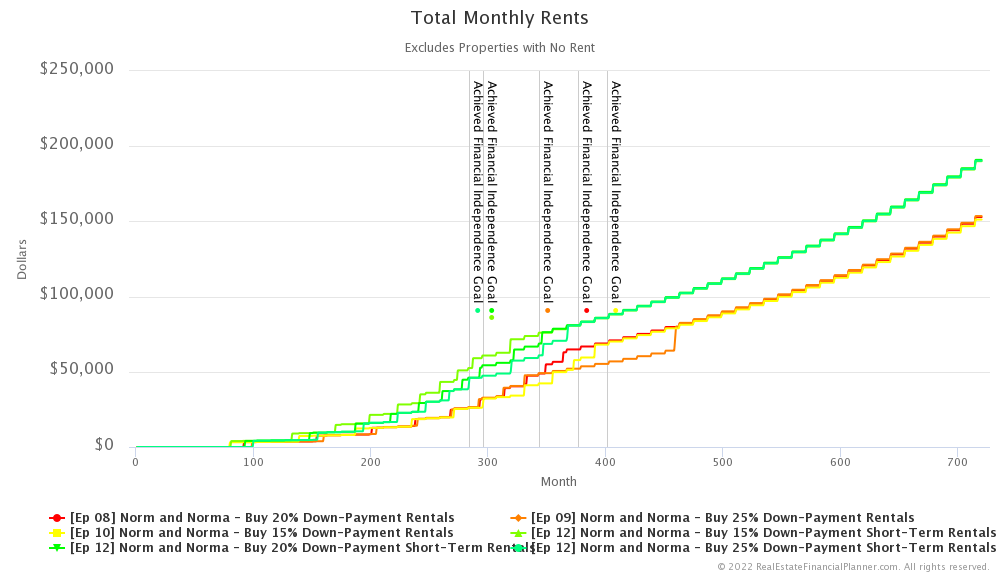

More Rents and More Expenses

For our modeling, we assumed that by converting from a long-term rental to a short-term or vacation rental they’re able to go from averaging $2,600 per month in rent at the start to earning $650 more per month in rent… a total of $3,250 per month in rent on average.

We opted not to model irregular rents throughout the year… in other words we did not show rents were higher based on peak short-term rental seasons in their market… instead we opted to use an average for the year. In the real world… depending on their market and their short-term rental strategy… they may see some months perform much, much better than other months and so their rental income may be irregular.

In addition to more rents, we’ve also increased the maintenance expenses from 10% of gross rents for long-term rentals to 20% of gross rents for short-term rentals.

So, the extra $650 per month in rent as a short-term rental is not just all extra profit.

Unrealistic Expectations

Now, as soon as I told you my assumptions, you immediately thought one or more of the following thoughts:

- “I could do better than that with a short-term rental in my market and my marketing skills?”

- Or, “I am not getting that much extra rent? An extra $650 per month seems unreasonably optimistic.”

- Or, “Pffttt… going from 10% in maintenance to 20% in maintenance is not realistic… it should be much higher.”

- Or, “Wow… I am not paying that much more in maintenance… why did he penalize them so much?”

- Or, “What about the cost to setup the property as a short-term rental which you totally ignored James?”

- Or, “What about the extra risk that the HOA, city, county or whatever will disallow short-term rentals?”

- Or, any number of other comments about how my assumptions are either too good to be true or too bad to be true.

I get it. It is hard to come up with reasonable assumptions that apply to everyone, but that’s why you can copy any of these Scenarios for Norm and Norma

Don’t like the $3,250 per month in rent I used… change it… make it more or less… whatever is appropriate for you and your market and situation.

Don’t like the 20% maintenance number I used… change it… make it more or less… again… whatever is appropriate for you and your market situation.

For this episode, this is what I assumed Norm and Norma

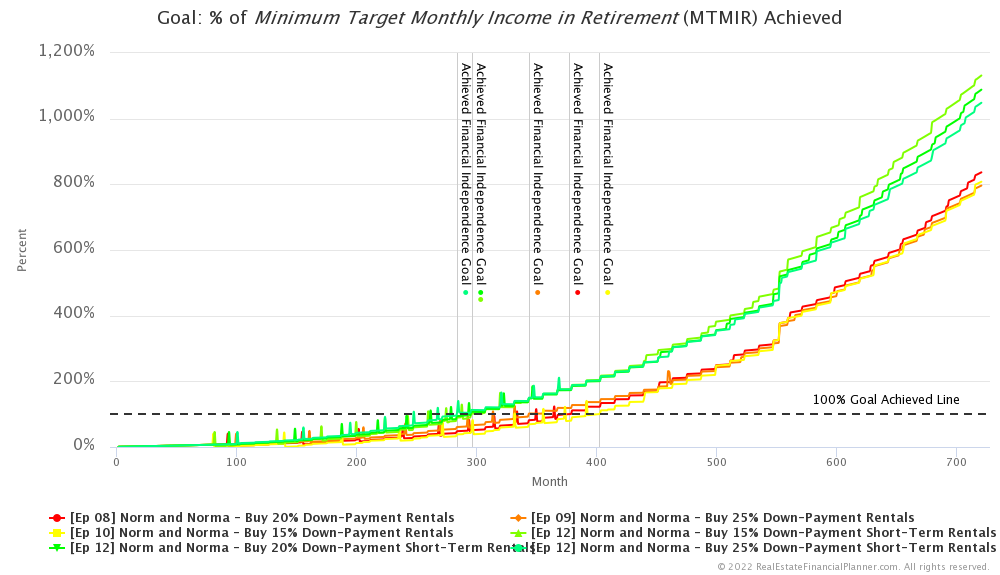

Financial Independence

So, how does Norm and Norma

In each of these scenarios, Norm and Norma

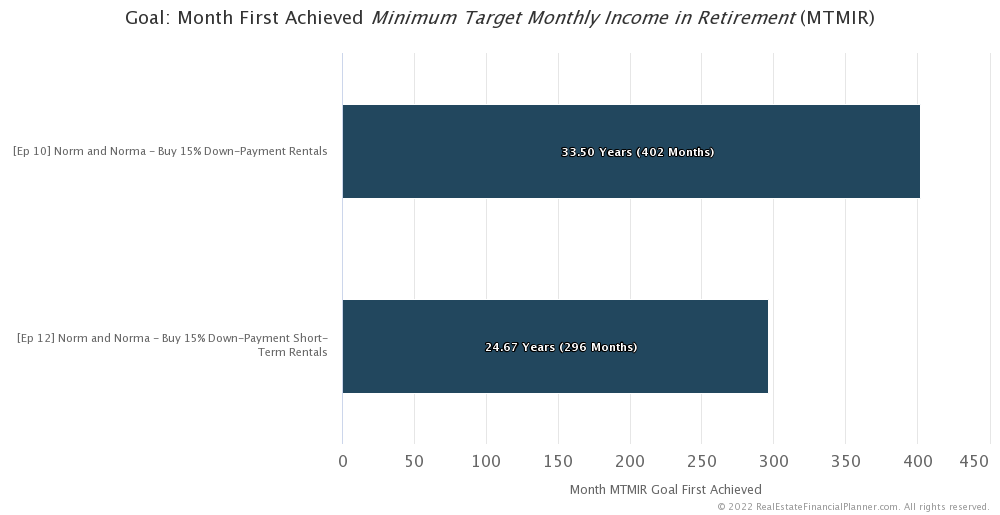

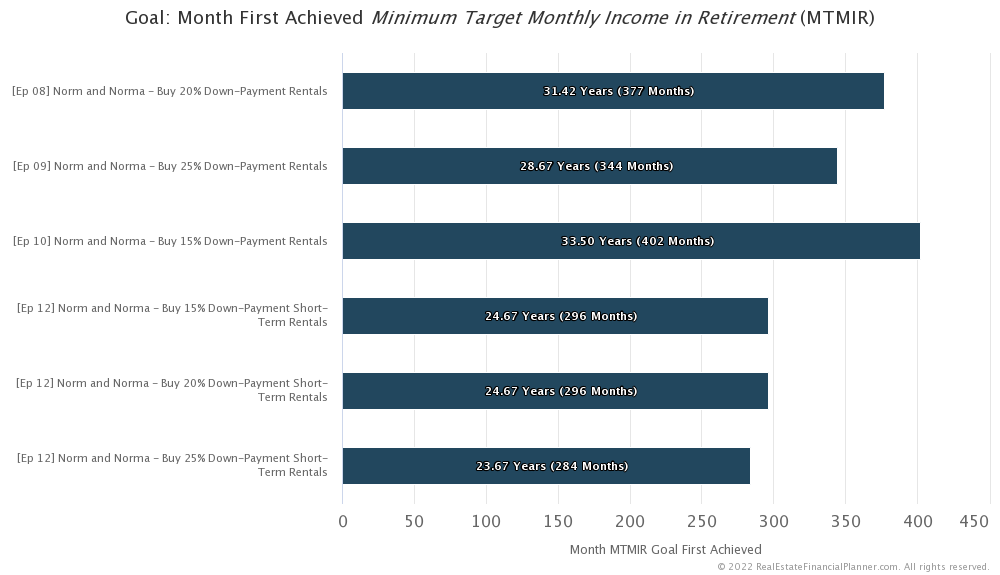

If Norm and Norma

So, that’s them putting 15% down and paying private mortgage insurance.

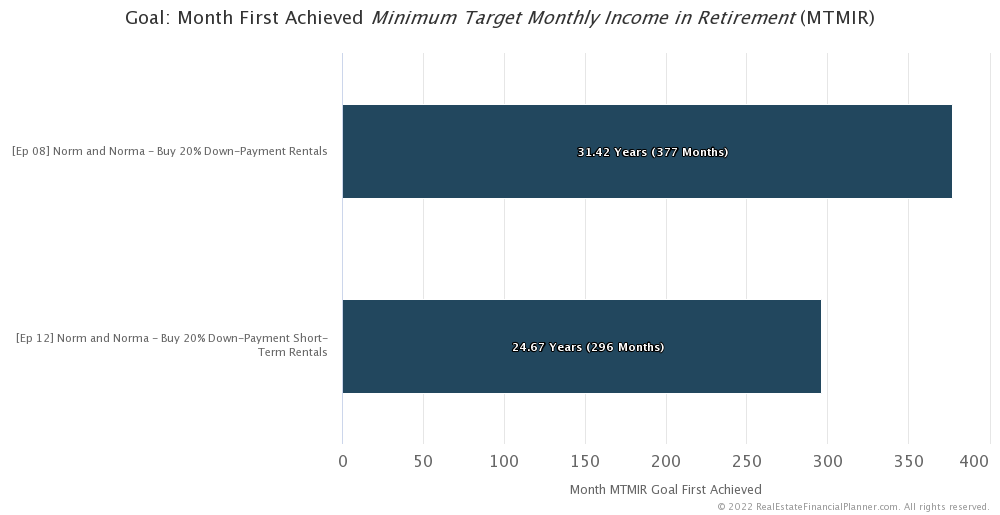

What if they opt to put 20% down?

If they put 20% down, it is 6.75 years faster for them to do short-term rentals than to do long-term rentals.

It would take them 31.42 years to be financially independent with 20% down payments and long-term rentals compared to 24.67 years with 20% down payments buying short-term rentals.

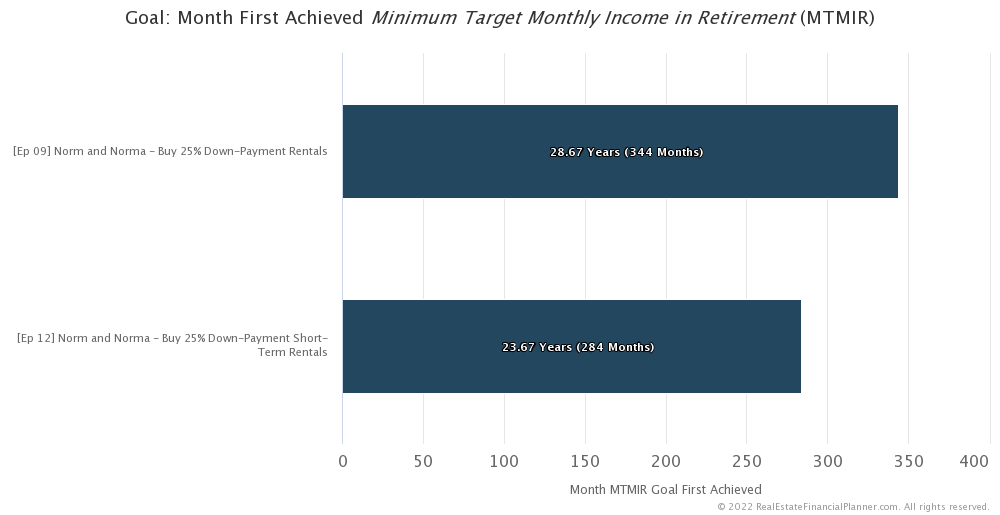

What if they put 25% down to reduce the cost of getting the loan with fewer points, getting a better interest rate and borrowing less?

If they put 25% down it would be 5 years faster to do short-term rentals over long-term rentals.

Regardless of down payment percentage, it is faster for them to do short-term rentals than long-term rentals.

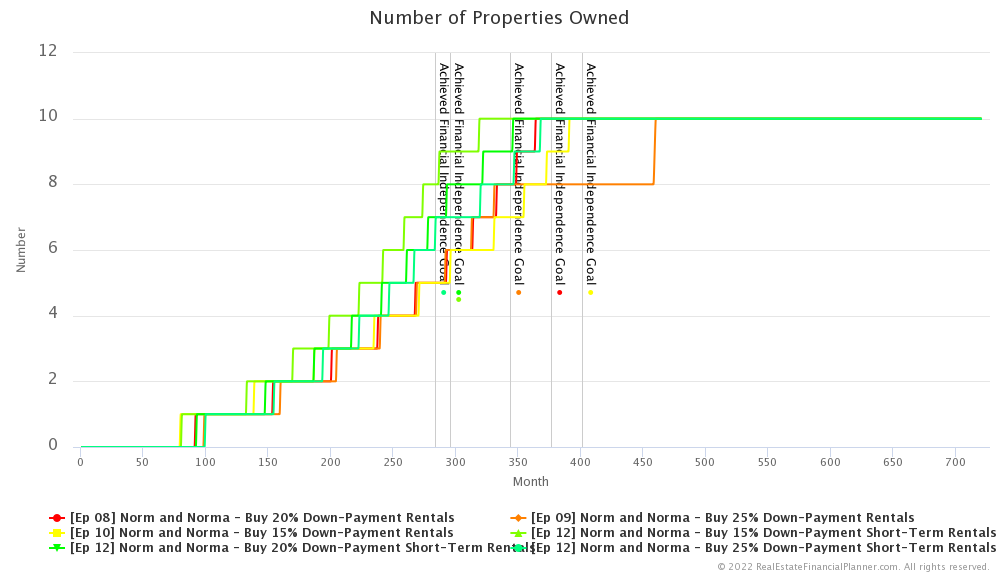

Buying Properties

Let’s talk about buying properties.

When you have more income coming in from properties you own you can buy the next property faster. That’s what happens when they buy short-term rentals… they trade doing a little more work in managing the property in exchange for a little more income from the property.

But why does getting more income allow you to buy the next property faster?

Well, for one, you can save up down payments a little faster.

And, secondly, your debt-to-income is a little better. So, if you were limited by debt-to-income you will qualify for the next loan sooner (and maybe with a slightly better interest rate in some situations).

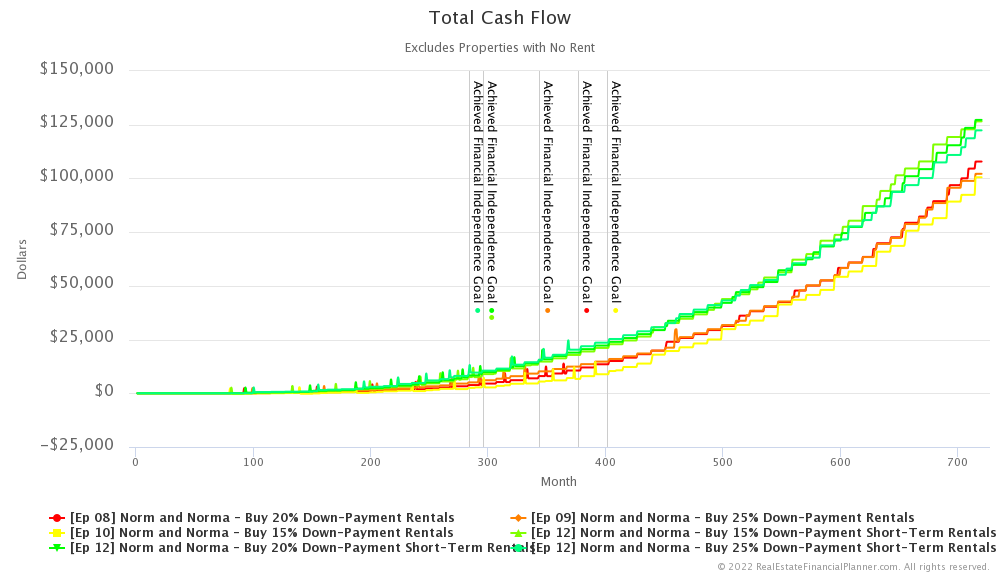

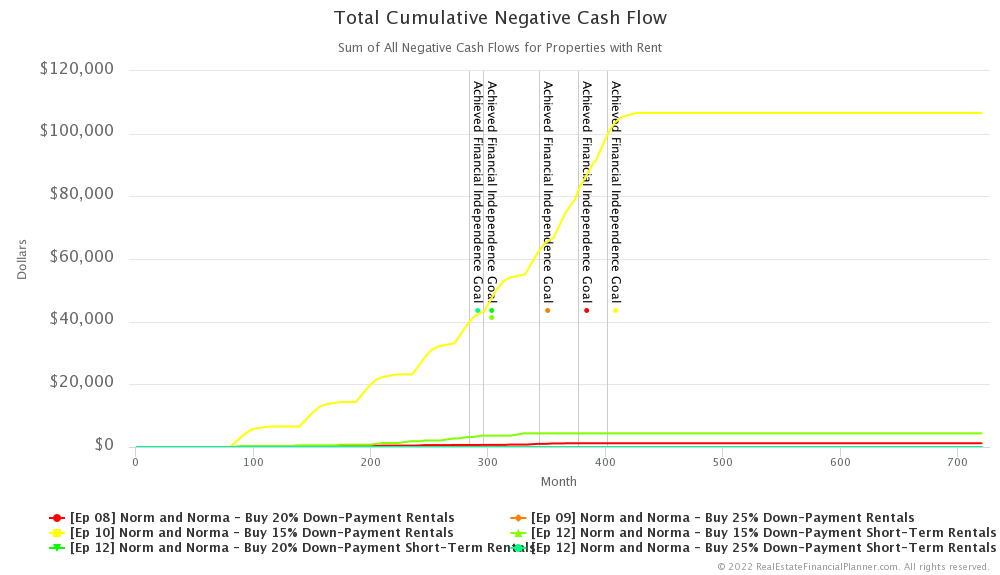

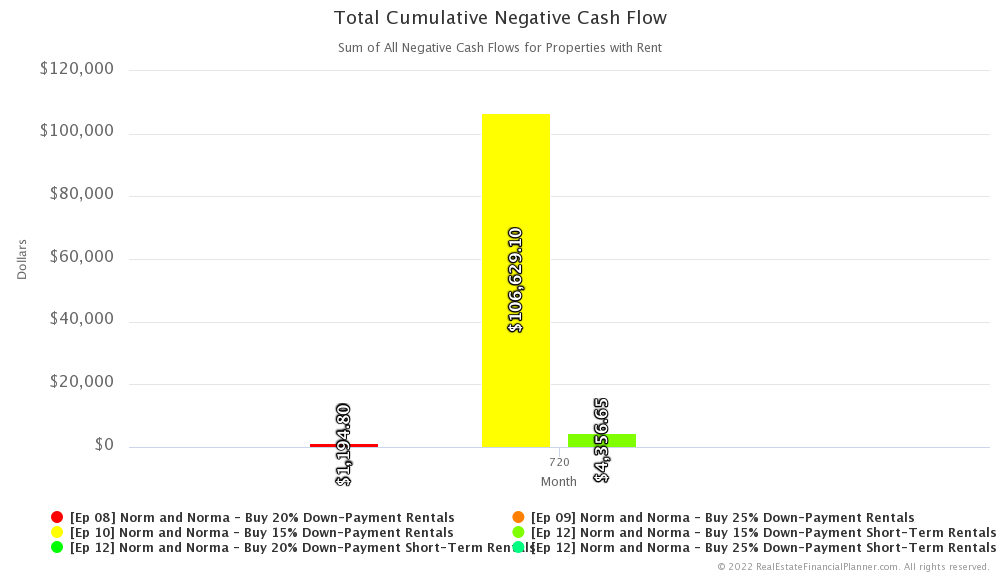

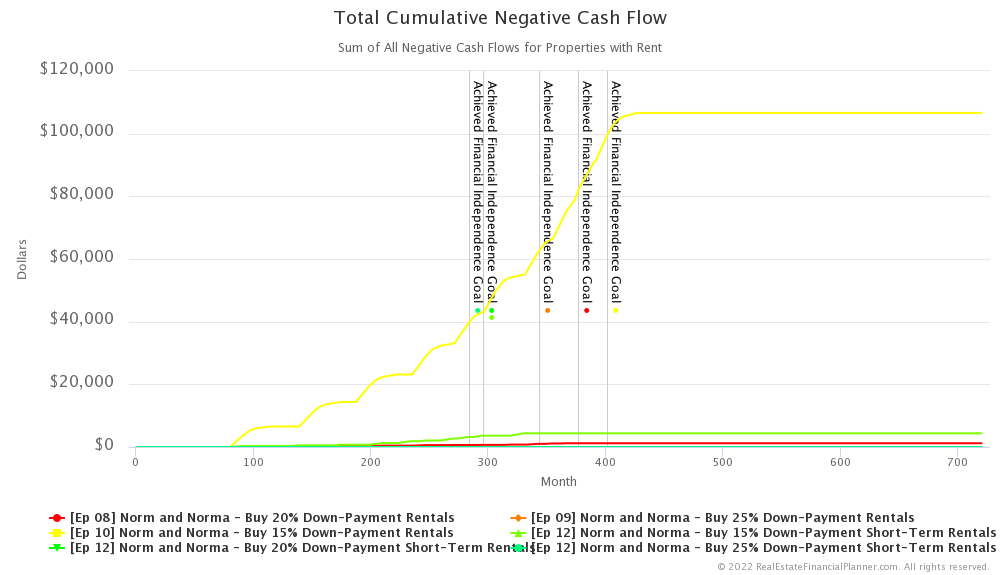

Negative Cash Flow

What about negative cash flow?

Well, putting 15% down… even with the higher rent of doing short-term rentals results in a small amount of deferred down payment… also know as negative cash flow. This is true whether they do short-term rentals or long-term rentals… although it is less if they do the short-term rentals.

If they put 20% down, they’d have a very small amount of negative cash flow… about $1,200 total for all properties across the entire 60-year modeling period… and only when they did long-term rentals. We don’t anticipate any negative cash flow with 20% down if they did short-term rentals.

And neither of the 25% down payment scenarios… short-term or long-term… have negative cash flow at all.

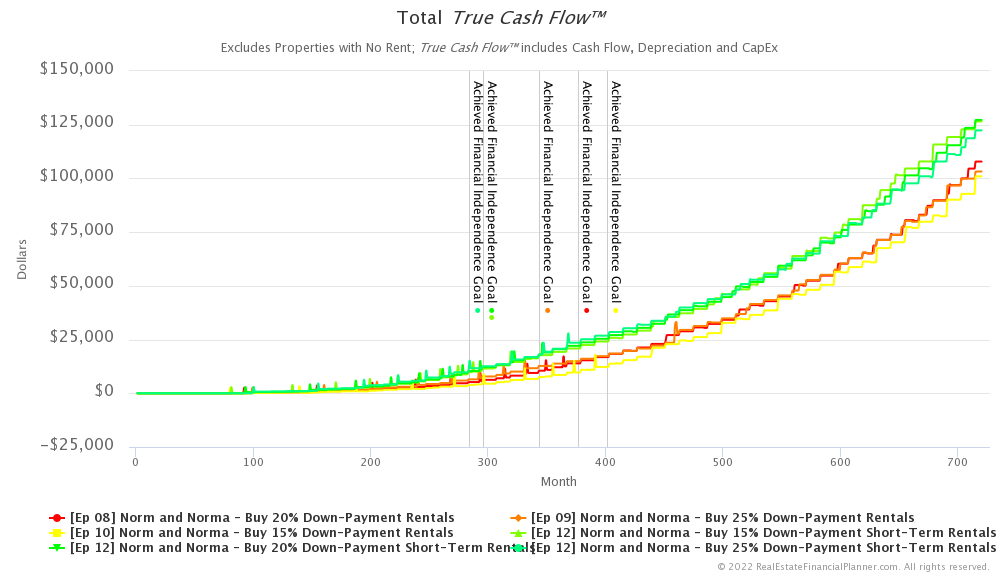

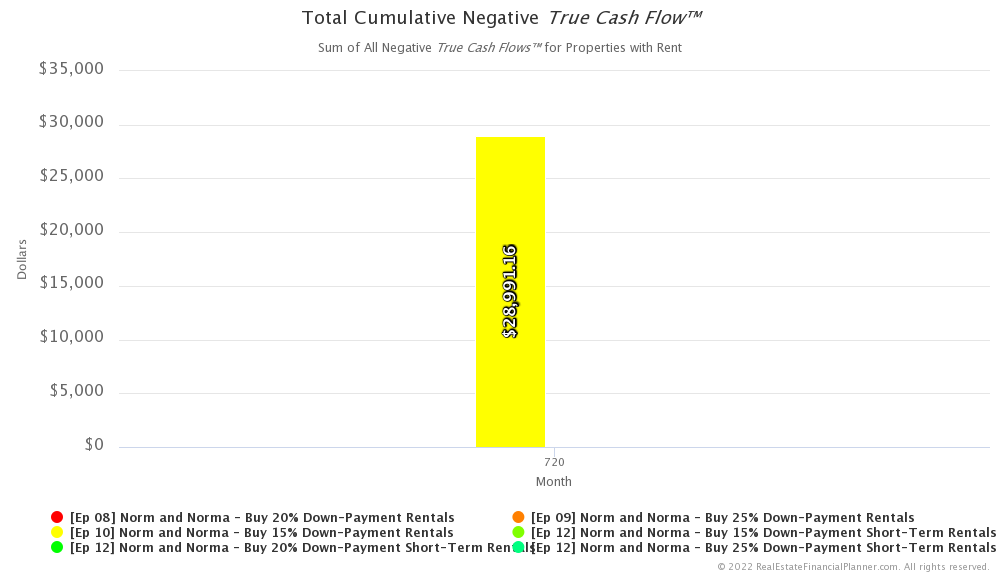

True Cash Flow™

True Cash Flow™ is cash flow plus any Cash Flow from Depreciation™… which are the tax benefits received from owning rental properties at their estimated tax rate.

Since it includes the benefit from depreciation it can offset some… if not all of the negative cash flow… they might experience.

If we look at the cumulative negative True Cash Flow™ that includes the tax benefits of depreciation, they only experience negative cash flow with long-term rentals putting 15% down. All the short-term rental scenarios as well as the long-term rental scenarios with 20% and 25% down do not have any negative True Cash Flow™.

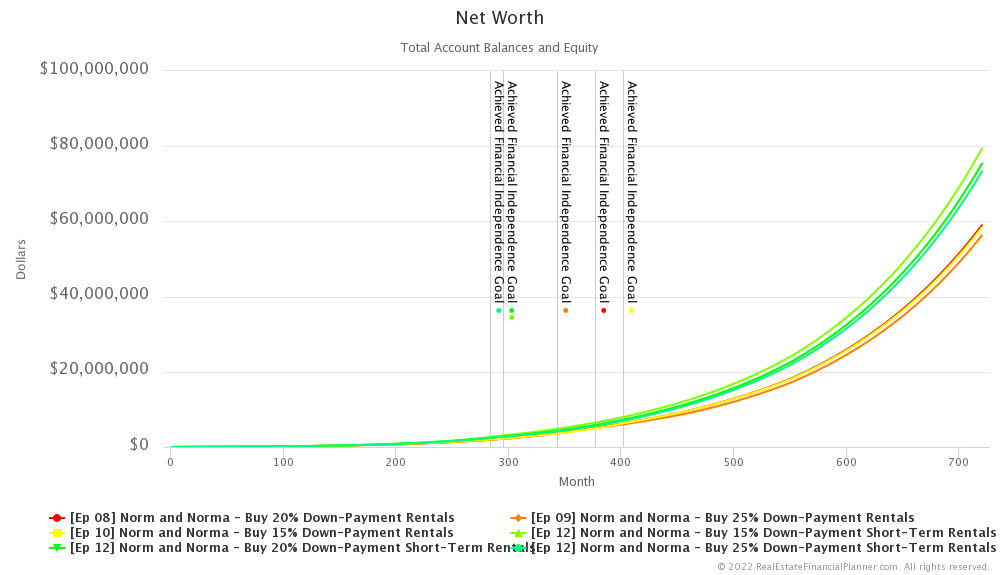

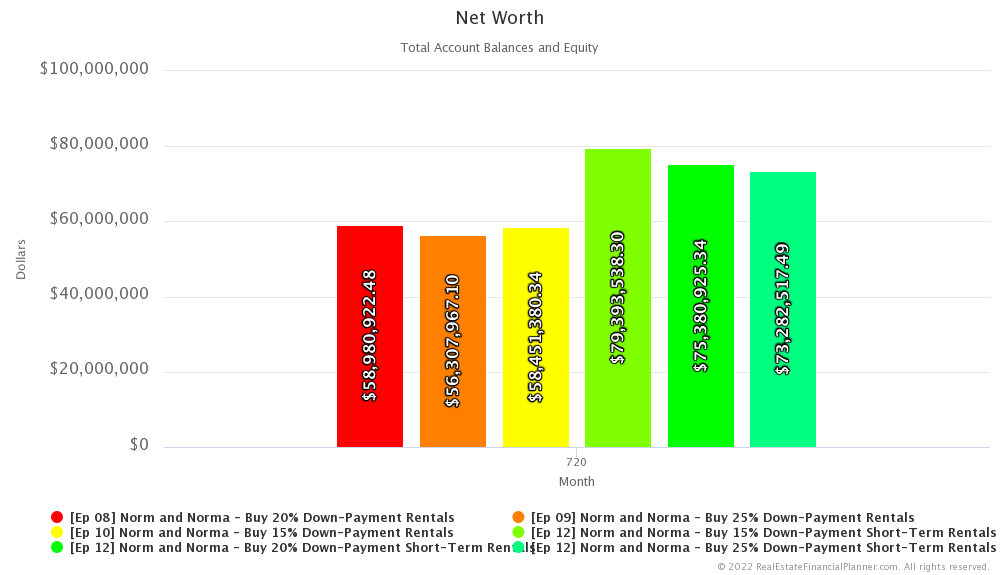

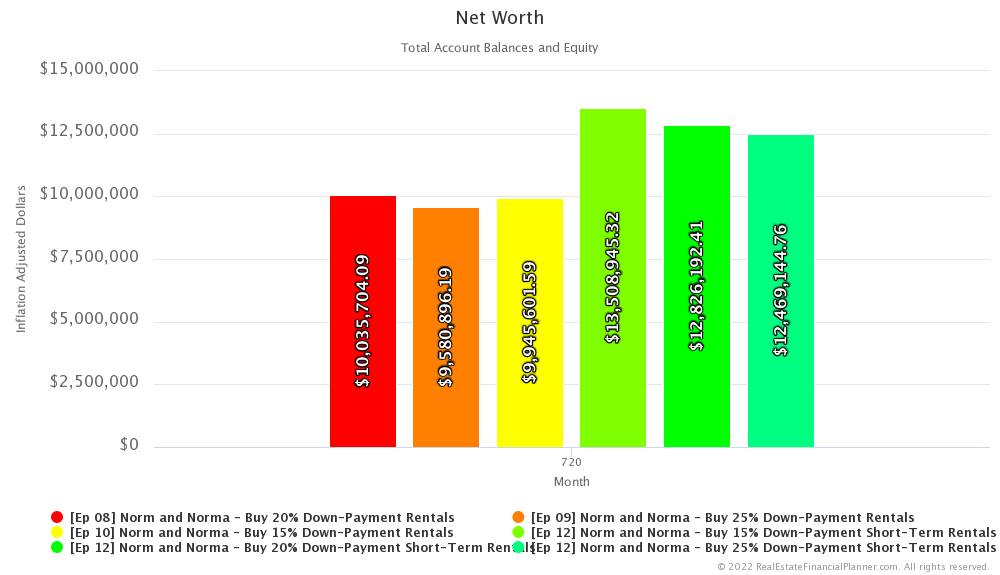

Net Worth

But, what about net worth? What impact does doing short-term rentals have on their overall net worth compared to doing long-term rentals?

Well, doing short-term rentals results in a higher net worth. You could have easily guessed that. But how much better?

Well, at the end of 60 years… the net worths for long-term rentals are all in the mid to high $50 million range where for short-term rentals they’re all in the $70 million range.

But, if we adjust for inflation back to today’s dollars it is a lot lower. For example, the net worths for long-term rentals are in the high $9 million to just over $10 million dollar range. Compare that to net worths in the mid $12 to mid $13 million range for doing short-term rentals.

So, I’d call about $3 million difference on about $10 million dollars pretty significant, but remember it comes with the extra work of doing some additional management which we did not end when they technically achieved financial independence… we assumed they kept doing short-term rentals and doing that extra management associated with doing short-term rentals.

Higher Standard of Living

But the extra cash flow they’re receiving from doing short-term rentals does mean they could live at a higher standard of living then the expenses we modeled.

In fact, by the time they achieve financial independence with long-term rentals putting 15% down, they could be living at TWICE the standard of living with short-term rentals… for all down payment scenarios of the short-term rentals.

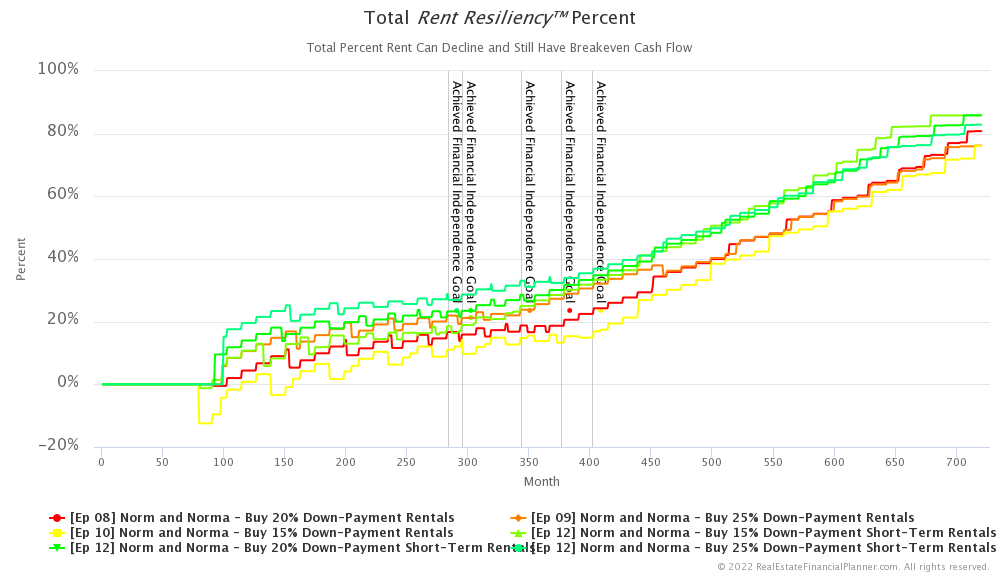

Risk

Increasing their standard of living could increase their risk a little bit.

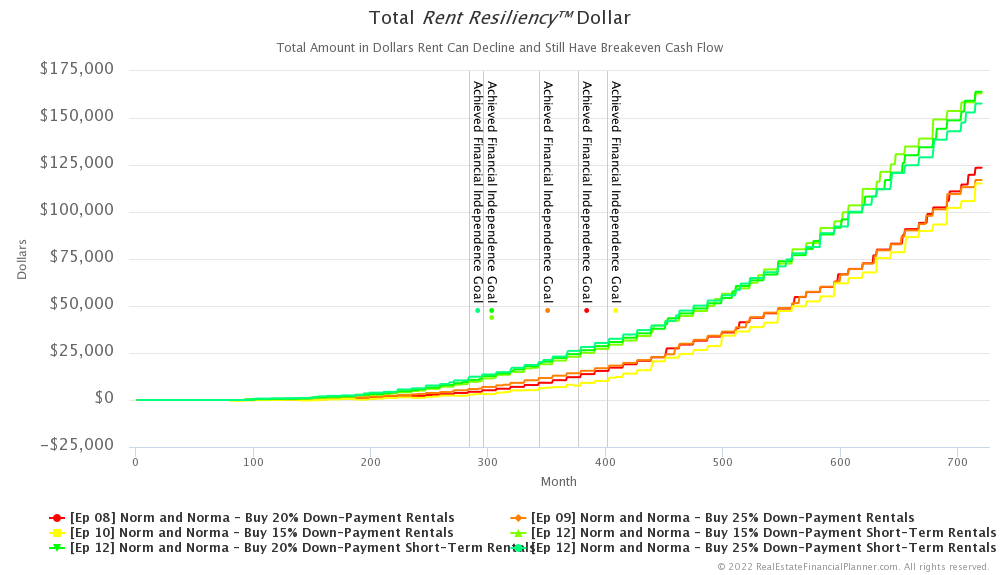

For example, one measure of risk is how resilient are they to drops in rents?

With short-term rentals, they’re collecting higher rents.

In general that means that rents can drop more before they’d have negative cash flow. So, Rent Resiliency is better when they do short-term rentals.

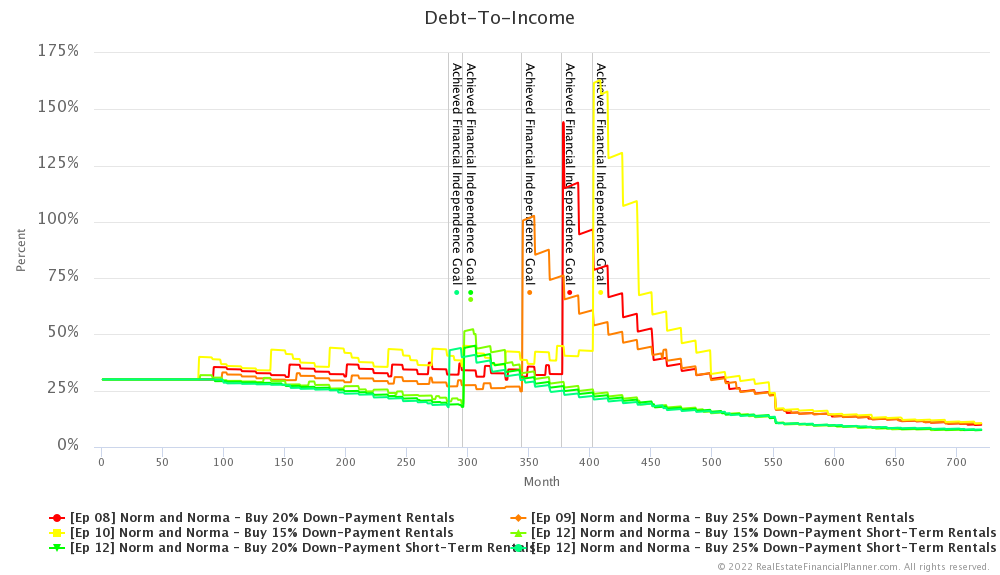

Debt-To-Income

Another measure of risk is debt-to-income.

I already talked about how getting more income from the properties by doing short-term rentals helps with their debt-to-income ratios.

Having lower debt-to-income ratios is a measure that they have lower risk when you think about risk in terms of income compared to debt obligations.

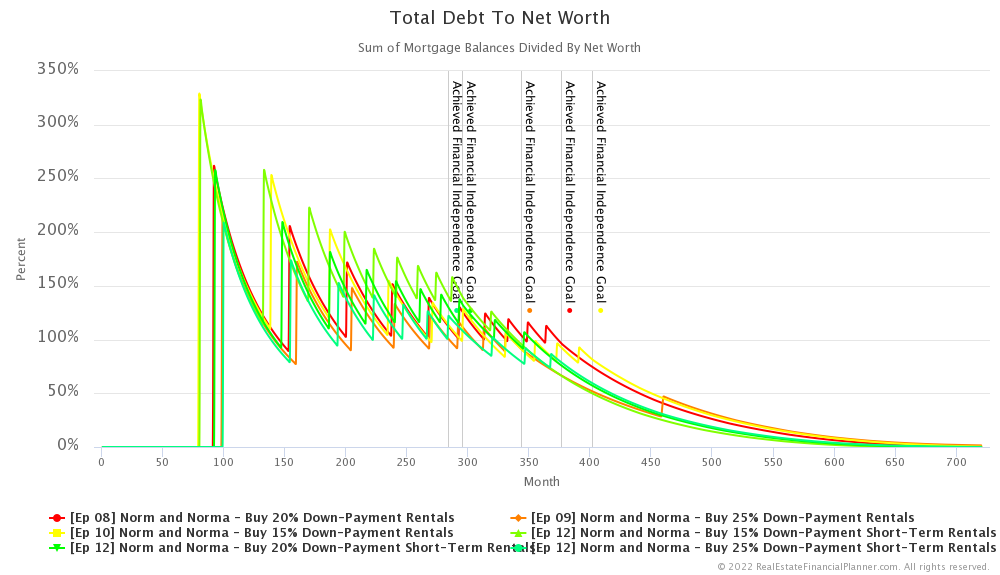

Debt to Net Worth

Another measure of risk is to look at how much debt they have compared to their overall net worth. It is true that the extra cash flow and buying properties sooner ultimately improves their net worth but they’re buying the same properties with similar down payment amounts. That does mean that debt to net worth is probably slightly better with short-term rentals but it is not *that* significant in my opinion.

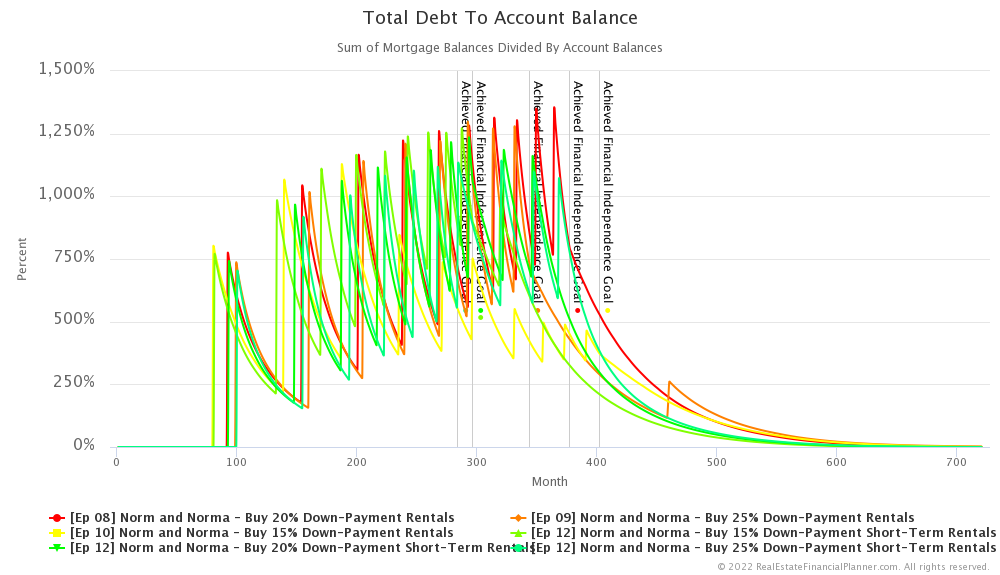

Total Debt To Account Balance

A similar argument can be made with total debt to account balance… short-term rentals have less risk with this measurement, but it is not drastically different.

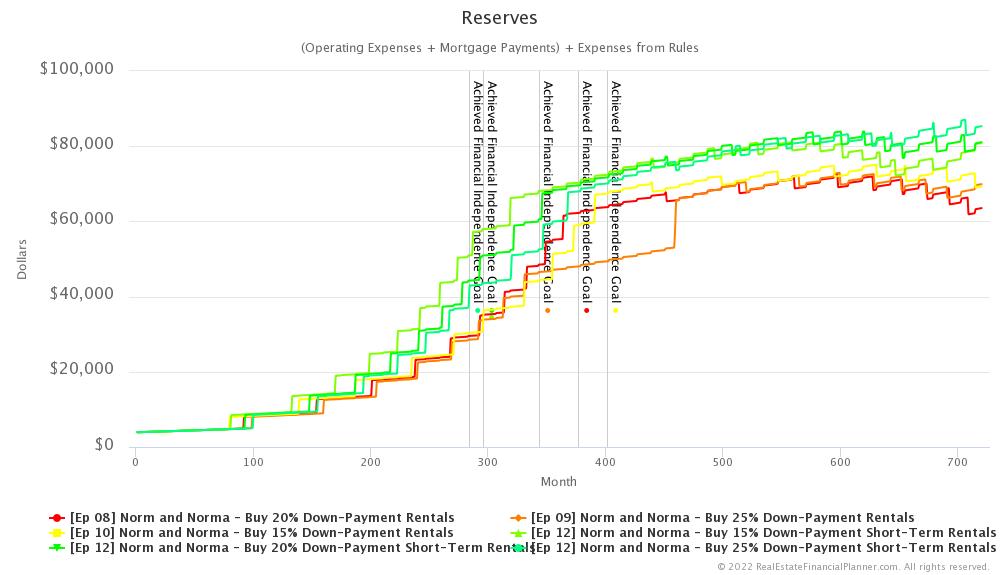

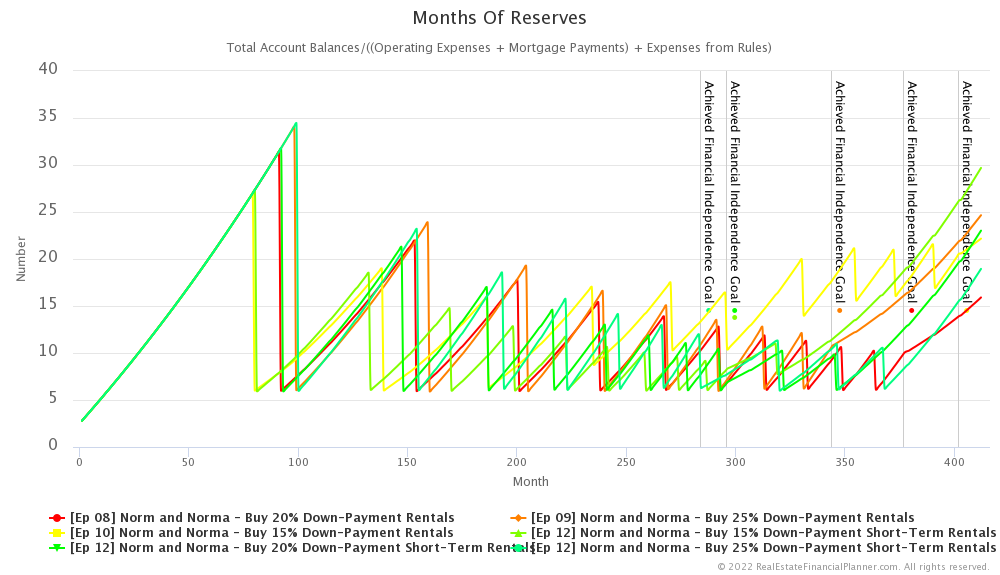

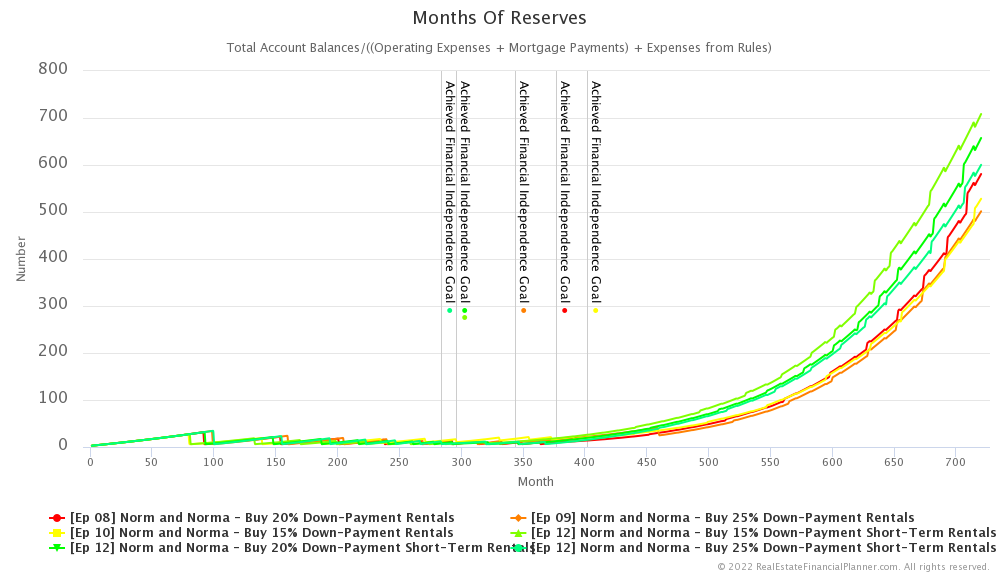

Reserves

One more discussion about risks… let’s talk about reserves.

Since we’ve modeled short-term rentals with having 20% maintenance instead of the 10% that we’ve used with long-term rentals and the rent amount we’re using further amplifies this, we need more reserves for short-term rentals.

I’ll also throw out there that with irregular income… some months being much better than others… the case can be made that reserves are even more important.

Side Note: If we look at how much Norm and Norma

End of side note and back to our discussion of reserves.

Since we model the purchase of properties as requiring they have six months of reserves set aside before they buy the next property it means that they keep hovering around 6 months of reserves while acquiring properties. The number of months of reserves increases as they save up their next down payment and drops back to 6 months when they acquire their next property.

However, once they’re done acquiring properties, the improved cash flow from the short-term rentals and them NOT increasing their standard of living means that they have more months of reserves saved with short-term rentals.

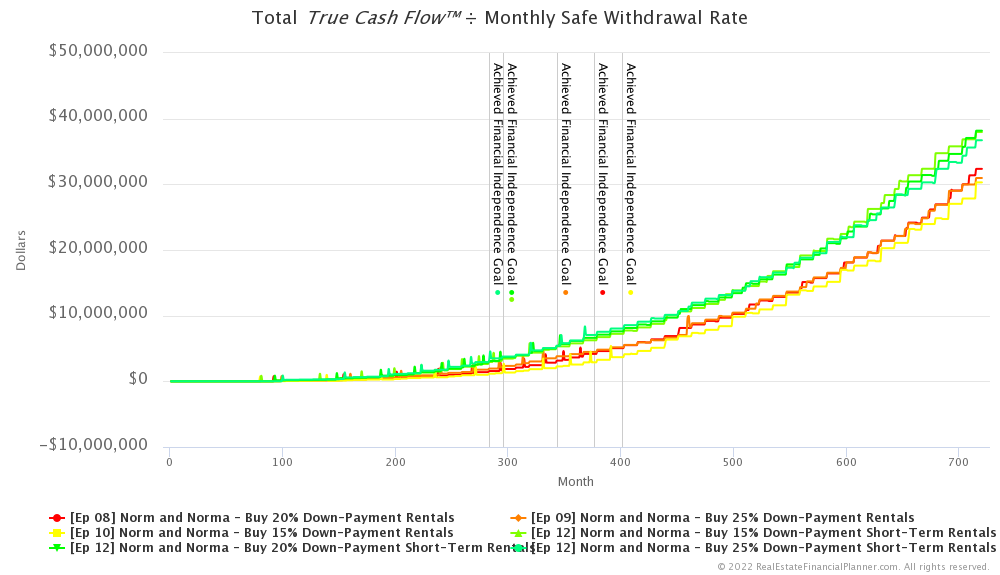

Total True Cash Flow™ ÷ Monthly Safe Withdrawal Rate

I’d like to pause for a moment to introduce a new concept.

If you recall from previous episodes, we discussed how if you take the money you have invested in stocks or bonds or similar investments we could multiply the amount you have invested times your safe withdrawal rate to determine how much money you can… at least in theory… safely withdrawal each year without running out of money.

Well, what if we turned that equation around and used it with rental properties instead?

For example, we know how much cash flow the rental properties are producing and we know what Norm and Norma

What if we took the cash flow from the rental properties and divided it by the safe withdrawal rate? We could come up with a number that represents how much money they would have needed to have invested in the stock market or other similar investments to produce that same amount of cash flow.

It gives us an idea of what the rental properties are worth to us if they were money invested in stocks instead.

When I do this calculation I don’t use just plain old cash flow… I tend to use cash flow and the tax benefits… what we call Cash Flow from Depreciation™. When we combine cash flow and Cash Flow from Depreciation™ we call that True Cash Flow™.

So, for the calculation to determine what the rental properties are worth if they were invested in stocks, I’d take True Cash Flow™ and divide it by the monthly safe withdrawal rate to come up with a value for what the rental properties would be worth if they were invested in an investment that generated the same amount of cash flow.

I call this calculation the very literal: Total True Cash Flow™ ÷ Monthly Safe Withdrawal Rate.

I bring this up in this episode because when Norm and Norma

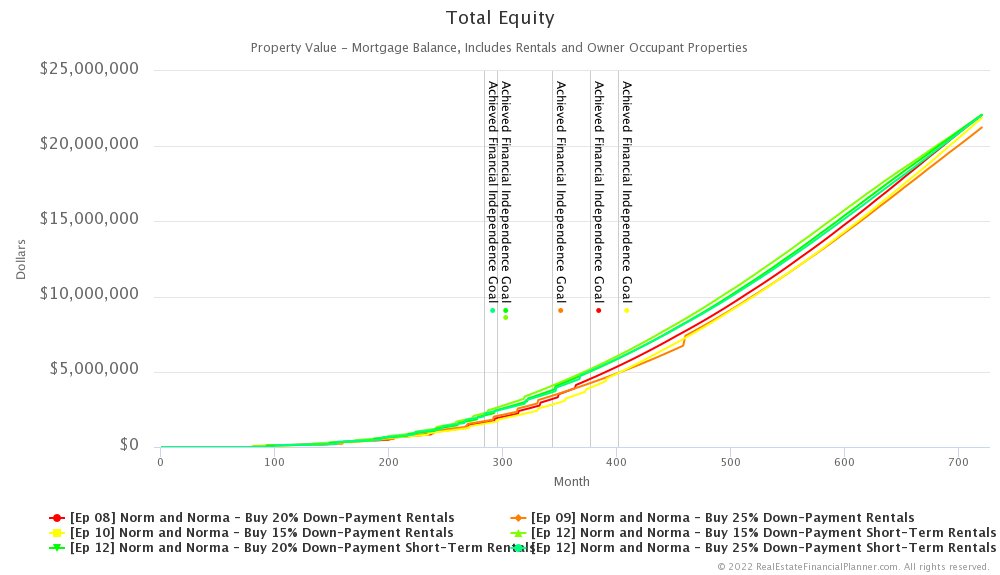

Equity

If you recall earlier in this episode I mentioned that Norm and Norma

Of course, once all the properties are paid off, they have the same amount of equity since we’re assuming they’re essentially the same properties.

Conclusion

In conclusion, renting themselves and buying 10 short-term rentals adds some extra work, but it does:

- Speed up their ability to achieve financial independence

- Improves cash flow and net worth

- Allows a higher standard of living

- And reduces risk in many measures of risk that we considered

So, this seems like a viable option for them to consider as they evaluate which is the optimal path for them to achieve financial independence.

But they were getting attached to the idea of buying a home to live in, what is the impact of buying a home to live then buying 10 short-term rentals on their journey toward financial independence? We’ll discuss that in the next episode.

Next Episode

Also, be sure to check out the Advanced Real Estate Financial Planner™ Podcast to see how having variable property appreciation rates and rent appreciation rates, variable mortgage interest rates, variable inflation rate and variable stock market rates of return impacts Norm and Norma

I hope you have enjoyed this Episode about Norm and Norma

Get unprecedented insight into Norm Norma’s Scenario with dozens of detailed, interactive charts.

Compare “short-term rental versus long-term rental” in pairs by down payment:

Or, compare all of them together. Please be aware that with 6 variations on the same chart, they can be a bit cluttered and harder to interpret.

Inside the Numbers

Watch the Inside the Numbers video to see exactly how we set up their Scenario

Buying Long-Term Rental Properties

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 10 Norm and Norma - Buy 15% Down-Payment Rentals with 2  Accounts, 1

Accounts, 1  Property, and 6

Property, and 6  Rules.

Rules.

Or, read the detailed, computer-generated, narrated  Blueprint™

Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 08 Norm and Norma - Buy 20% Down-Payment Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 09 Norm and Norma - Buy 25% Down-Payment Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Buying Short-Term Rental Properties

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 12 Norm and Norma - Buy 15% Down-Payment Short-Term Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 12 Norm and Norma - Buy 20% Down-Payment Short-Term Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 12 Norm and Norma - Buy 25% Down-Payment Short-Term Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Podcast Episodes

The following are the podcast episodes for variations of Norm Norma’s

More posts: Norm Episode