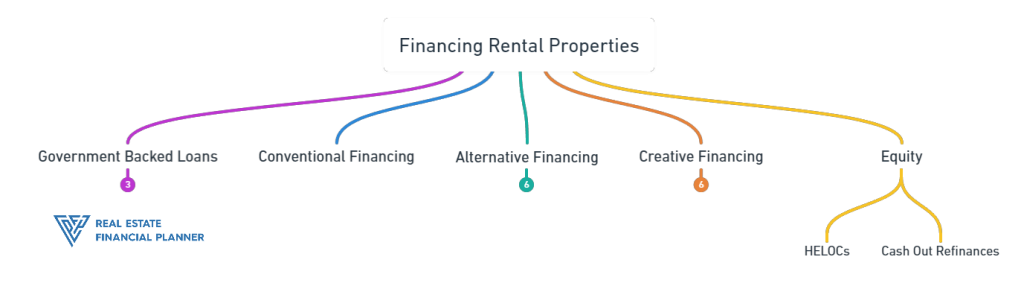

In the world of real estate investing, one of the most pivotal decisions you’ll make is how to finance your property acquisitions. Whether you’re a seasoned investor eyeing your next rental property or a newcomer ready to dive into the lucrative realm of real estate, understanding the vast landscape of financing options can significantly impact your investment strategy and overall success. From government-backed loans designed with favorable terms to alternative financing routes that offer flexibility for more unique investment scenarios, the right financing choice can open doors to opportunities while aligning with your financial goals and investment timeline. This guide aims to illuminate the variety of financing pathways available to real estate investors, focusing on the nuances of each to help you navigate the complex yet rewarding world of real estate investment financing. By exploring the advantages and considerations of each option, from conventional loans to more creative lending solutions, you’ll be better equipped to tailor your financing strategy to your specific investment needs, optimizing your potential for growth and profitability in the dynamic landscape of real estate.

Government-Backed Loans

Navigating the realm of real estate investment requires not just savvy negotiation and market insight but also a keen understanding of the financing options at your disposal. Among these, government-backed loans stand out as particularly appealing for a broad swath of investors, thanks to their favorable terms and conditions. These loans are supported by various government agencies, each designed to make property ownership more accessible and affordable. Let’s delve into the three primary types of government-backed loans that real estate investors, especially those eyeing rental properties, should consider:

- VA Financing: Zero down payment, no PMI for veterans and active military.

- USDA Financing: No down payment for eligible rural properties.

- FHA Financing: Low down payment, accessible for first-time investors.

For veterans and active military members eyeing real estate investment, VA financing emerges as a particularly advantageous option. Established to honor the service of America’s military personnel, VA loans offer several unique benefits that can significantly ease the path to property ownership and investment. Here’s a closer look at what VA financing entails and why it stands out as a prime choice for eligible investors:

- Zero Down Payment: Perhaps the most compelling feature of VA loans is the ability to finance 100% of a property’s purchase price. This eliminates the barrier of saving for a large down payment, making it easier for veterans and active military members to invest in real estate sooner rather than later.

- No Private Mortgage Insurance (PMI): Unlike many other loan types, VA loans do not require borrowers to pay PMI, a monthly expense that can add a significant cost to other types of financing. This absence of PMI can save investors hundreds of dollars each month, increasing the cash flow potential from rental properties.

- Competitive Interest Rates: VA loans typically offer interest rates that are comparably lower than those of conventional loans. Lower interest rates translate to lower monthly mortgage payments, enhancing the affordability of investment properties and improving the return on investment over time.

- Flexible Credit Requirements: While VA loans do have credit requirements, they are generally more lenient than those for conventional financing. This flexibility opens the door for many veterans and active service members who may not qualify for other types of loans due to credit history.

- VA Loan Limits and Funding Fees: It’s important to note that while the VA does not set a cap on the amount an eligible person can borrow, lenders may impose their own loan limits based on the borrower’s credit, income, and other factors. Additionally, most VA loans come with a funding fee, a one-time charge that varies based on the loan amount, type of loan, and the borrower’s military category. This fee helps fund the VA loan program and is often financed into the loan amount.

- Use for Various Property Types: VA loans can be used to purchase a variety of property types, including single-family homes, condos, and multi-unit properties, as long as the borrower intends to occupy one of the units as their primary residence. This opens up opportunities for savvy investors to live in one unit while renting out the others, creating a stream of rental income.

- Lifetime Benefit: Another remarkable aspect of VA financing is that it’s a lifetime benefit. Eligible veterans and service members can use the VA loan benefit multiple times throughout their lives, offering ongoing access to its advantages for future real estate investments.

VA financing stands as a testament to the United States’ commitment to its military members, offering them a powerful tool to achieve their real estate investment goals. By leveraging the unique benefits of VA loans, veterans and active military members can navigate the real estate market with greater ease and confidence, turning the dream of property investment into a tangible reality.

USDA financing, provided by the United States Department of Agriculture, is a unique loan program designed to encourage homeownership in rural and suburban areas. For real estate investors looking to explore markets outside of urban centers, USDA loans offer an attractive pathway with several key benefits:

- No Down Payment Required: One of the most significant advantages of USDA loans is the possibility to finance up to 100% of a property’s purchase price. This feature allows investors to acquire properties without the initial financial burden of a down payment, making real estate investment more accessible.

- Lower Interest Rates: Generally, USDA loans come with interest rates that are competitive with, or sometimes even lower than, conventional loan rates. Lower interest rates can significantly reduce the monthly cost of owning an investment property, improving cash flow and the potential for profit.

- Minimal Insurance Costs: While USDA loans do require a form of mortgage insurance, the upfront and annual fees are typically lower than those associated with other loan types. This reduced cost further enhances the affordability of properties financed through USDA loans.

- Eligibility Based on Location and Income: To qualify for a USDA loan, the property must be located in an eligible rural or suburban area as defined by the USDA. Additionally, borrowers must meet certain income limits, which are set to ensure the program serves those it’s intended to help. This focus on rural and suburban areas opens up unique investment opportunities that might be overlooked by traditional investors.

- Use for Primary Residences: It’s important to note that USDA loans are intended for primary residences. However, for investors willing to live in one of the units of a multi-family property or those planning to transition a property into a rental after meeting initial occupancy requirements, USDA financing can still be a valuable tool.

USDA financing is a powerful option for real estate investors looking to capitalize on the potential of rural and suburban markets. By removing some of the traditional barriers to entry, such as the need for a down payment, USDA loans make it possible to enter the real estate market with less capital, offering a unique advantage in the pursuit of investment properties.

Federal Housing Administration (FHA) loans present a compelling financing option for those entering the real estate investment arena. Catering especially to first-time homebuyers and investors with limited capital, FHA loans offer several attractive features that can facilitate the acquisition of investment properties:

- Low Down Payment Requirements: FHA loans are renowned for their low down payment requirement, as low as 3.5% of the purchase price. This makes real estate investment more attainable for individuals without substantial savings.

- Accessible Credit Qualifications: Compared to conventional financing options, FHA loans have more lenient credit criteria, opening the door for investors who may not have perfect credit scores.

- High Loan-to-Value Ratio: FHA financing allows for a higher loan-to-value ratio, meaning investors can borrow a greater portion of the property’s value. This reduces the amount of cash required upfront and can accelerate the investment process.

- Insurance for the Lender: FHA loans come with a mandatory Mortgage Insurance Premium (MIP), which protects lenders against losses if the borrower defaults on the loan. While this does add a cost to the borrower, it’s this insurance that enables the favorable terms of FHA loans.

- Use for Multi-Unit Properties: An appealing aspect of FHA loans for real estate investors is the ability to use them for purchasing multi-family properties, up to 4 units, as long as one of the units is occupied by the borrower as their primary residence. This allows investors to live in one unit and rent out the others, generating income that can cover the mortgage and operational costs.

- Refinancing Opportunities: FHA loans offer streamlined refinancing options, which can be beneficial for investors looking to improve their loan terms in the future, especially if interest rates drop or their financial situation improves.

FHA financing stands out as a gateway for individuals and families to step into real estate investment. By offering a combination of low down payment requirements, lenient credit qualifications, and the possibility to invest in multi-unit properties, FHA loans provide a foundation for building a real estate portfolio with less initial capital.

Conventional Financing

Conventional loans, not insured or guaranteed by any government agency, remain the most popular choice for real estate investors due to their flexibility and potential cost savings for those who qualify. This type of financing offers a straightforward approach to purchasing investment properties, with several key characteristics:

- Higher Credit Score Requirements: Conventional loans typically require a higher credit score than government-backed options. Investors with strong credit histories can benefit from more competitive interest rates and lower fees.

- Varied Down Payment Options: Down payment requirements for conventional loans can range from as low as 3% to 20% or more, depending on the lender’s policies and the borrower’s financial profile. A higher down payment usually results in better loan terms and lower interest rates.

- No PMI with 20% Down: One of the significant advantages of conventional financing is the ability to avoid private mortgage insurance (PMI) by making a down payment of 20% or more, which can substantially reduce the monthly payment.

- Loan Limits: Conventional loans are subject to maximum loan limits set by government-sponsored entities Fannie Mae and Freddie Mac. These limits vary by location and are periodically updated to reflect changes in the housing market.

- Investment Property Interest Rates: Interest rates for conventional loans on investment properties are typically higher than those for primary residences, reflecting the increased risk associated with rental properties. However, investors with excellent credit can still secure competitive rates.

- Flexibility in Property Types: Conventional financing can be used for a wide range of property types, including single-family homes, multi-unit properties, condos, and townhouses. This versatility makes it a suitable option for many investment strategies.

Conventional financing stands as a testament to traditional real estate investment, offering a blend of rigor and reward. For investors with the financial wherewithal to meet its more stringent requirements, conventional loans provide a path to property ownership with potential long-term benefits, including equity building and the possibility of no mortgage insurance. As with any investment decision, weighing the pros and cons of conventional financing in the context of your financial situation and investment goals is crucial.

Alternative Financing Options

While traditional financing methods serve as the backbone for many real estate transactions, a dynamic and diverse market demands equally versatile financing solutions. Alternative financing options cater to this need, offering real estate investors creative and flexible pathways to acquire properties. These methods can be particularly appealing for those facing challenges with conventional loan approval, seeking faster closings, or looking for financing that accommodates unique investment strategies. From private lenders to hard money loans, commercial loans, and portfolio loans, alternative financing provides a broad spectrum of opportunities for investors to leverage their assets and realize their investment goals. This section delves into the nuances of each alternative financing route, highlighting how they can fit into various investment scenarios and propel investors towards success in the competitive world of real estate.

- Private Lenders: Flexible terms, often faster funding with higher interest rates.

- Hard Money Loans: Asset-based lending suitable for fix-and-flips.

- Commercial Loans: For income-producing properties, based on business creditworthiness.

- Portfolio Loans: More flexible criteria, kept in-house by lenders.

- Self-Directed Retirement Accounts: Utilize self-directed 401Ks and self-directed IRAs to invest in real estate.

Private money loans represent a flexible and often accessible form of financing for real estate investors, sourced from individual investors or small groups rather than traditional financial institutions. This type of financing can be a game-changer for investors looking for quick closings, flexible terms, and funding for projects that might not meet the criteria of conventional lenders. Here are the key features and benefits of using private money loans for real estate investments:

- Speed of Funding: One of the most significant advantages of private money loans is the speed at which transactions can be completed. Without the extensive paperwork and approval processes typical of banks, funding can be secured in a matter of days, making it ideal for time-sensitive deals.

- Flexibility in Terms: Private lenders are often more flexible than traditional lending institutions, allowing for negotiation on loan terms, interest rates, and repayment schedules. This flexibility can be particularly beneficial for unique or unconventional real estate projects.

- Asset-Based Lending: Private money loans are typically secured by the property itself, with less emphasis on the borrower’s credit score or income. This focus on the asset’s value rather than the borrower’s financial history can be advantageous for investors with less-than-perfect credit.

- Higher Costs: The convenience and flexibility of private money loans often come at a cost, with interest rates and fees that are generally higher than those of traditional loans. However, for many investors, the benefits of quick access to capital and lenient terms outweigh the higher costs.

- Shorter Loan Terms: Private money loans usually have shorter terms than traditional mortgages, often ranging from one to five years. This necessitates a clear exit strategy for repayment, such as refinancing with a long-term loan or selling the property for a profit.

Private money loans can provide a crucial lifeline or strategic advantage for real estate investors, enabling deals that might not be possible through traditional financing routes. By understanding and leveraging the unique aspects of private lending, investors can expand their portfolio and execute on investment opportunities with speed and agility.

Hard money loans stand out as a pivotal financing tool for real estate investors, particularly those involved in fix-and-flip projects, land loans, or when a quick close is crucial. These loans are provided by private investors or companies and are primarily secured by the value of the property being purchased. Unlike traditional bank loans, hard money loans prioritize the asset’s potential rather than the borrower’s creditworthiness, offering a unique blend of speed and accessibility. Here’s what makes hard money loans a valuable option for certain investment strategies:

- Rapid Approval and Funding: Hard money lenders typically offer a swift approval process, with funding available in as little as a few days. This speed can be crucial for investors looking to secure properties in competitive markets or those needing immediate cash to take advantage of investment opportunities.

- Asset-Based Lending: The primary criterion for hard money loans is the value of the property and its potential after repair or development, rather than the borrower’s financial history. This focus allows investors with varied credit histories to obtain financing.

- Flexibility in Terms: Hard money lenders often provide more flexible terms compared to traditional financing options. Loan terms, interest rates, and repayment schedules can often be negotiated to fit the specific needs of the investment project.

- Higher Costs: The convenience and accessibility of hard money loans come at a price. Interest rates are typically higher than those of conventional loans, reflecting the greater risk assumed by the lender. Additionally, origination fees and closing costs can also be higher.

- Shorter Loan Duration: Hard money loans are generally structured as short-term financing solutions, with loan terms often ranging from one to three years. This necessitates a solid exit strategy on the part of the investor, such as selling the property or refinancing into a longer-term loan.

Hard money loans provide a critical financing avenue for real estate investors, enabling them to capitalize on short-term opportunities and projects that require quick action. While the costs associated with hard money loans are higher than traditional financing, the value they offer in terms of speed and flexibility can significantly outweigh these expenses for the right investment scenario.

Commercial loans cater specifically to the needs of investors looking to purchase or refinance income-producing properties such as office buildings, retail spaces, apartment complexes, and more. Unlike residential loans, commercial loans are evaluated based on the income potential and operating history of the property, offering a distinct set of criteria and benefits for real estate investors. Here are the key aspects of commercial loans that investors should consider:

- Focus on Property Income: Lenders assess commercial loan applications based on the property’s ability to generate income, considering factors like occupancy rates, lease lengths, and the financial stability of tenants. This focus shifts the emphasis from the individual investor’s financial situation to the property’s earning potential.

- Longer Approval Process: Due to the detailed analysis of the property’s financials, the approval process for commercial loans can be more time-consuming than for residential loans. Investors should be prepared for thorough due diligence checks and potentially lengthy closing times.

- Higher Down Payment Requirements: Commercial loans typically require higher down payments compared to residential financing, often ranging from 20% to 30% of the purchase price. This reflects the higher risk associated with commercial real estate investments.

- Variable Interest Rates and Terms: Commercial loan interest rates and terms can vary widely based on the lender, the type of property, and the loan’s structure. Terms are generally shorter than residential mortgages, with many loans structured to have balloon payments after a set period or amortization schedules that exceed the loan term.

- Personal Guarantee Requirements: While the loan is primarily secured by the property, lenders may require a personal guarantee from the investor, making them personally liable if the loan defaults. This is especially common in loans for smaller or riskier properties.

Commercial loans offer real estate investors the opportunity to expand their portfolios into the potentially lucrative market of income-producing properties. Understanding the unique aspects of commercial financing, including the emphasis on property income and the more rigorous approval process, is essential for navigating this complex yet rewarding investment landscape.

Portfolio loans present a flexible financing option for real estate investors, offered by lenders who keep the loans within their own portfolios rather than selling them on the secondary market. This type of loan is particularly suited for investors who may not qualify for traditional loans due to unconventional income sources, the desire to finance multiple properties at once, or the need for more tailored loan terms. Here are the distinctive features and advantages of portfolio loans:

- Customized Loan Terms: Since portfolio lenders manage their own loans, they have the flexibility to offer customized terms that match the unique needs and situations of individual investors. This can include adjustable interest rates, varied loan lengths, and tailored repayment schedules.

- More Holistic Evaluation Process: Portfolio lenders often take a more comprehensive approach to assessing loan applications, considering the overall financial picture and potential of the investor and their projects, rather than strictly adhering to conventional lending criteria.

- Financing for Multiple Properties: For investors looking to finance several properties simultaneously, portfolio loans can provide a streamlined solution, allowing for the consolidation of multiple property loans into a single loan agreement.

- Higher Flexibility with Property Types: Portfolio loans can be used for a wide variety of property types, including those that might not qualify for traditional financing, such as mixed-use buildings, non-warrantable condos, or properties requiring significant renovation.

- Potentially Higher Costs: The increased flexibility and customization of portfolio loans often come with higher interest rates and fees compared to standard loans. Investors should carefully consider these costs against the benefits of a more personalized lending solution.

Portfolio loans offer a viable path for real estate investors facing challenges with traditional financing routes or those in need of more bespoke financing solutions. By working closely with a portfolio lender, investors can secure the funding needed to move forward with their investment strategies, even in complex or non-traditional scenarios.

Self-Directed 401Ks and Self-Directed IRAs

Self-Directed 401Ks and Self-Directed Individual Retirement Accounts (IRAs) offer real estate investors an innovative way to leverage retirement funds for investment in real estate. Unlike traditional retirement accounts, which are typically limited to stocks, bonds, and mutual funds, self-directed options allow investors to diversify their portfolios with real estate assets. Here’s how these tools can be a game-changer for savvy investors:

- Broader Investment Choices: Self-Directed 401Ks and IRAs enable investors to use their retirement funds to invest in a wide range of real estate opportunities, from rental properties and fix-and-flips to land and commercial real estate, offering a path to potentially higher returns compared to traditional retirement investments.

- Tax Advantages: Investing in real estate through a Self-Directed IRA or 401K can provide significant tax benefits. Growth is tax-deferred, and in the case of Roth accounts, it may be tax-free. This can enhance the compounding effect of your investments over time.

- Direct Control Over Investments: Investors have direct control over their investment choices, allowing for a hands-on approach to building their retirement portfolio with real estate. This control requires due diligence and a deep understanding of real estate investing to navigate successfully.

- Complexity and Regulations: While offering greater flexibility, Self-Directed IRAs and 401Ks come with specific IRS rules and regulations, including prohibitions on self-dealing and transactions with disqualified persons. It’s crucial to understand these rules to avoid unintended tax consequences and penalties.

- Need for Custodian: Self-Directed IRAs require an IRS-approved custodian to hold the account. Choosing a custodian familiar with real estate investments can streamline the process, but investors should be mindful of custodian fees and services.

Self-Directed 401Ks and IRAs unlock the potential for real estate investors to grow their retirement savings through direct investment in the property market. By understanding the opportunities and challenges associated with these accounts, investors can strategically integrate real estate into their long-term financial planning, potentially achieving greater diversification and returns on their retirement funds.

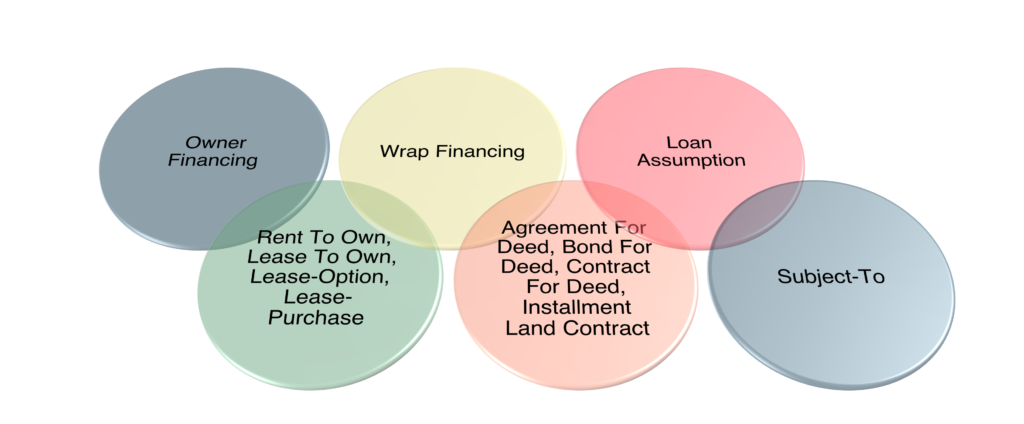

Creative Financing

In the dynamic world of real estate investment, traditional financing methods sometimes fall short of meeting every investor’s needs. Creative financing options step into this gap, offering innovative solutions that can bypass common obstacles such as credit issues, down payment challenges, and stringent lending criteria. From owner financing to wrap financing, loan assumptions, rent-to-own arrangements, agreements for deed, and buying properties subject to existing financing, these strategies open up new avenues for securing investment properties. Each method comes with its own set of advantages, considerations, and suitability depending on the investor’s situation and goals. This section delves into the mechanics of these creative financing options, providing insights on how they can be leveraged to facilitate real estate acquisitions, enhance flexibility, and potentially reduce costs.

- Owner Financing – Where the seller owns the property free and clear of all mortgages and acts like the bank and allows you to make payments when purchasing the property.

- Wrap Financing – Where the seller finances the property for the purchase by there is still an underlying loan on the property from the seller that is wrapped.

- Loan Assumption – Where you formally assume responsibility for the seller’s loan from the lender.

- Rent-To-Own, Lease-To-Own, Lease-Option, Lease-Purchase – Where you rent or lease the property with the option or purchase contract to be able to buy the property at a later date.

- Agreement-For-Deed, Bond-For-Deed, Contract-For-Deed, Installment Land Contract – A form of seller financing where you make payments and get the deed when you’ve fulfilled your contractual obligations to the seller.

- Subject To – Where the seller deeds you ownership of the property but leaves their existing loan (or other liens) in place and you agree to buy the property

“subject to” the existing financing (and/or other liens).

Owner financing, also known as seller financing, is a creative real estate acquisition method where the property’s seller acts as the lender, providing the buyer with the loan needed to purchase the property. This arrangement eliminates the need for a traditional mortgage from a bank or financial institution, offering a flexible and negotiable path to ownership for both parties. Here are the key aspects and benefits of owner financing for real estate investors:

- Negotiable Terms: One of the primary advantages of owner financing is the ability to negotiate the loan terms directly with the seller. Interest rates, repayment schedules, and down payment amounts can often be tailored to suit the financial situations of both the buyer and seller.

- Reduced Closing Costs: Without the involvement of traditional lenders, the closing costs associated with owner financing transactions are typically lower, saving both parties money.

- Faster Closing Process: Owner financing can significantly speed up the closing process since it bypasses many of the steps required by banks and mortgage lenders, such as extensive credit checks and loan underwriting.

- Accessibility for Buyers with Credit Challenges: For buyers who may not qualify for traditional financing due to credit issues or unconventional income sources, owner financing provides an accessible alternative, allowing them to purchase property they might otherwise be unable to afford.

- Income Stream for Sellers: For sellers, providing financing can create a steady income stream from the interest payments on the loan, often at a higher interest rate than traditional savings or investment options.

While owner financing offers numerous advantages, it’s important for both buyers and sellers to conduct thorough due diligence, possibly consulting with legal and financial professionals to structure the agreement. Properly executed, owner financing can be a win-win situation, providing sellers with a viable buyer and offering buyers a unique opportunity to purchase real estate without the hurdles of traditional loan approval processes.

Wrap financing, also known as a wraparound mortgage, is a form of creative financing where a seller extends a secondary mortgage to a buyer that “wraps around” and includes the existing mortgage. This innovative strategy allows buyers to make payments to the seller, who then continues to pay the original mortgage, often at a different interest rate. Wrap financing can be particularly useful in scenarios where buyers have difficulty securing traditional financing. Here’s how wrap financing works and its benefits for real estate investors:

- Consolidated Payments: Buyers make one monthly payment to the seller, covering both the new wraparound loan and the underlying original mortgage. This simplifies the payment process and can offer more favorable terms than obtaining a new mortgage directly.

- Flexible Financing: Wrap financing agreements can be customized to fit the financial situations and goals of both the buyer and the seller, including adjustable interest rates, down payments, and loan durations.

- Opportunity for Buyers with Credit Issues: Buyers who might not qualify for a traditional mortgage due to credit history or other factors may find wrap financing a viable path to homeownership or investment.

- Income Potential for Sellers: Sellers can potentially earn income from the interest rate spread between the original mortgage and the wraparound loan, making it an attractive option for sellers looking to maximize their return on investment.

However, it’s crucial for both parties to be aware of the risks and legalities involved in wrap financing, including the need for transparency with the existing lender to avoid triggering a due-on-sale clause. Proper legal and financial counsel should be sought to structure the deal appropriately, ensuring a beneficial outcome for both the buyer and the seller in the real estate transaction.

Loan assumption is a financial strategy in real estate where a buyer takes over, or “assumes,” the seller’s existing mortgage under its current terms. This approach can be particularly advantageous in a market where existing loan terms are more favorable than current market rates. By assuming a mortgage, buyers can bypass the conventional loan application process, potentially saving on closing costs and interest rates. Here are the essential aspects and benefits of loan assumption for real estate investors:

- Preservation of Favorable Loan Terms: If the existing mortgage has a lower interest rate than current market rates, assuming the loan can offer significant long-term savings on interest payments.

- Reduced Closing Costs: Since the mortgage is not being originated anew, the closing costs associated with loan assumption are typically lower than those for securing a new mortgage.

- Quicker Transaction Process: The process of assuming a loan can be faster than applying for a new mortgage, facilitating a quicker property transfer and potentially giving buyers a competitive edge in hot markets.

- Lender Approval Required: It’s important to note that not all mortgages are assumable, and the process requires approval from the existing lender. Lenders will assess the buyer’s creditworthiness and may impose additional conditions.

- Potential for Immediate Equity: Assuming a mortgage can also offer the benefit of immediate equity in the property, especially if the property’s value has increased since the original mortgage was secured.

For buyers and sellers alike, loan assumption can be a mutually beneficial strategy, offering a streamlined path to property acquisition and sale. However, it is crucial to carefully review the terms of the existing mortgage and secure lender approval before proceeding with a loan assumption to ensure it aligns with the buyer’s investment goals and financial situation.

Rent-to-own agreements provide a unique pathway to homeownership, blending elements of leasing and property purchase. This arrangement allows tenants to rent a property with the option to buy it at a later date, typically within a set period. Rent-to-own can be an attractive option for individuals who are not yet ready to secure financing through traditional means but wish to invest in their future home. Here’s how rent-to-own works and its potential benefits for real estate investors:

- Option Fee: Tenants pay an upfront option fee, usually a percentage of the home’s price, which grants them the option to purchase the property in the future. This fee may be credited towards the purchase price if the tenant decides to buy.

- Rent Premiums: A portion of the monthly rent typically goes towards the purchase price. This rent premium allows tenants to build equity in the home over the lease term, even before officially purchasing it.

- Fixed Purchase Price: In many rent-to-own agreements, the purchase price is fixed at the lease’s start, offering potential savings if the property’s market value increases over the rental period.

- Time to Improve Credit: Rent-to-own provides tenants with time to improve their credit scores and financial standing, enhancing their ability to qualify for a mortgage when they opt to purchase.

- Test Drive: This arrangement allows tenants to live in the home before committing to purchase, giving them insight into the property and neighborhood to ensure it’s a good fit.

Rent-to-own agreements can serve as a beneficial strategy for investors and tenants alike, offering a creative solution to bridge the gap between renting and owning. However, it’s crucial for both parties to clearly understand the terms and conditions, including deadlines, fees, and responsibilities, to ensure a successful transition from tenant to homeowner.

An Agreement-for-Deed, also known as a land contract or contract for deed, is a real estate purchase agreement where the buyer makes payments directly to the seller over a period until the full purchase price is paid, at which point the deed is transferred to the buyer. This financing option can be particularly appealing for buyers who may not qualify for traditional financing. Here are the key components and advantages of an Agreement-for-Deed for real estate transactions:

- Immediate Possession: Buyers can gain possession of the property and start living in or using it almost immediately, even though the deed will only be transferred after the full purchase price is paid.

- Flexible Terms: The payment schedule, interest rate, and down payment can often be negotiated directly between the buyer and seller, allowing for flexibility based on the buyer’s financial situation.

- No Traditional Lending Requirements: Since the agreement is between the buyer and seller, there’s often no need for a traditional mortgage, making this a viable option for buyers with credit issues or unconventional income sources.

- Simple to Execute: Agreements-for-Deed can be simpler and quicker to execute than traditional real estate transactions, potentially saving time and money on closing costs.

However, it’s crucial for buyers to be aware of the risks involved, such as the potential for losing investment and possession of the property if unable to complete the payments. Both parties should carefully draft the agreement to protect their interests, ideally with the help of legal and real estate professionals, to ensure a clear, fair path to property ownership.

Subject To (The Existing Financing)

Buying a property “Subject To” existing financing means acquiring real estate under the terms of the seller’s existing mortgage, without formally assuming the loan. The buyer takes control of the property and agrees to make mortgage payments on the seller’s behalf, but the original loan stays in the seller’s name. This strategy can offer significant advantages to both buyers and sellers in the right circumstances. Here are the key benefits and considerations:

- Immediate Financing: Buyers can bypass the traditional mortgage application process, closing costs, and potential financing delays, making the purchase process quicker and less expensive.

- Potential for Favorable Terms: If the existing mortgage has an interest rate lower than current market rates, the buyer benefits from those terms, potentially saving on interest payments over the life of the loan.

- No Large Down Payment: Since the transaction does not involve a new mortgage, buyers may not need to provide a large down payment, which is often a barrier to real estate investment.

- Risk of Due-on-Sale Clause: One significant consideration is the lender’s due-on-sale clause, which allows the lender to demand full repayment upon transfer of property ownership. Buyers and sellers must weigh this risk, as triggering this clause could require refinancing under less favorable terms.

“Subject To” transactions require thorough legal and financial due diligence to ensure that all parties understand their obligations and risks. This strategy can be a powerful tool for investors looking to expand their portfolios with minimal upfront capital, provided they navigate the associated risks and responsibilities carefully.

Utilizing Equity

For real estate investors, the equity built up in existing properties can be a powerful tool for further investment and portfolio expansion. Home Equity Lines of Credit (HELOCs) and cash-out refinances offer two pathways to access this equity, turning it into liquid capital that can be used for purchasing additional properties, renovations, or other investment opportunities. Both options have distinct features and advantages, making them suitable for different financial strategies and goals. This section explores how HELOCs and cash-out refinances work, highlighting how investors can leverage the equity in their properties to fuel their investment journey and achieve greater financial growth.

- Home Equity Lines of Credit (HELOCs): Revolving credit line based on home equity.

- Cash Out Refinances: Refinance the property and convert some equity to cash.

A Home Equity Line of Credit (HELOC) is a revolving credit line secured by the equity in your property, offering a flexible way to borrow money as needed. For real estate investors, HELOCs can be an invaluable tool for accessing funds for new investments, renovations, or covering operational costs. Here are the key features and advantages of utilizing HELOCs in real estate investment:

- Flexibility in Use: HELOCs provide a credit line that investors can draw from as needed, pay back, and then borrow against again, offering tremendous flexibility in managing cash flow for various projects.

- Interest-Only Payment Options: Many HELOCs offer interest-only payment periods, reducing the cost of borrowing during the initial years of the credit line.

- Competitive Interest Rates: Since HELOCs are secured by your property, they typically come with lower interest rates compared to unsecured lines of credit, making them a cost-effective borrowing option.

- Potential Tax Benefits: Interest paid on a HELOC may be tax-deductible if the funds are used to buy, build, or substantially improve the taxpayer’s home that secures the loan.

- Control Over Loan Amount: With a HELOC, you only borrow what you need, giving you control over the amount of debt you take on and the associated interest costs.

HELOCs offer real estate investors a dynamic financing tool, providing quick access to funds with the flexibility to use the capital as needed. However, it’s important to manage this type of financing carefully, as the loan is secured against your property, and improper use could lead to financial strain. By strategically leveraging the equity in their properties through HELOCs, investors can significantly enhance their ability to grow and diversify their real estate portfolios.

Cash-out refinancing allows real estate investors to refinance their existing mortgage into a new loan for more than they owe, pocketing the difference in cash. This strategy not only provides access to a substantial amount of capital but can also potentially improve loan terms. Here’s how cash-out refinancing works and why it might be a smart move for investors looking to leverage their property’s equity:

- Immediate Access to Capital: Cash-out refinancing provides a lump sum of cash up front, which can be used for property improvements, expanding investment portfolios, or consolidating debt.

- Potential for Better Interest Rates: If market conditions are favorable, refinancing can offer lower interest rates compared to the original mortgage or other types of debt, reducing the overall cost of borrowing.

- Long-Term Financing: Unlike a HELOC, cash-out refinancing offers a long-term loan, providing a stable, predictable payment schedule that can be easier to manage within an investment strategy.

- Debt Consolidation: Investors can use the funds to pay off higher-interest debts, streamlining finances and potentially improving cash flow.

- Tax Deductible Interest: Interest paid on the cash-out portion used for home improvement or purchasing additional properties may be tax-deductible, enhancing the financial benefits.

While cash-out refinancing can offer a significant financial boost to real estate investors, it’s important to consider the risks, such as extending the loan term or increasing the amount owed. Careful planning and market analysis are crucial to ensure that cash-out refinancing aligns with long-term investment goals and financial health.

Conclusion: Navigating Real Estate Financing with Confidence

The journey through real estate investment is filled with opportunities to leverage various financing options, each offering unique benefits and considerations. From government-backed loans that provide accessible entry points to the market, to traditional and alternative financing methods that cater to specific investment strategies, understanding these options is crucial for success. Additionally, creative financing techniques and leveraging equity in existing properties can open new doors for investment and portfolio growth.

As investors navigate these diverse financing paths, it’s essential to assess each option carefully, considering factors such as interest rates, terms, flexibility, and potential risks. By doing so, investors can make informed decisions that align with their investment goals and financial situation. Whether you’re a seasoned investor expanding your portfolio or a newcomer making your first foray into real estate, the right financing strategy can be a powerful tool in achieving your investment objectives.

Remember, while the landscape of real estate financing offers numerous pathways to success, it also demands diligence, foresight, and a willingness to adapt to changing market conditions. With the right approach and a clear understanding of the financing options available, real estate investors can build a strong foundation for long-term growth and profitability.