Pro Tip: Listen to the podcast below and while you’re listening follow along with the charts below. Then, when you’re done, copy the  Scenario

Scenario

Welcome to the Real Estate Financial Planner™ Podcast. I am your host, James Orr. This is Episode 10.

Today we’re going to continue with  Norm and Norma’s Norm and Norma

Norm and Norma’s Norm and Norma

It turned out that taking the extra time to save up an extra 5% down payment to get the lower interest rate and borrowing less resulted in being able to achieve financial independence faster… and arguably safer.

For many listeners this was counter-intuitive… surely buying properties faster would allow them to achieve financial independence faster. It turns out that for their specific situation and market conditions that was not the case.

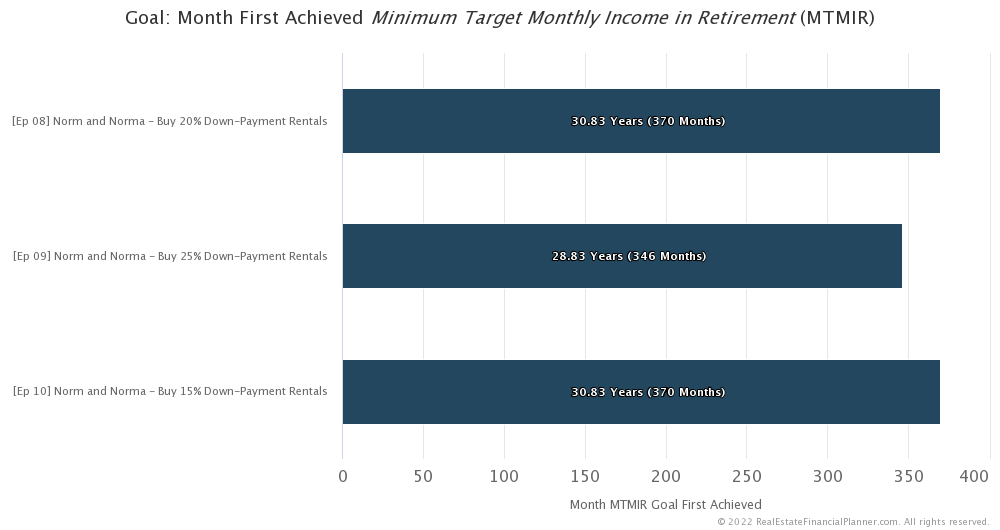

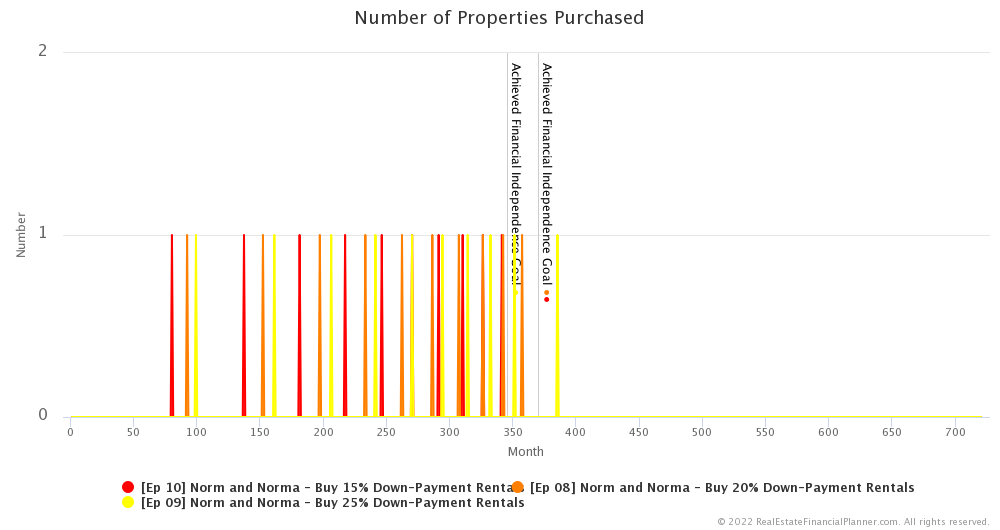

But what if they are able to buy 10 properties faster by only saving up 15% for down payments? How long will it take them to achieve financial independence if they put 15% down when buying rentals?

Financial Independence

Well… I’m not going to keep you guessing if putting 15% down is better or worse… instead I’m just going to tell you: putting 15% down works out to be the same amount of time to achieve financial independence as putting 20% down.

But, that’s not the end of the story. Because it turns out that putting 15% down is very different in a lot of ways than putting 20% down or 25% down even if… in these very specific assumptions for Norm and Norma

Down Payments, Interest Rates and Private Mortgage Insurance

First, let’s talk about down payments, interest rates and private mortgage insurance.

The following were based on real mortgage quotes right before I made these Scenarios for Norm and Norma

But, for this episode:

- If

- PMI is about .47% of the loan amount each year or about $124.84 per month if they happened to buy the property in the first month (which they didn’t).

- The PMI would remain until they got below 80% loan-to-value and then it would go away. At that point their cash flow would improve by the amount they had previously been paying for PMI.

- PMI is a cost of “financing” the down payment. If they had put 20% down, they wouldn’t have had PMI. But because they put 15% down, they do have it.

- The questions

- Are the benefits of buying a little earlier worth the extra expenses of a slightly higher interest rate, borrowing a little more and having PMI?

- Will the combination of appreciation, debt paydown, cash flow and Cash Flow from Depreciation™ for the amount of time they’d save by being able to act earlier good enough to pay the premium of these extra expenses?

- With

- So,

- And remember, this is for just 1 property… and they’re buying 10. And, it was only the first 15% down property that they bought 12 months sooner than putting 20% down… many of the additional properties are bought with an even greater headstart.

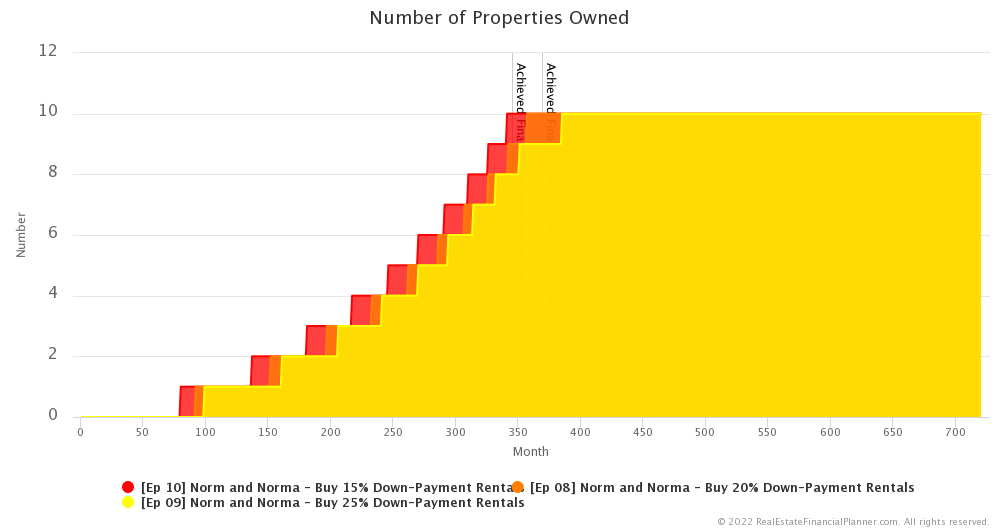

As you might expect they could buy properties sooner with 15% down than 20% down payments and 20% down payments are faster than 25% down payments.

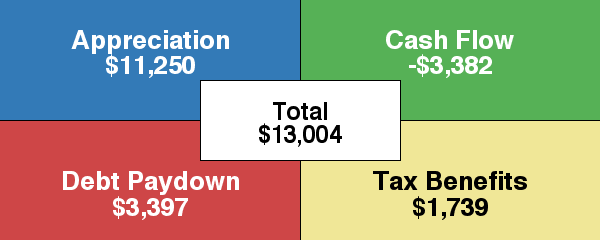

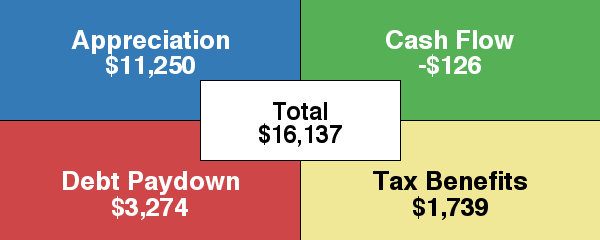

If we look at the Return in Dollars Quadrant™, we can see that the advantages of buying properties early is mostly found in the appreciation and debt paydown half. Neither of those directly count toward whether they achieve financial independence. They count toward net worth.

If they decided to sell the properties later or even refinance them, they could gain some of the benefit of early purchases but in this episode we’re focused on them just buying 10 rentals with a variety of down payments. In future episodes, we can come back and look at what if they sold off some or refinanced some rentals and paid off other rentals or, alternatively, invested the proceeds into the stock market or some other investment that counted toward achieving financial independence.

Let’s get back to the down payments, interest rates and PMI:

- We started to discuss

- If

- And, finally, if

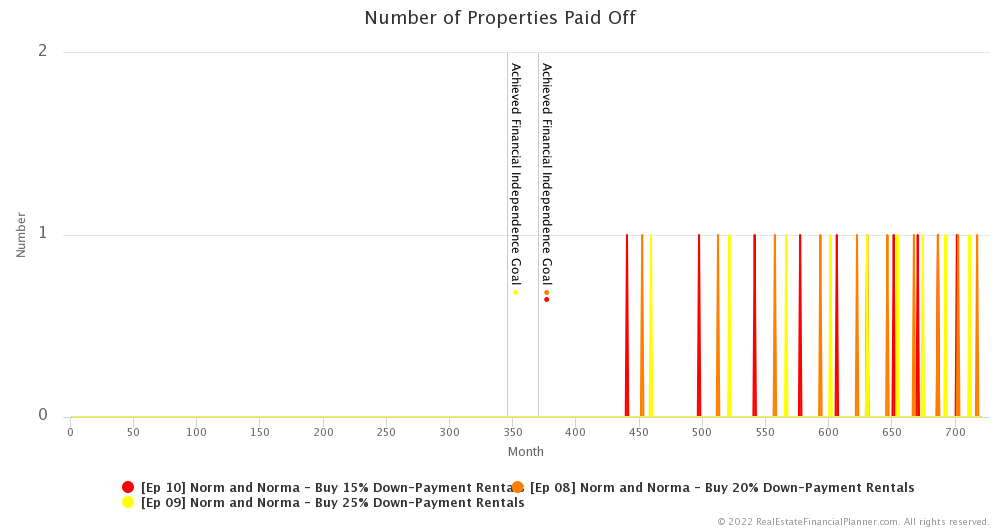

Number of Properties Paid Off

If you assume you’re going to just make the regular monthly payments on all your rentals, a magical thing happens when you get to buy properties earlier by putting 15% down over 20% down or 25% down… do you know what that magical thing is? You get to have paid off properties earlier. If you bought your first property 12 months earlier, you get a paid off property that same 12 months earlier. Why? Because 30-year amortizing loans pay off in… well… 30 years if you make all your payments as scheduled.

But, since they achieve financial independence before any properties get paid off, having paid off properties does not come into play when determining when they achieve financial independence. It does come into play with their standard of living after they achieve financial independence.

A paid off property with no mortgage, means they get better cash flow on that property. Better cash flow means they could… at least in theory… increase how much they spend each month and therefore have a higher standard of living.

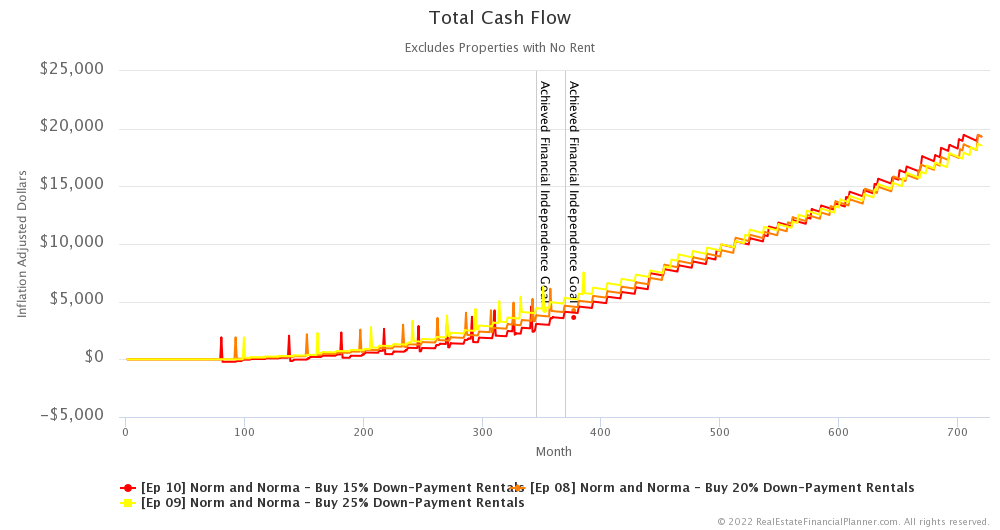

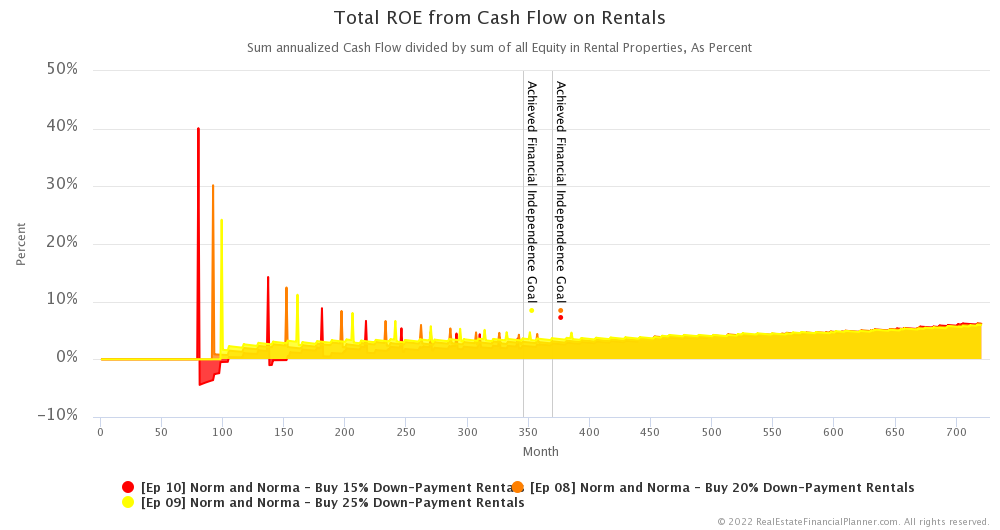

Cash Flow

Of course, all three strategies… regardless of down payment amount… end up with 10 unmortgaged rental properties at some point and then they all have very similar cash flow.

But before they’ve paid off properties in all 3 Scenarios, the cash flow is best for 25% down payments then 20% down payments and finally, the worst cash flow is 15% down payments.

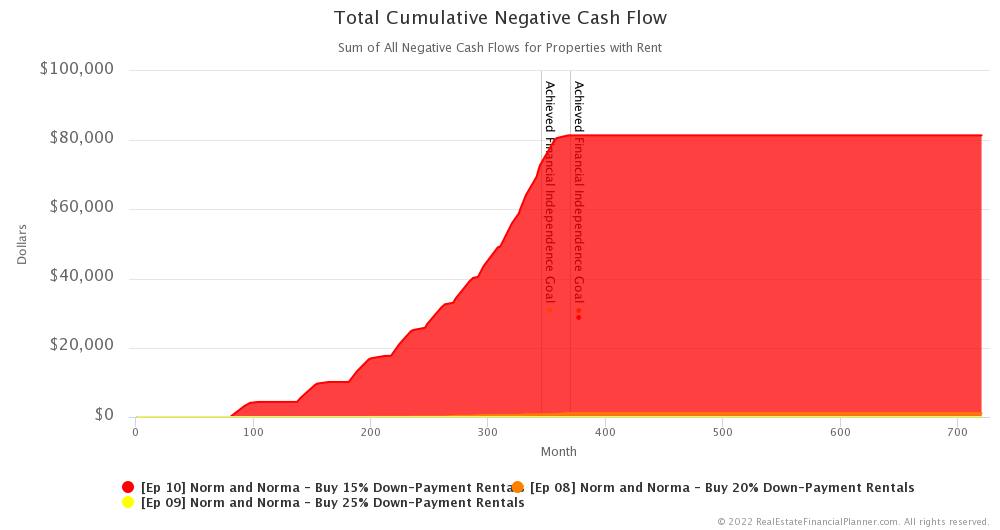

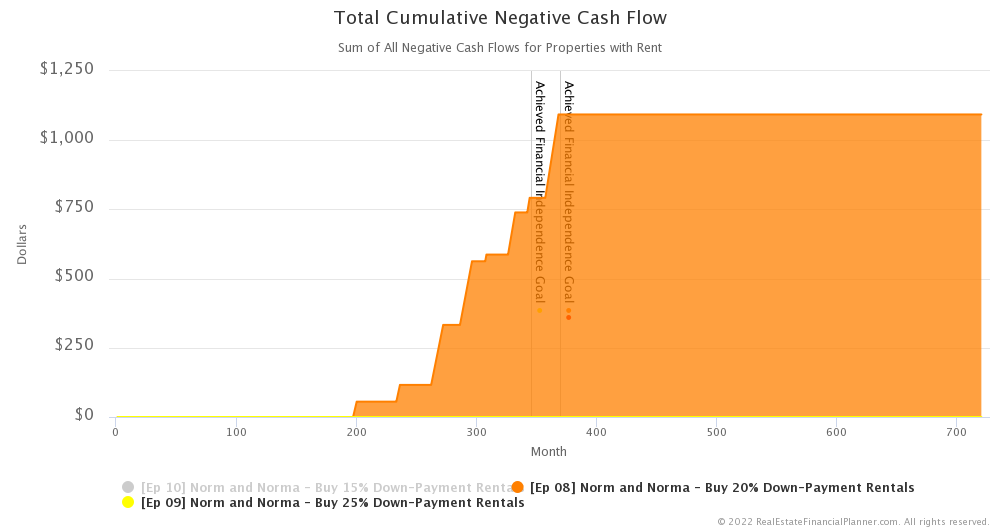

Negative Cash Flow

In fact, they experience what I’d describe as pretty significant negative cash flow when they put 15% down.

Significant is subjective, but maybe you too would consider over $80,000 total… across all 15% down payment properties and the entire 60 year run as significant… because that how much it was.

Compare $80,000 in cumulative negative cash flow for 15% down payments to less than $1,200 total for all 10 properties combined over the entire 60-year term for 20% down payment rentals and zero negative cash flow with 25% down payments.

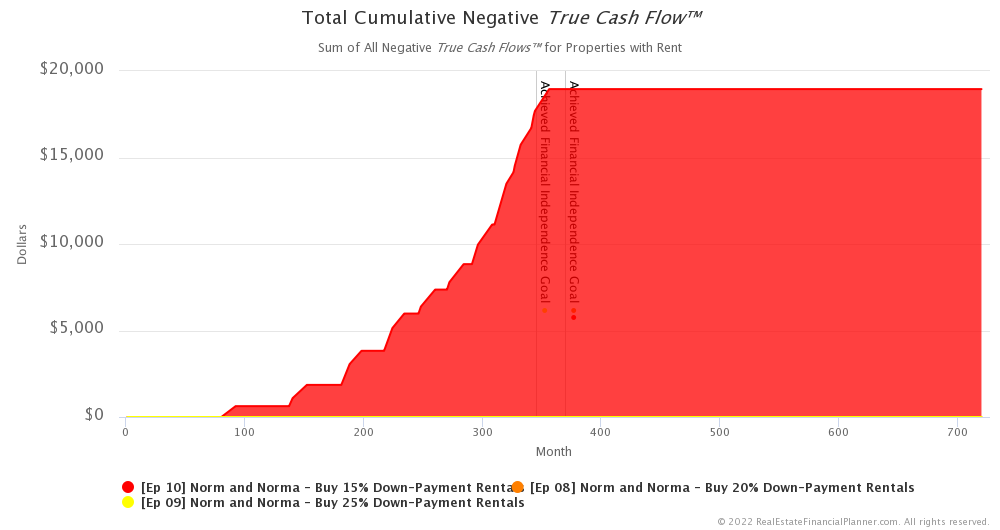

Negative True Cash Flow™

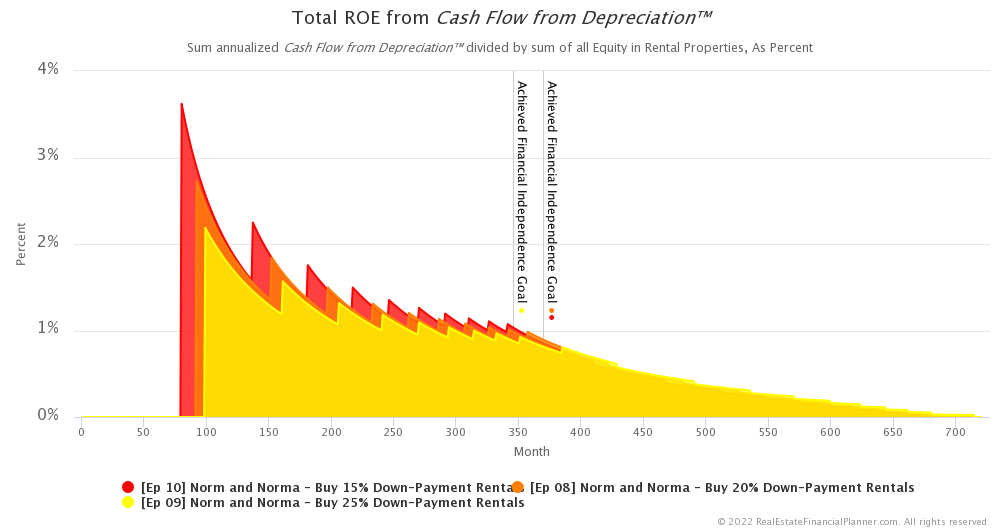

Another way of looking at negative cash flow is when we consider negative cash flow but only when we don’t have enough tax benefits to offset that negative cash flow. In other words, when cash flow is still negative when we add in Cash Flow from Depreciation™.

When we combine cash flow with Cash Flow from Depreciation™ we call that True Cash Flow™.

How much negative True Cash Flow™ would Norm and Norma

Heck, even $80,000 in negative cash flow instead of coming up with 10 times the $18,750 difference between 15% down and 20% down seems like a deal. They could decide to “finance” $80,000 in negative cash flow over about 30 years instead of coming up with $187,000… that’s 10 times the $18,750 difference between 15% down and 20% down… as they buy 10 properties.

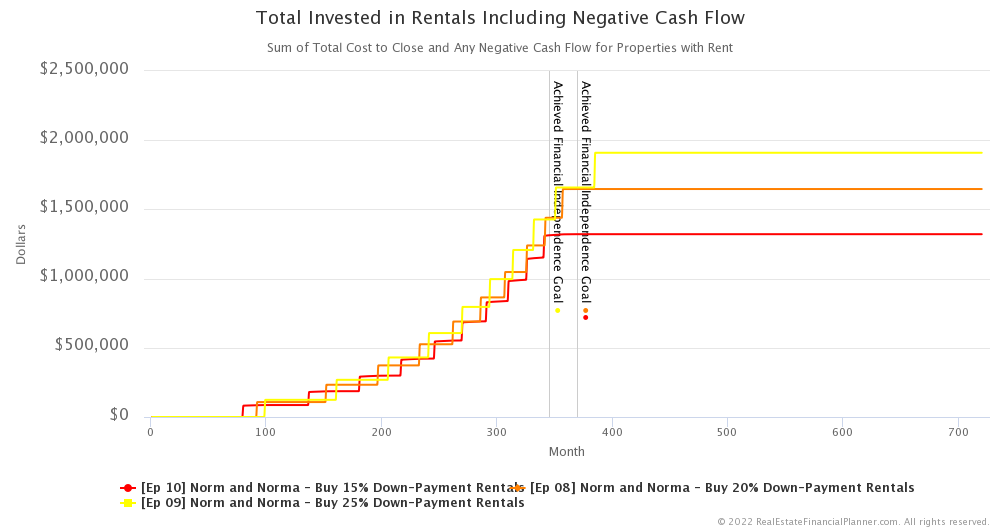

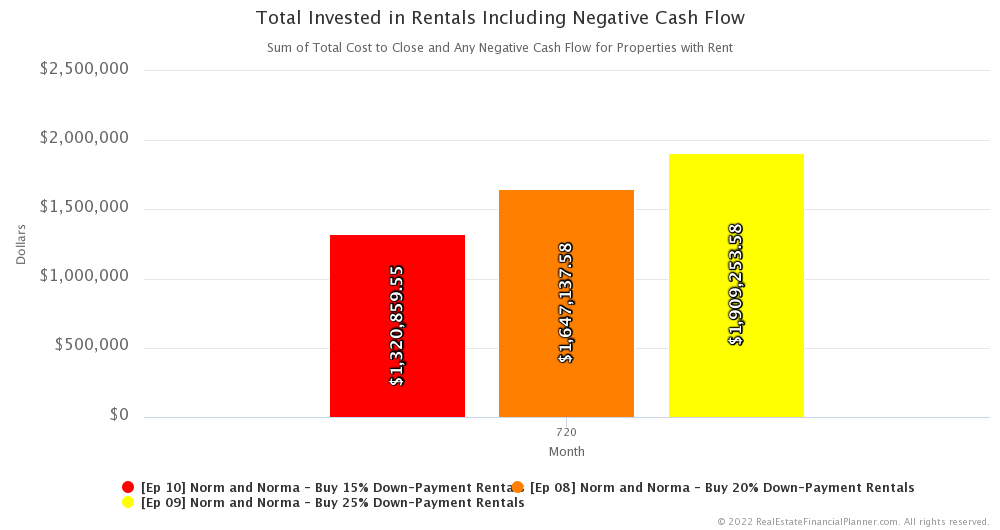

Total Invested in Rentals Including Negative Cash Flow

Another interesting way I like to look at this is to consider the total amount they needed to invest to acquire their properties including any negative cash flow.

That would be down payments and closing costs including points to get the loan plus any negative cash flow on the properties.

If we look at that, the largest investment made is when they put 25% down. That’s right, they end up investing more by putting 25% down than putting 20% down and 15% down.

- For 15% down payments, they’d invest about $1.32 million dollars including that $80K or so in negative cash flow.

- For 20% down payments, they’d invest about $1.65 million dollars.

- And, for 25% down payments, they’d invest about $1.91 million dollars.

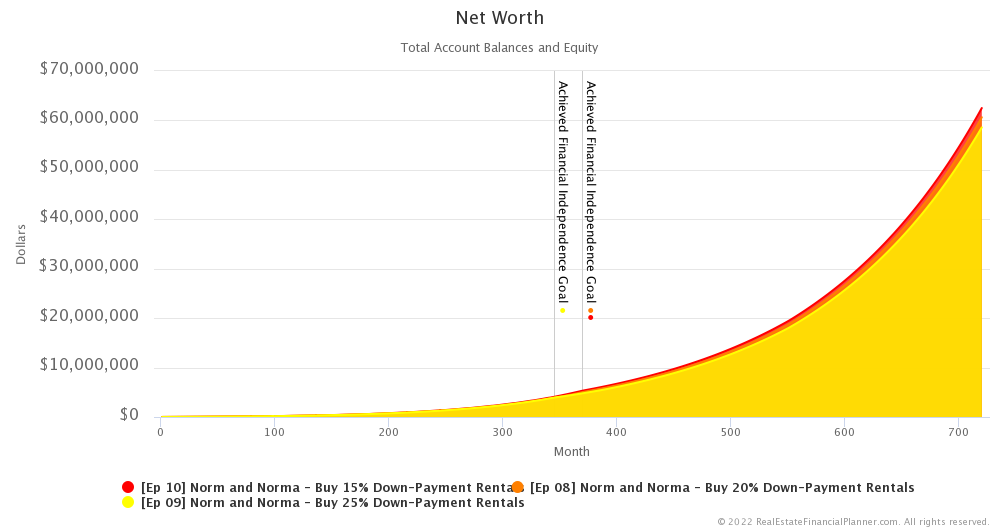

Net Worth

But enough about how much they invested, let’s look at net worth.

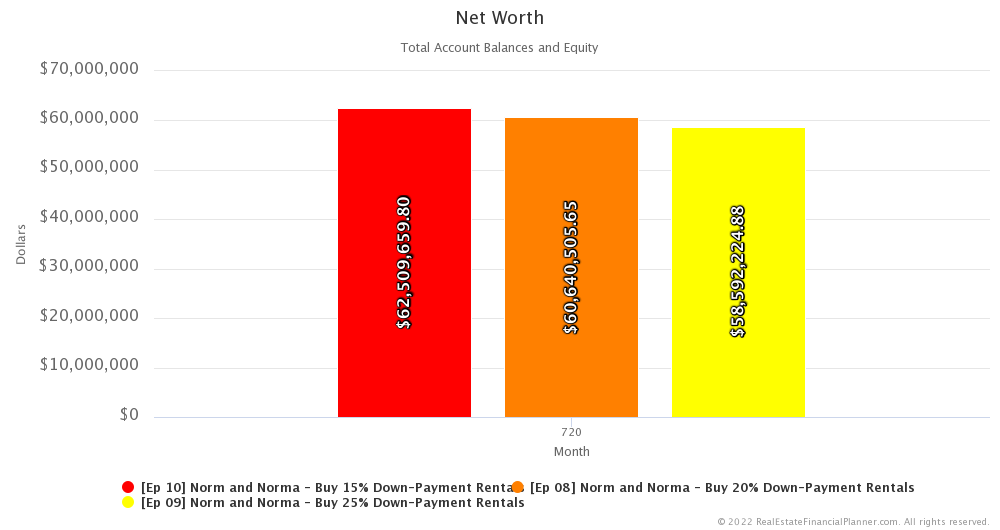

Even though putting 25% down gets them to financial independence faster, the less they put down… at least with these static assumptions in this episode… the more net worth they end up with.

At the very end of our modeling after 60 years, putting 15% down leaves them with about $62.5 million in net worth.

Compare that to $60.6 million for 20% down payment and $58.6 million for 25% down.

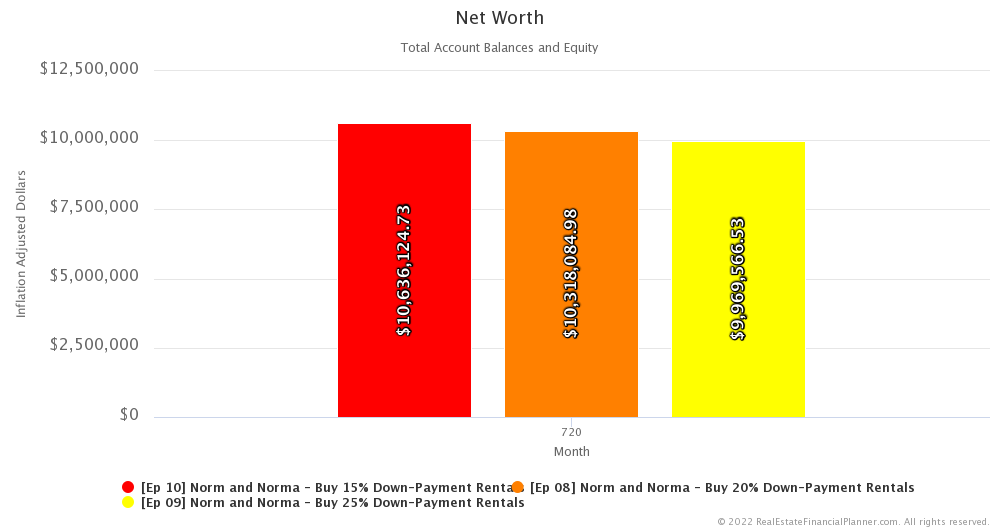

Now, those are in inflated future dollars 60 years in the future.

If we adjust those numbers back to today’s dollars, putting 15% down gives them a net worth of $10.64 million compared to $10.32 million for 20% down. That’s about a $300K difference… not zero, but a relatively small percentage of $10 million in net worth. Putting 25% down leaves them with about $350K less than putting 20% down.

In general, it seems that buying properties earlier helps with net worth as we suspected previously when we discussed the extra appreciation, debt paydown and tax benefits. But some of that is offset by some negative cash flow with the extra PMI and borrowing more.

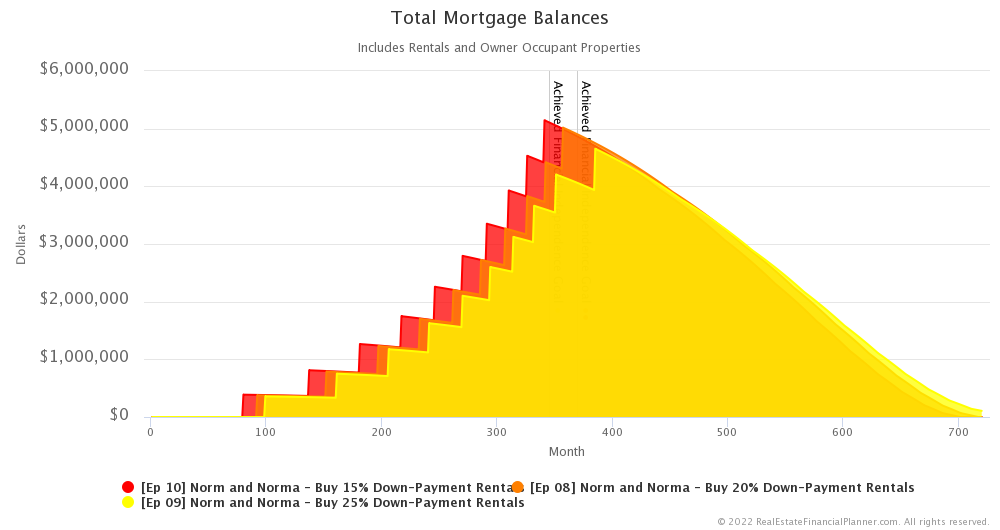

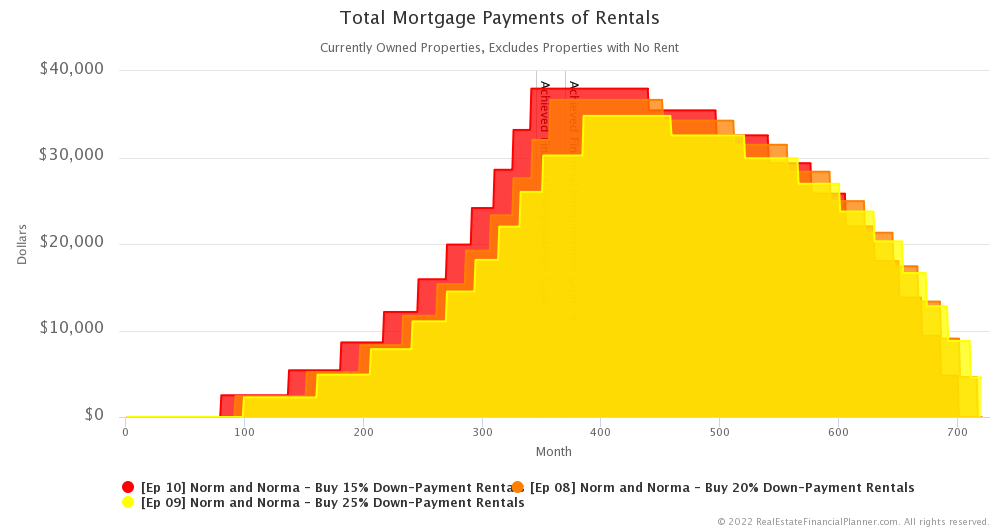

Mortgage Balances and Mortgage Payments

Speaking of borrowing more, what about mortgage balances?

As you’d expect, putting only 15% down gives you a higher mortgage balance. This compounds when they buy 10 properties. Such that they have the highest overall mortgage balance for 15% down with the next highest being 20% down and finally, the smallest mortgage balance for all properties happens when they wait to put 25% down.

A similar phenomenon occurs with mortgage payments. Borrowing more and at a higher interest rate results in higher mortgage payments.

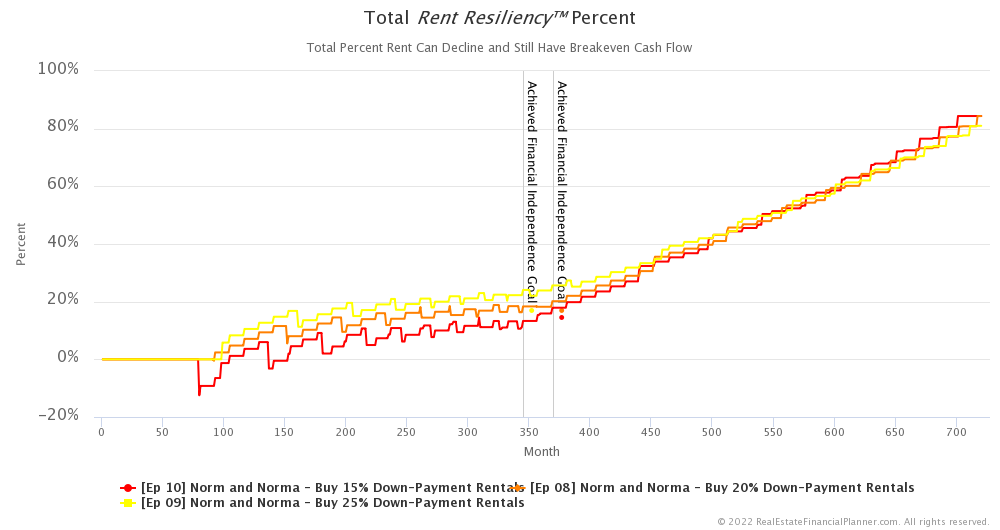

Rent Resiliency™

With higher mortgage payments comes less cash flow and therefore worse Rent Resiliency™. When they put 15% down, they increase their risk should rents decline. The least risky strategy in terms of Rent Resiliency™ is putting 25% down… they can afford to see rents decline the most before they have negative cash flow if they have the lowest monthly payments.

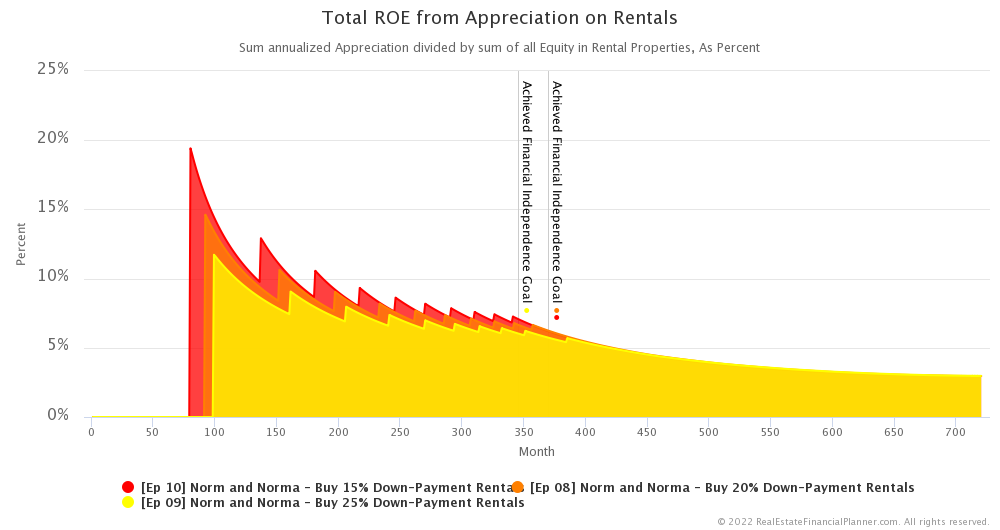

Return on Equity

But, here’s something interesting… since putting 15% down means they have less equity in the property then when we measure things like appreciation that is the same regardless of how much they put down, the return on equity for those things tends to be better.

For example, if a property goes up $10,000 in value in a year from appreciation then it doesn’t really matter whether they put 15% or 20% or 25% down. They still earned $10,000 in appreciation. However, they earned that $10,000 on a smaller amount of equity in the property if they put 15% down than if they put 20% or 25% down. The more they put down, typically the more in equity they have.

This is similarly true for things like return on equity from debt paydown and return on equity from the tax benefits of depreciation.

The same cannot be said when we look at the return on equity from cash flow.

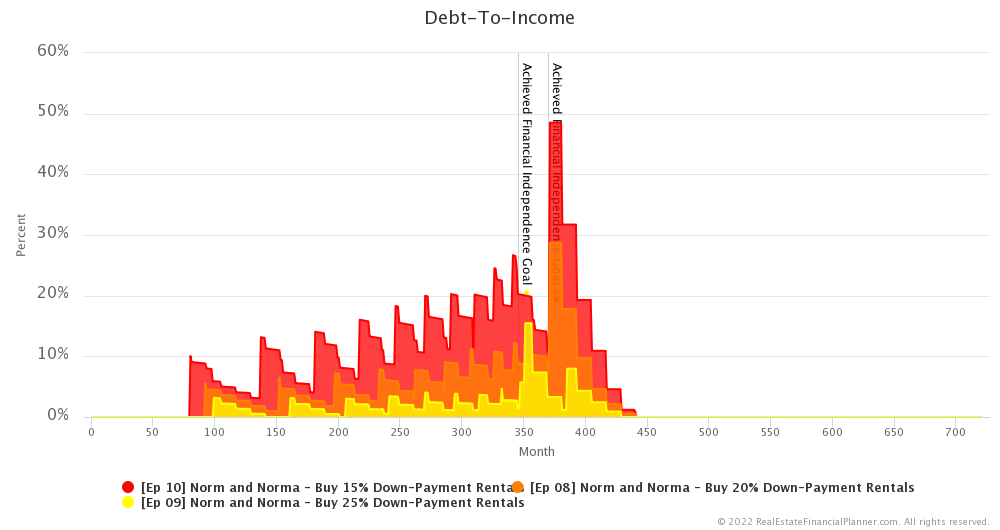

Debt-To-Income

The cash flow when they put 15% down is often negative… especially early on.

With negative cash flow, that hurts their debt-to-income ratio but not really enough to impact their ability to qualify for purchasing additional rentals. If they had other debt including an owner-occupant mortgage this might have a much more significant impact in their ability to qualify. We may return to this idea in a future episode when we see the impact of Norm and Norma

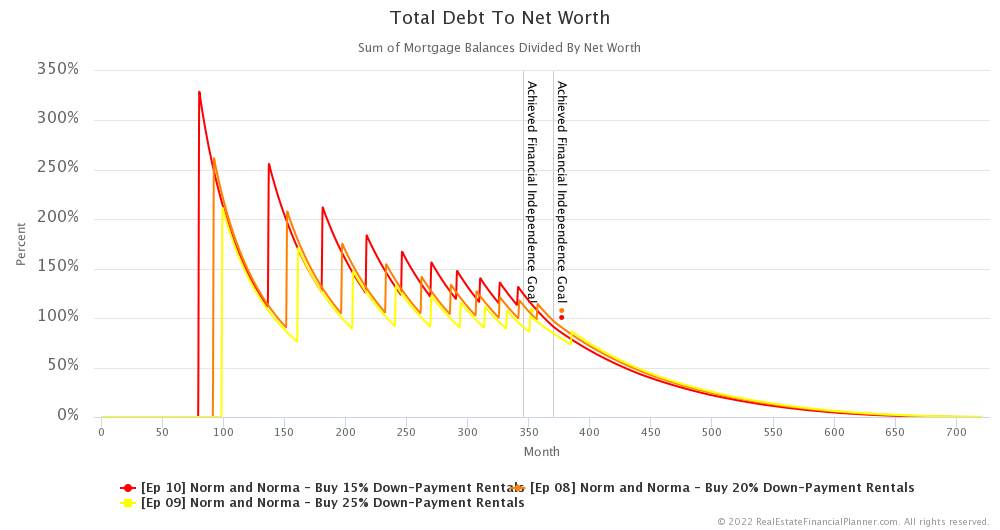

Total Debt To Net Worth

But, for this episode let’s consider how risky it is to put 15% down versus 20% or 25%.

We already discussed one way of measuring risk: rent resiliency or the ability for rent to drop without having negative cash flow. But that’s not the only way we measure risk.

Another way is the total debt they have versus their net worth.

Putting 15% down and buying properties sooner means they tend to have more debt than putting 20% or 25% down and buying a little slower.

And, it turns out that means their measure of risk in the form of total debt to net worth is worse and worse earlier than putting more down. This tends to be true for most of the time leading up to achieving financial independence. However, because they keep buying properties later when putting 25% down, the risk stays very slightly higher later when they put 25% down.

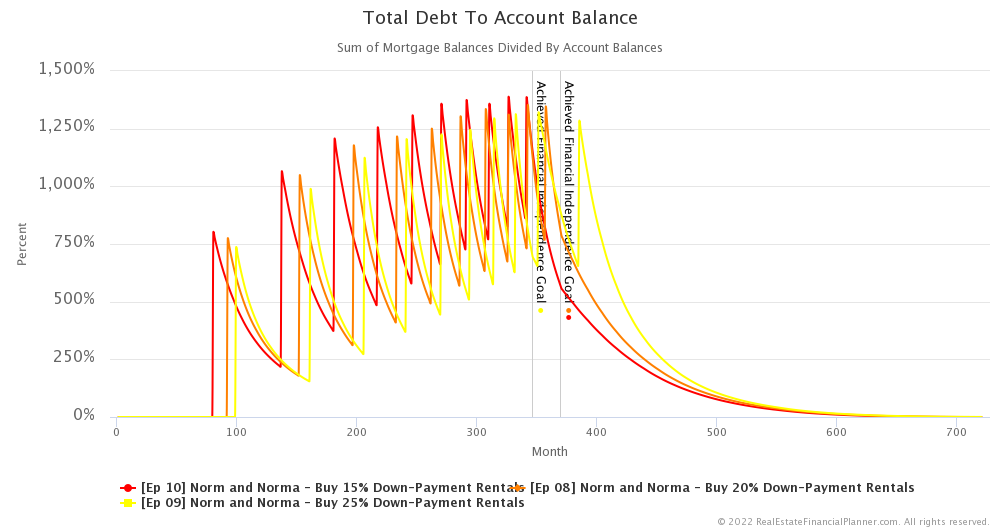

Total Debt to Account Balances

Another variation of measuring risk involving the debt load is the total debt compared to how liquid they are with money in their accounts… and by this we’re explicitly excluding net worth from property equity.

We call this total debt to account balance and a similar phenomenon occurs here… put less down, increase your risk.

The exception is that they’re buying properties later when putting 25% down so the risk lingers longer with 25% down then putting 15% or 20% down.

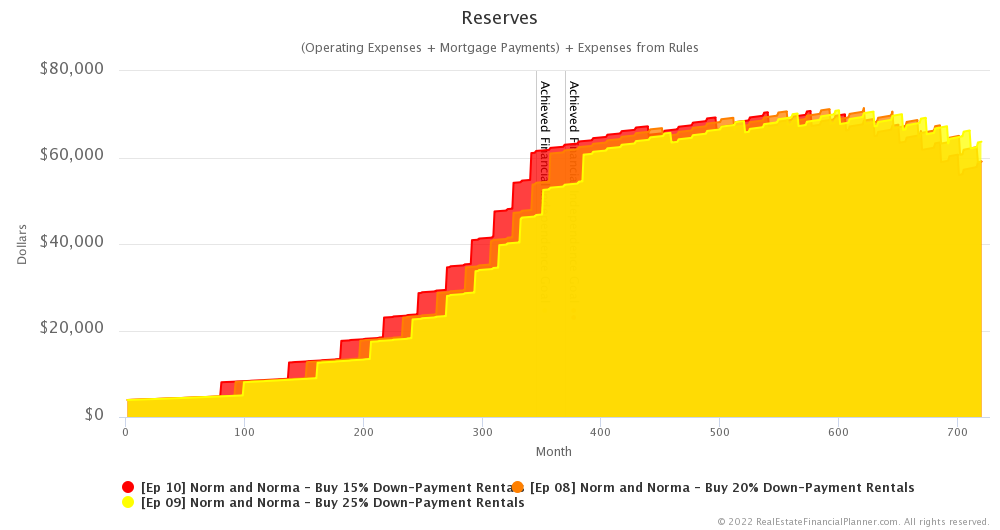

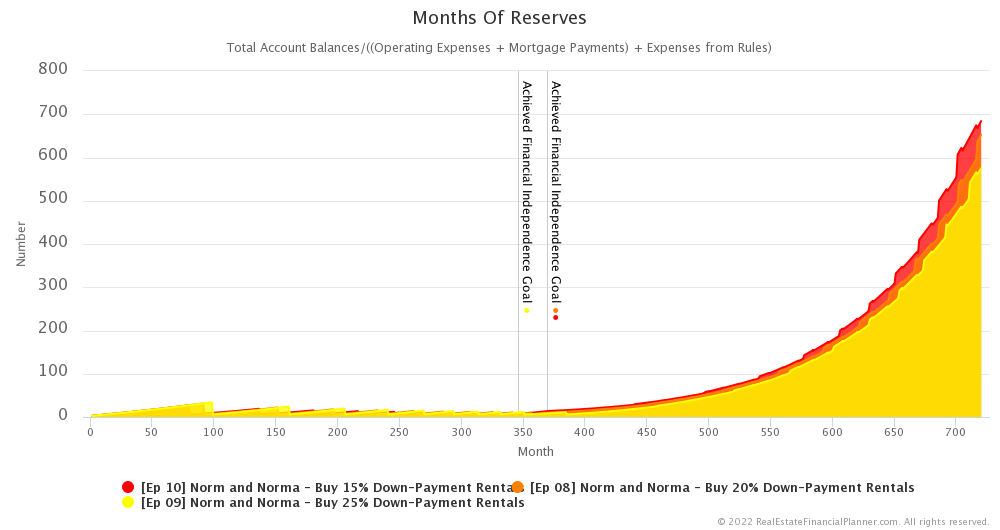

Reserves

Besides the debt based measures of risk, I also like to consider reserves as a measure of risk.

In general, when they put less down, they need to set aside more dollars for a single month of reserves. A higher mortgage payment and PMI associated with putting 15% down means that they need to have a higher dollar amount set aside for a single month of reserves.

However, in all three down payment cases, they are making certain they’ve got 6 months of reserves saved up before they buy their next rental. That’s in addition to the down payment and closing costs required to buy the next property.

That means that the risk as measured by the number of months of reserves is going to be similar with the static assumptions in this episode. In theory, they shouldn’t ever dip below 6 months of reserves.

When we do the advanced modeling though this may not always be the case. Check out the Advanced Real Estate Financial Planner™ Podcast to see the impact… if any.

Conclusion

In conclusion, putting 15% down instead of 20% or 25% does allow them to buy properties sooner. And, it ultimately gives them a slightly higher net worth. Not a significantly higher net worth but a little higher.

However, it comes with an increase in risk in just about every measure except the number of months of reserves which is similar because they refused to buy properties without 6 months of reserves in any of the 3 different down payment scenarios.

Next Episode

In all three of these down payment scenarios, Norm and Norma

Also, be sure to check out the Advanced Real Estate Financial Planner™ Podcast to see how having variable property appreciation rates and rent appreciation rates, variable mortgage interest rates, variable inflation rate and variable stock market rates of return impacts Norm and Norma

I hope you have enjoyed this Episode about Norm and Norma

Get unprecedented insight into Norm Norma’s Scenario with dozens of detailed, interactive charts.

Inside the Numbers

Watch the Inside the Numbers video to see exactly how we set up their Scenario

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 08 Norm and Norma - Buy 20% Down-Payment Rentals with 2  Accounts, 1

Accounts, 1  Property, and 6

Property, and 6  Rules.

Rules.

Or, read the detailed, computer-generated, narrated  Blueprint™

Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 09 Norm and Norma - Buy 25% Down-Payment Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 10 Norm and Norma - Buy 15% Down-Payment Rentals with 2 Accounts, 1 Property, and 6 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Podcast Episodes

The following are the podcast episodes for variations of Norm Norma’s

More posts: Norm Episode