Pro Tip: Listen to the podcast below and while you’re listening follow along with the charts below. Then, when you’re done, copy the  Scenario

Scenario

Welcome to the Real Estate Financial Planner™ Podcast. I am your host, James Orr. This is Episode 3.

Today we’re going to continue with  Andrea’s

Andrea’s

Previously, in episodes 1 and 2, Andrea

They suggested that she invest in stock index funds instead of real estate.

So, in this episode, we will look at Andrea

How long will it take for her to achieve financial independence without acquiring rental properties?

She has $100,000 from the divorce to start with.

She buys a property to live in with 5% down. Properties are about $250,000 so about 5% of that is about $12,500 plus some closing costs.

After she buys the house, she’ll have just under $85,000 left over to invest in stocks in this case.

What return can she get in the stock market?

Well… we’re assuming she is getting the same 8% return on her money that we’ve been assuming she’s earning on any money she had not yet invested in properties in the previous Scenarios.

Something to think about: we’re also assuming that inflation is happening at 3% per year.

That means that really the stock market return… net of inflation… is only 5% per year.

In other Scenarios with Andrea

What does this mean in Andrea’s

Well, it means at least 3 things:

First… it means that it is slightly easier for her to buy properties later in the Scenario. Property values are going up each year, but her wages from her accounting job and the return from the stock market mean that the price of properties seems to be a slightly better deal the longer we go.

We explore this idea with more realistic assumptions in the Advanced Real Estate Financial Planner™ Podcast with variable inflation and appreciation rates.

We will also explore this more in future episodes of this podcast as we change our assumptions for price appreciation and inflation in other Scenarios.

In many cases when I do modeling for myself or with clients, I often assume that property prices and inflation are the same 3% per year. My justification for this is based on some analysis done by Al on his Observations and Notes blog using Robert Shiller’s housing price index data.

In his blog post he writes:

“So, what’s the result of over 100 years of ups and downs in the housing market? The bottom line, somewhat surprisingly, is that the average annual price increase for U.S. homes from 1900 to 2012 was only 0.1%/year after inflation! And, that includes the possibly one-of-a-kind increase in prices caused by the baby boom and G.I. Bill.”

But I digress. I was telling you about the 3 ways that having property values go up slightly slower than inflation means to Andrea

Second… is that cash flow on properties she buys later is better. We’re assuming that rents keep pace with inflation. Inflation is calculated using an estimated form of rent as part of the formula… and a relatively large percentage of the formula I might add.

So, when rents go up a little faster than home prices… 3% per year versus 2% per year… cash flow on later houses is a little bit better to start then on the houses that she bought earlier.

Of course in the Advanced Real Estate Financial Planner™ Podcast and in other Scenarios on this podcast we don’t use these same assumptions.

Third… is that equity in her properties is growing slower than if property values were going up with inflation. Equity is the difference between what the property is worth and what she owes. So, if the value of the properties are not going up as fast, that means that her equity is not growing as fast.

This makes it a more conservative modeling of what historical data might suggest.

Why did I even go down this rabbit hole? Oh yeah… it was because I mentioned that the stock market rate of return of 8% is really more like a net gain of 5% per year when you take into account for inflation. But, I wanted to make a similar comparison for property appreciation rates and rent appreciation rates for this particular analysis with Andrea

Back to our story… so when does Andrea

Well, let’s break that down a bit.

Her retirement income would need to consist of 3 things:

- Passive income like social security, pensions or annuities. In her case, she doesn’t have a pension or annuities, but she will collect social security starting at age 65. That’s about $1,423 per month in today’s dollars.

- Net cash flow after all expenses on rental properties. In other Scenarios this was a major source of income in retirement for her. However, in this Scenario for this episode it is zero. She has no rental properties… just the property she lives in… and therefore no rental income.

- The yearly safe withdrawal rate of her invested assets. This is going to be the primary source of her retirement income. The financial advisor she met with suggested she can “safely”… and I use that in quotes because we will really need to dig into that in a future episode… but the advisor suggests she can safely withdrawal 4% of the initial amount she has invested each year. And, she can adjust that amount up by inflation each year.

So, if she had $1M dollars, she could take out $40,000 per year in the first year and $40,000 adjusted up for inflation in year 2 and so on.

So, those are the 3 sources of retirement income for Andrea

First, she’s living on $4,000 per month… that’s what she is earning from her job. We assume that her wages from her job are also going up with inflation. That means that even though her income is going up, so are her expenses and that she’s really just maintaining her same standard of living even though she’s earning and spending more money with each passing year.

That means… at first blush… she needs to replace $4,000 per month from her retirement income to be considered financial independent. But, that’s not exactly true for 2 reasons.

Reason #1: it is really the $4,000 adjusted up for inflation that she needs to replace.

OK… that makes sense… to have her retirement income keep her living the same standard of living she has been living at, she needs to replace $4,000 per month ADJUSTED UP for inflation. Got it.

But, that’s not the only thing we need to adjust for.

Reason #2 The $4,000 per month she is living on includes her mortgage payment… the principal and interest part of the payment associated with the loan. I’m not talking about taxes and insurance… she will always have property taxes and she will opt to always keep insurance on the property… even though she could… in theory… choose to not be insured when she no longer has a mortgage.

What I’m really wanting to talk about though is that principal and interest payment with the loan. That mortgage payment on the property she is living in is just over $1,000 per month.

There two very interesting things about that mortgage payment for Andrea

Let’s talk about the payment while she has the loan.

When she first gets the mortgage, she is earning about $4,000 per month from her job and the payment is about $1,000 per month. So, about 25% of her income is going towards the payment on the loan.

However, skip ahead 20 years. 20 years from now she’ll be earning a lot more than $4,000 per month. In today’s dollars it is still $4,000 per month but in future dollars it is more like $7,000 per month.

But what happens to the $1,000 per month she’s paying on the loan? It stays the same.

So, instead of it being 25% of her income… $1,000 in payment on a $4,000 paycheck… it is more like just under 14% of her paycheck. That means she has more money to do with as she pleases.

Now, all her other expenses do increase as well… property taxes go up, property insurance goes up, food costs go up, gas costs go up and so on. But a full 25% of her budget does NOT adjust with inflation… that payment on her mortgage… as long as she does not refinance or buy a new house… will remain fixed for 30 years.

And then do you know what happens in 30 years? Poof! It disappears completely.

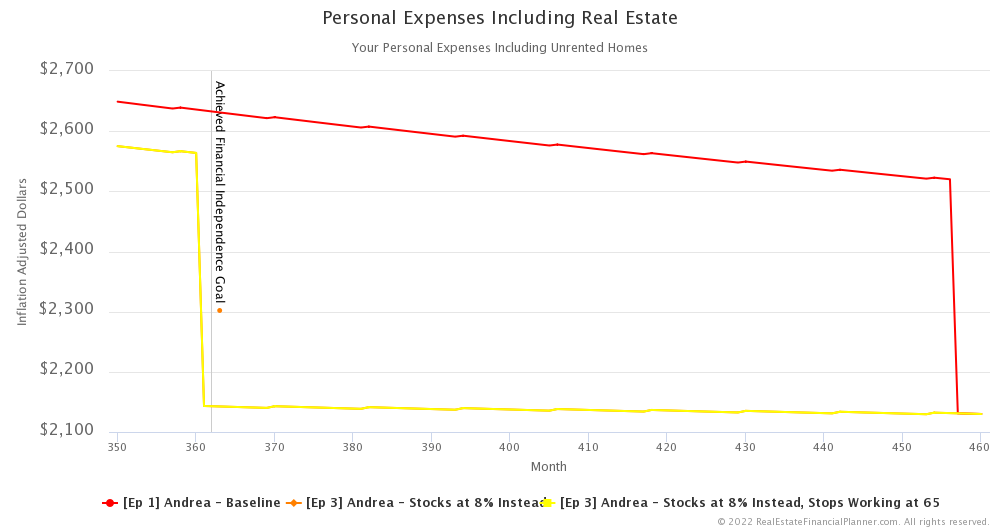

In month 361 she instantly frees up about $1,000 per month in expenses because she no longer has a mortgage payment due at all.

So, really… once she gets to month 361 she doesn’t need to replace $4,000 per month… adjusted for inflation… she only needs to replace about $3,000 per month… adjusted for inflation… because she no longer has that $1,000 expense from the mortgage payment.

I mention this because in previous Scenarios in other episodes, she is buying a bunch of properties and it is the LAST property she buys that she is living in. So, it is the last property she buys that she needs to wait until it is paid off to experience this reduction in need for her to be financially independent. Since she buys 8 properties before this one… at least a year apart each… that’s 8 more years until she experiences the benefit of no longer having that mortgage payment on the property she is living in.

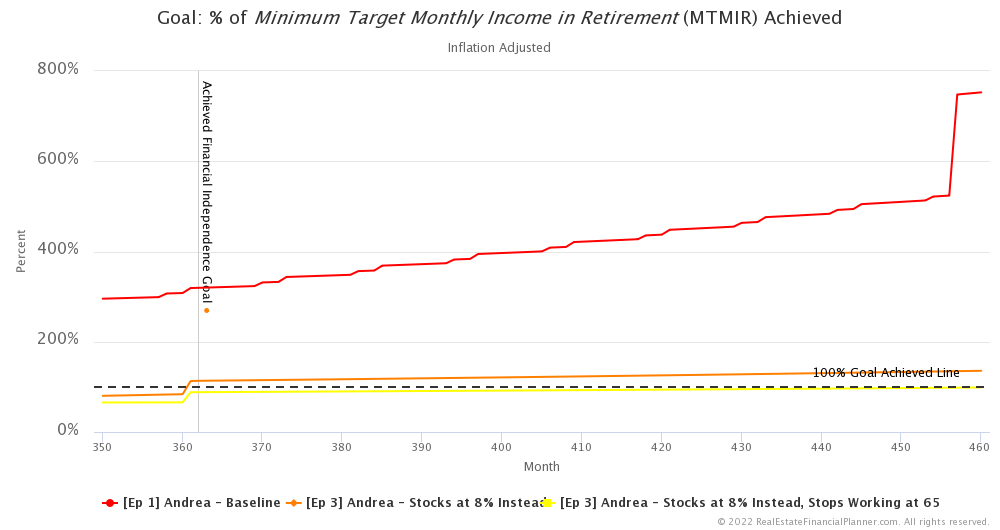

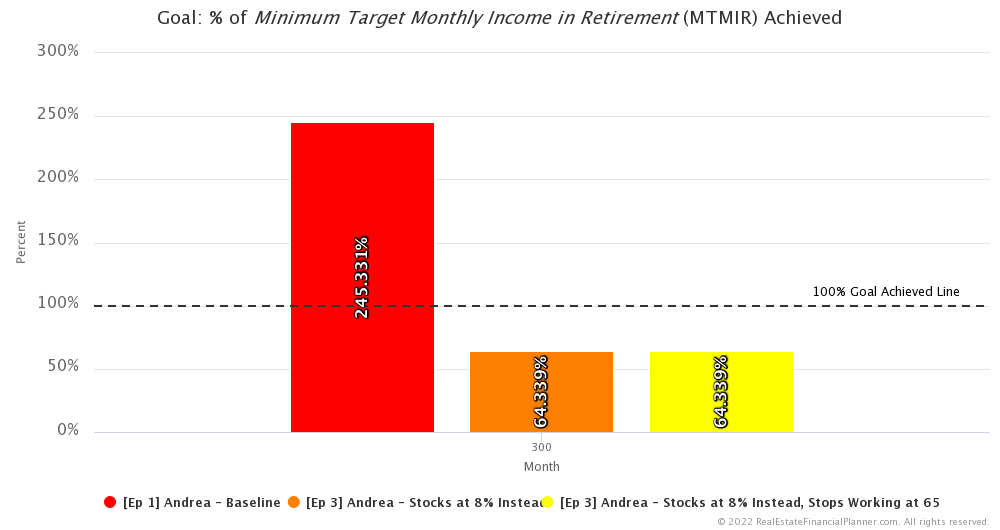

OK, so… she’s financially independent when the sum of all her passive income… which she just has social security starting at age 65… plus net cash flow from rentals… which she has none if she’s just investing in stocks… and the yearly safe withdrawal rate of her invested assets exceeds her living expenses… and if it is beyond month 361… that’s less her previous mortgage payment.

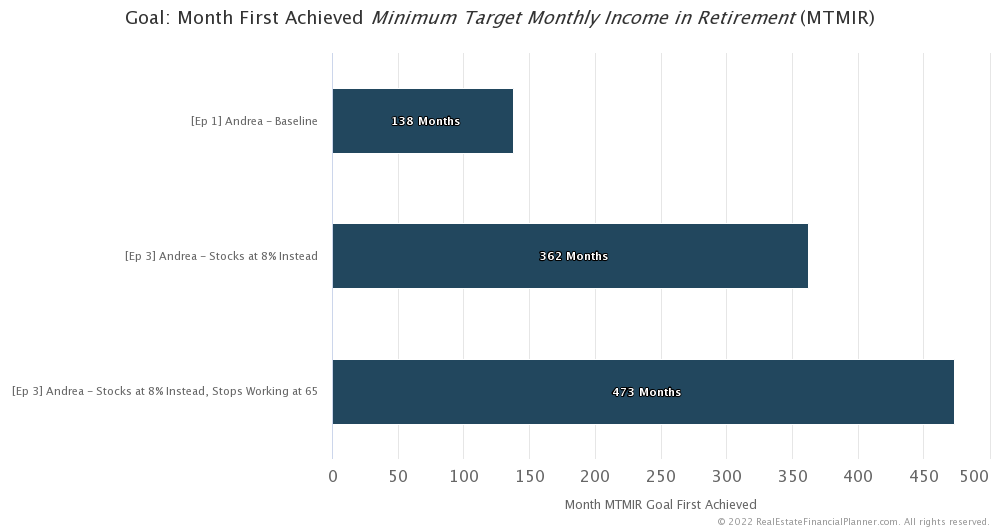

I ask again… when does she achieve financial independence just investing in stocks? It turns out, it is month 362… just after her mortgage is paid off. She’d be just over 70 years old by then.

Compare that to her achieving financial independence in month 138… before age 52… 18 years earlier… if she did the Nomad™ strategy as described in Episode 1.

That’s a big difference.

We assumed she continued working at her accounting job until she reaches financial independence in both those cases.

What if… in the Scenario where she was investing in stocks… she just stopped working at age 65? How does that look?

In that case, she’d be withdrawing money from her investments to live on starting at age 65. So, her stock market investments would not be growing as fast as if she was still living on her job income between age 65 and 70.

If she stopped working at age 65, she’d technically meet the definition of financial independence by month 473… that’s just a little bit shy of Andrea

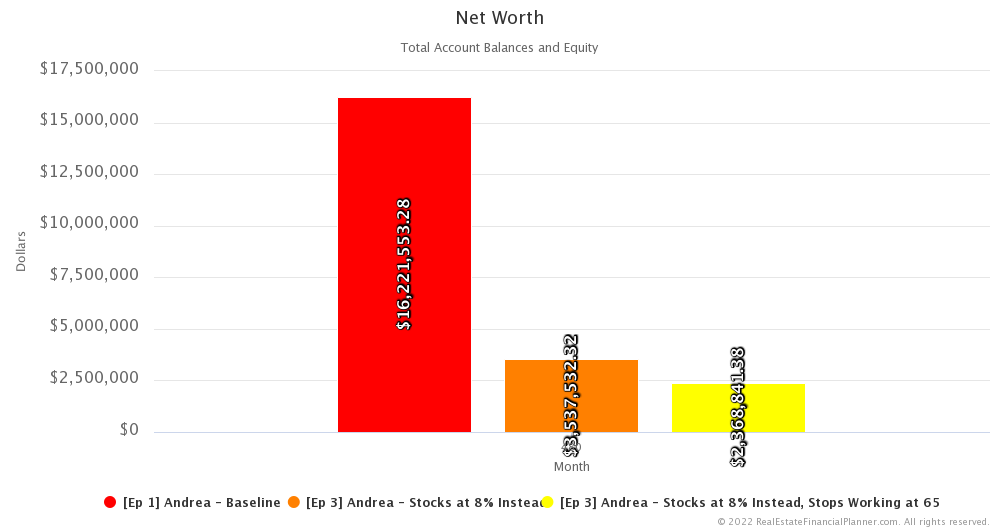

Net Worth

What about net worth? What does her net worth look like after 40 years?

It turns out that in the baseline Scenario from Episode 1, Andrea

If she invests in stocks earning 8% per year and waits until she achieves financial independence… at almost age 80… before stopping working, she has a Net Worth of about $3.5 million.

If she invests in stock and stops working at age 65… even though she technically does not meet the definition of having achieved financial independence… she’s about 64% of the way to being financial independent… she would have a Net Worth of just under $2.4 million.

So, she goes from $16 million net worth doing the full Nomad™ strategy when she stops working in just under 12 years to having a net worth of just under $2.4 million when working for 25 years… 13 years more than she does when Nomading™.

Now, those numbers are inflated dollars. In today’s dollars, doing the Nomad™ strategy is like having just under $5 million in today’s dollars. Investing in stocks and working until she’s almost 80 is just over $1 million in net worth. Investing in stocks and stopping work at 65 is just over $700K in net worth.

In all 3 cases, we assumed she maintained a $40,000 per year standard of living. Of course, we’re adjusting for inflation but it feels like $40,000 per year in today’s dollars.

The fact that she would end up with $16 million in net worth at age 80 doing Nomad™ really means she could have increased her standard of living up from the $40,000 per year.

Not sure I’d suggest she increase her standard of living up too much higher with either of the Scenarios where she was investing in stocks because it is possible that she could live well beyond 80 years old.

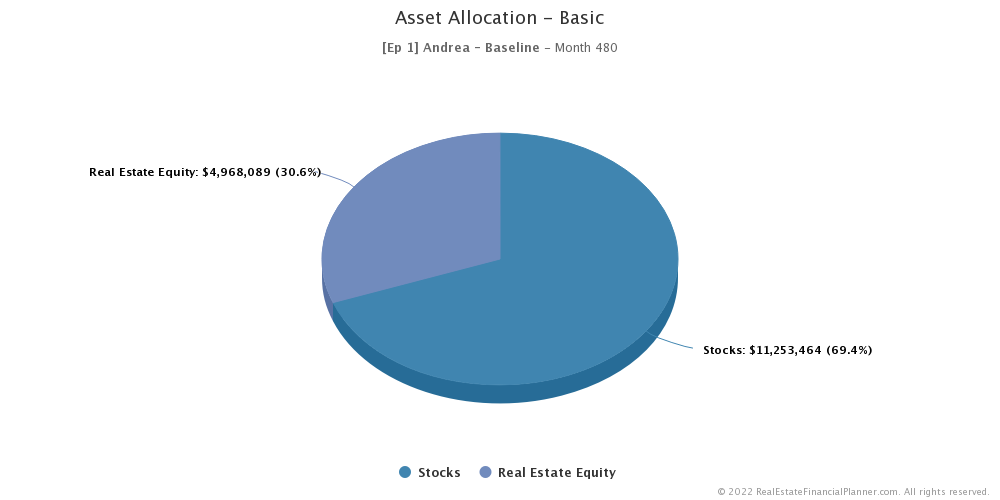

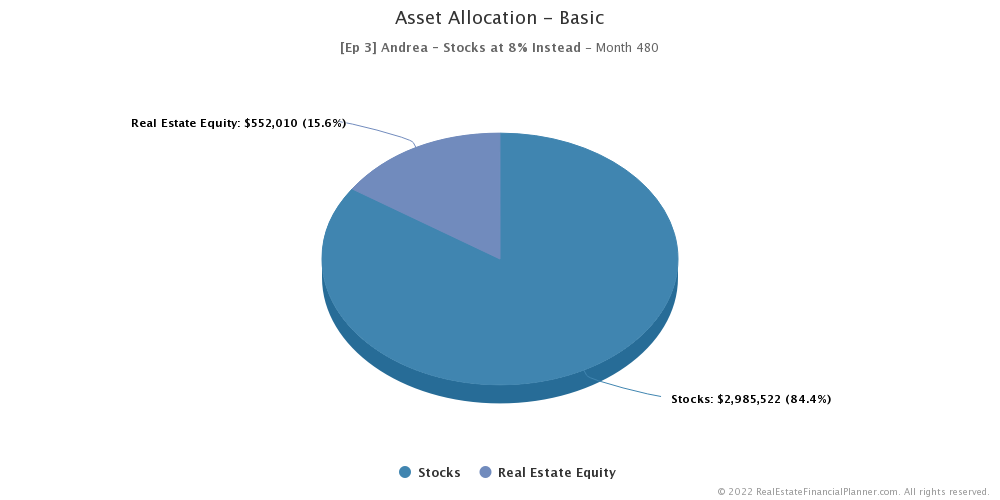

Account Balances

Net worth is made up of equity in her properties and money invested in her accounts.

In the baseline Scenario from Episode 1, she had about 30.6% of her net worth in real estate equity and about 69.4% in stocks at the end of 40 years.

When she invests in stocks and just has the property she is living in, about 15.6% is in real estate equity and the remaining 84.4% is in stocks at the end of 40 years.

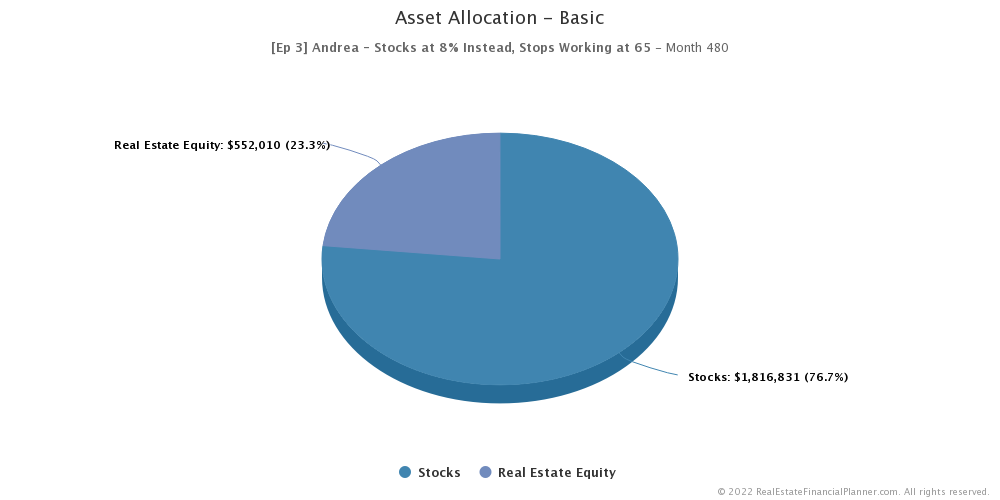

When she stops working at age 65, then by the time she turns 80 she has about 23.3% in real estate equity and 76.7% in stocks.

In a future episode we will discuss the advanced asset allocation ideas that include Bond-Like Real Estate Equity™ and True Net Equity™ after all the expenses to access it.

But for now, I want to discuss a couple more ideas before we finish up this episode.

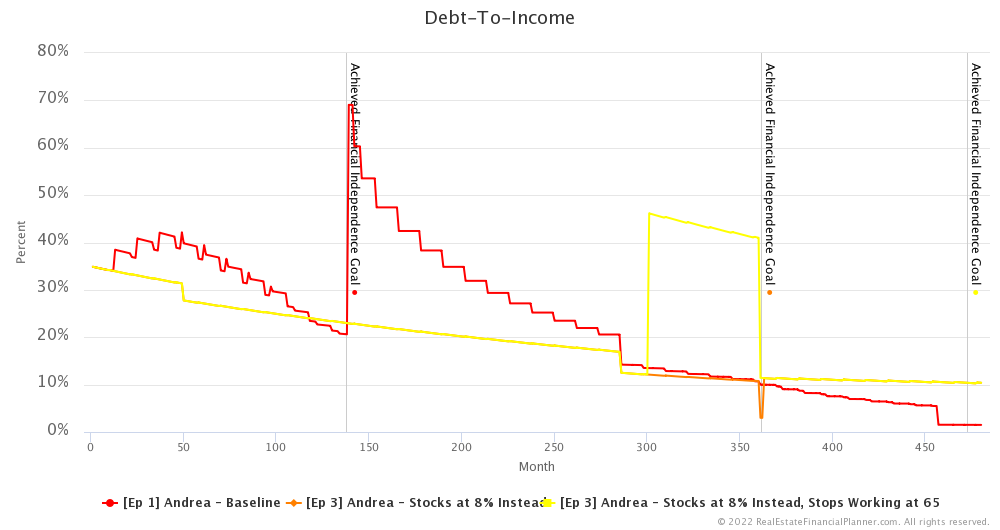

Debt-To-Income

First, let’s compare how Debt-To-Income works when she is investing in stocks with only the property she is living in.

When she buys her first property her Debt-To-Income is the same in all three Scenarios.

However, when she decides to not buy more properties, her Debt-To-Income slowly declines over time as her income increases with inflation and the payment on her loan remains fixed. We see a small bump down when private mortgage insurance drops off just after year 4.

Of course, when she stops working her income changes and that impacts Debt-To-Income in all three Scenarios.

In her baseline Scenario from Episode 1, with each new property she buys her income goes up from the rent she is receiving on the property she is moving out of but her debt increases with the new property she is buying to move into. So, her Debt-To-Income is higher when she is investing in rental properties.

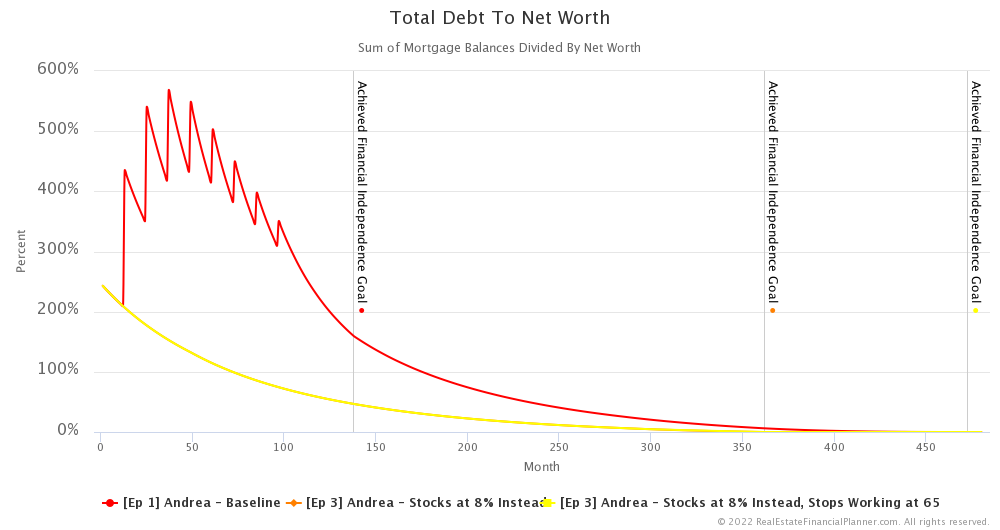

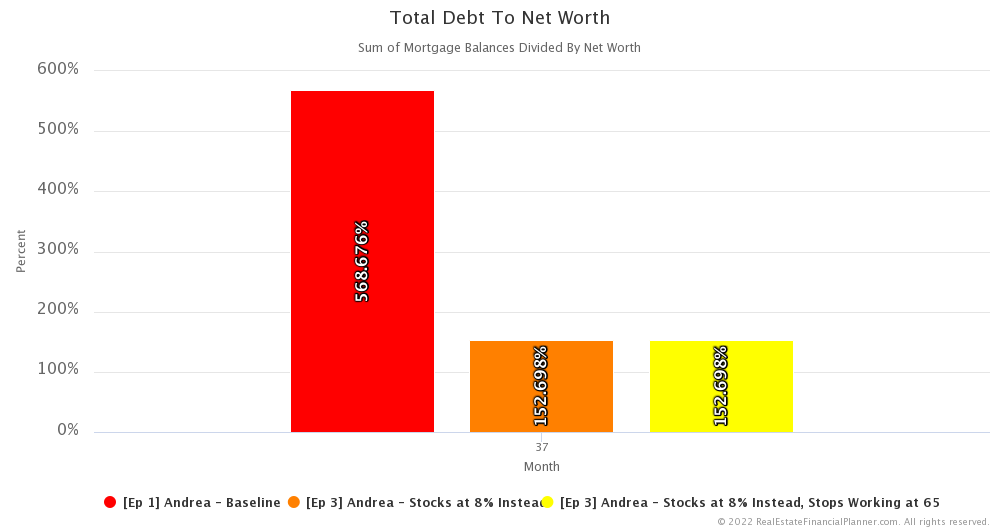

Total Debt To Net Worth

This leads right into my next topic… her total debt compared to her net worth. This is one way to measure risk.

It is true that she has a lower net worth when she invests in stocks, but she also has a much lower debt load by only purchasing one property versus the 1 per year in her baseline Nomad™ Scenario from Episode 1.

So, which wins out? Does she have more risk by having a lower net worth but also lower debt load or does she have more risk with a higher net worth and a much higher debt load?

It is far riskier… in terms of Total Debt To Net Worth for her to do the Nomad™ strategy.

In fact, at its peak… around month 37 when she would be buying her 4th property… it is about 3.7 times as risky… 152% versus 568%… to do the Nomad™ strategy instead of investing in stocks. Debt adds some risk and Total Debt To Net Worth literally measures this type of risk.

It takes almost 10 years to get to the point where the risk of doing the Nomad™ strategy returns to the high point of the risk… when she buys her first property… when she is investing in stocks.

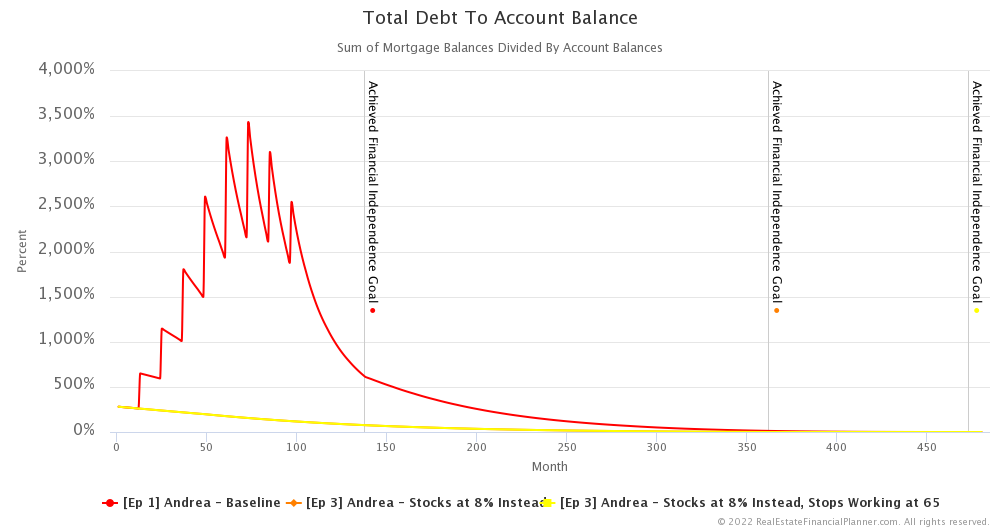

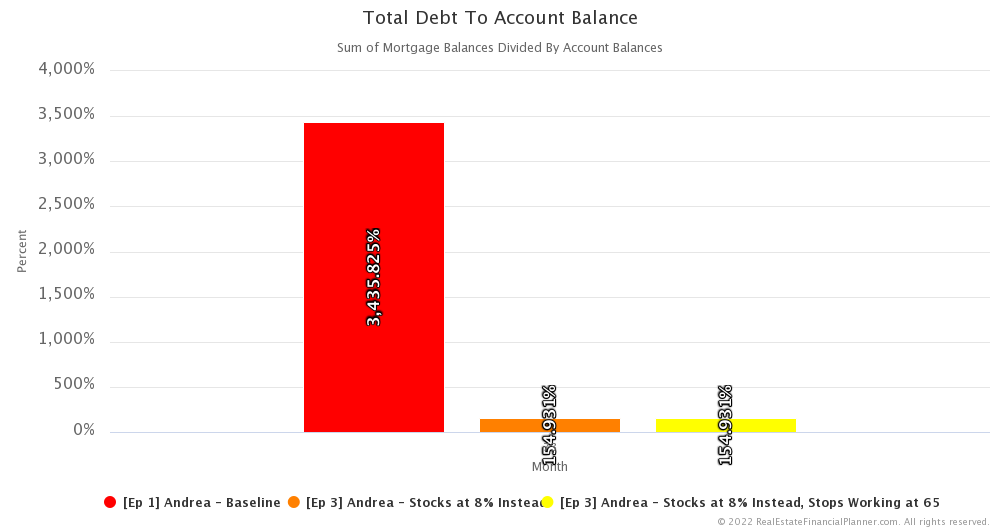

Total Debt To Account Balance

A similar, but slightly different way to measure risk is to measure her debt load compared to her liquid net worth… or her account balances.

When we measure that, her high point for risk from her baseline Scenario in Episode 1 is when she buys her 7th property.

At that point… the riskiest point… doing the Nomad™ strategy is 22 times as risky as investing in stocks.

It takes about 16 years doing the Nomad™ strategy to return to her highest risk point… when she buys her first property… when she is investing in stocks.

When it comes to measuring risk using Total Debt to Net Worth and Total Debt to Account Balance… investing in stocks is a far less risky strategy because with the Nomad™ strategy she is taking on a large amount of real estate debt with the 5% down mortgages.

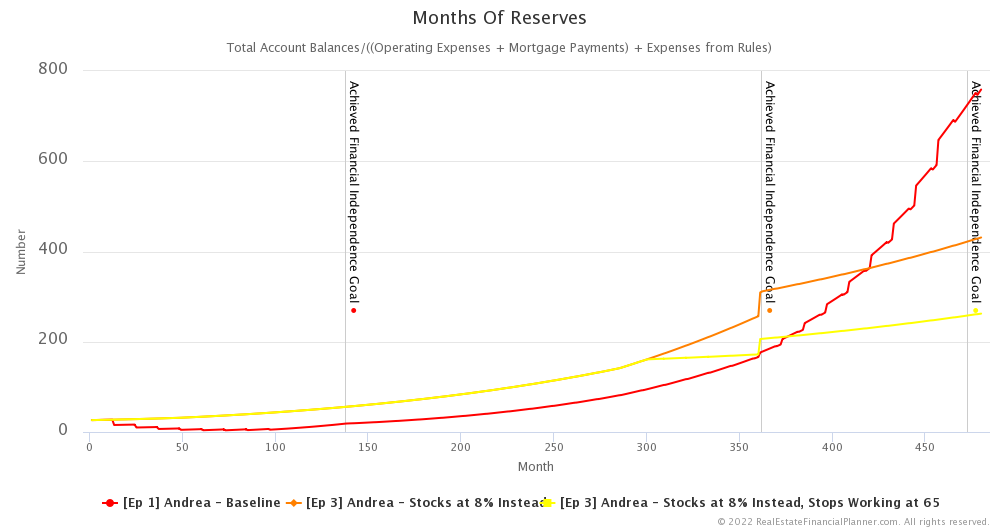

Reserves

Finally, let’s touch on reserves.

Investing in stocks means the amount she needs for a single month of reserves is lower. That’s because she only needs to replace her personal expenses including the mortgage on a single property that she is living in.

Compare that to the baseline Scenario doing Nomad™ from Episode 1 and she needs her personal reserves including the property she is living in PLUS all the reserves for her rental properties.

And, from her baseline Scenario she continues to spend the money she had from the divorce on down payments.

Combine needing more money in reserves for the rental properties and she is spending the money she does have on down payments to continue to acquire properties… it is no wonder that she has a much lower number of months of reserves when doing the Nomad™ strategy in this case compared to investing in stocks.

And, this is true for quite a period of time… in fact it is not until about 30 years from now that the number of months of reserves she has while Nomading™ passes the number of months of reserves she has investing in stocks.

But, the thing to point out is that eventually… although a long time in the future… eventually it does swap and investing in real estate becomes less risky… as measured by the number of months of reserves she has to cover all her expenses.

Conclusion

And that concludes Episode 3 of the Real Estate Financial Planner™ Podcast about Andrea

To summarize… Nomading™ has Andrea Andrea

However, it does come with some added risk… especially when we measure risk as it relates to her debt load. And, that makes sense… Nomading™ has her taking on a very large amount of mortgage debt whereas investing in stocks and buying just a single property to live in… has her taking only a moderate amount of debt to acquire the property to live in.

Next Episode

In general… an appeal of investing in stocks is that it often requires less active oversight and management than investing in real estate. In episodes 1 and 2 Andrea Andrea

Also, in the real world, the stock market doesn’t get 8% per year every year like clockwork. Sometimes you have good years and sometimes you have not so good years. So… be sure to check out the Advanced Real Estate Financial Planner™ Podcast to see how having variable property appreciation rates and rent appreciation rates, variable mortgage interest rates, variable inflation rate and… most importantly for this episode… variable stock market rates of return… impacts Andrea

I hope you have enjoyed this Episode about Andrea

Get unprecedented insight into how Andrea Scenarios.

Inside the Numbers

Don’t like the assumptions I used. Sometimes I don’t like them either. But, it is easy to see exactly what I used for all my assumptions and to change any that you don’t like. Use the copy buttons below to pick one of the three Scenarios Scenario

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 1 Andrea - Baseline with 2  Accounts, 1

Accounts, 1  Property, and 3

Property, and 3  Rules.

Rules.

Or, read the detailed, computer-generated, narrated  Blueprint™

Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 3 Andrea - Stocks at 8% Instead with 2 Accounts, 1 Property, and 3 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Login to copy this Scenario. New? Register For Free

Scenario into my Real Estate Financial Planner™ Software

Ep 3 Andrea - Stocks at 8% Instead, Stops Working at 65 with 2 Accounts, 1 Property, and 4 Rules.

Or, read the detailed, computer-generated, narrated Blueprint™

Learn why we used the assumptions we did and how to change any of the assumptions by going “Inside the Numbers” with the video walk through below of how we setup the Scenarios

Podcast Episodes

The following are the podcast episodes for variations of Andrea’s story.

More posts: Andrea Episode