One of the more common questions we get from real estate investors is Should I refinance my rental property?.

It is right up there with Should I Sell My Rental Property?. However, the math for the decision making process is a little bit different.

When considering selling you often look at your True Net Equity™ and the return you’re currently receiving on that equity. Then, you know what return you’d need to get on the proceeds from the sale (aka your True Net Equity™) with what you’re going to do with that money.

When considering the question of refinancing, there are a few different variations:

- Rate and term refinance to eliminate interest rate or balloon risk

- Rate and term refinance to lower your monthly payment

- Cash out refinance

- Where your new payment is lower

- Where your new payment is higher

Let’s look at each one.

Rate and Term Refinances

A Rate and Term refinance is one where you are refinancing to change the mortgage interest rate and/or the term of the loan.

Rate and Term Refinance to Eliminate Interest Rate or Balloon Risk

If you have a variable/adjustable rate mortgage or a balloon on your mortgage you may be considering a refinance to eliminate those risks.

In these cases, the reason to refi has less to do with the math of improving your cash flow or pulling out cash to reinvest elsewhere and more to do with eliminating risks.

If you extend your loan term with the refinance (ie 24 years left and refinance to it a new 30 year loan), you may be reducing your monthly payment. If you shorten your loan term (ie you were previously on a 30 year amortization schedule and you decide to switch to a 15 year term), you may be increasing your monthly payment.

There may be cases where the current interest rates are so much better than what you have where your payment actually improves even if you shorten your term. Or, where interest rates are so much worse than what you currently have where even extending the term results in higher monthly payments.

Of course, you can choose to buy down interest rates to improve your monthly payment and therefore cash flow.

Rate and Term Refinance to Lower Monthly Payment

Cash Out Refinances

What if you plan to refinance, voluntarily increase the amount you borrow to receive cash back at the refinance closing? That’s a cash out refinance.

There are two flavors of cash out refinances:

- Where your new payment is lower

- Where your new payment is higher

Lower New Payment

There may be times where between a decline in interest rates and/or an extension of the term of the loan where your new payment—even when pulling cash out—where your new monthly payment will be lower than your previous monthly payment.

In these cases, some real estate investors will look at the “cost” to refinance as a percentage of the cash received to get a feeling for the cost to access that money.

For example, let’s assume you’re considering a cash out refinance. You can pull net $100,000 out when you do the refinance. But, the refinance will cost you $3,000.

You just paid $3,000 to get access to $100,000 in cash. Your payment will be the same or better by doing this.

That’s 3% cost of the money you accessed. You did not need to come out of pocket for the $3,000. You were really going to receive $103,000 but the lender took $3,000 of that to pay for the cost to refinance. So, really, it shows up as part of your mortgage balance. That means you have $3,000 less in equity (really $103,000 less but you also got $100,000 in cash with the refi). That means your net worth decreased by $3,000.

If you’re going to take that $100,000 and do something valuable with it (like use it to fund your lifestyle if that’s a priority for you or to re-invest if that’s a priority for you).

For me, a 3% cost to get at money to invest would be an acceptable cost in this example. But, what if it was a different situation? What if I was only going to receive $10,000 by doing the cash out refinance? It is still improving my monthly payment, so there is a benefit to doing it.

However, now the $3,000 cost to refinance means that I just spent about 30% of the $10,000 to get access to that $10,000. That seems expensive to me. But it does also improve my cash flow.

Since interest rates for cash out refinances are sometimes higher than the interest rates for rate and term refinances, I’d be looking closer at the difference between those two options. With that being said, sometimes that extra $10,000… even at a high cost… to bolster reserves might still be a worthwhile trade-off for SOME real estate investors. If you access that same money cheaper elsewhere, that might be a better option.

Modeling this in the Real Estate Financial Planner™ software will allow you to look at the whole picture and see the impact to cash flow, net worth, time to reach financial independence, risk and much, much more.

Higher New Payment

In most cases when you are increasing the amount you are borrowing with a cash out refinance, your monthly payment will increase.

Sometimes this is slightly mitigated by a reduction in your interest rate from your current mortgage.

There are times when you need the cash and the increase in payment doesn’t matter. For example, you need to pay for an emergency medical treatment. In those cases you’re choosing to finance what it is you’re using the money for with long-term, relatively low interest real estate debt. Any reduced cash flow caused by your cash out refinance is the cost of financing whatever it was that you NEEDED the money for.

However, there are times when you are strategically considering increasing your leverage (with a cash out refinance) to invest that money elsewhere. In these cases, you need to consider what the cost to access that new money is and the return you’re likely to see on the money you’re investing.

In my opinion, you need to account for both.

To calculate the cost of your refinance, first calculate the difference in monthly payments from the previous mortgage to the new payment with the refinanced loan. It will be a negative number. Multiply this by 12 to get a yearly amount of the difference between the two loan payments. If you divide this annual difference by the net amount of cash you received with the refinance, you can see the “short-term” cost having access to this extra money.

What you decide to invest your cash out proceeds in will need to have a return that exceeds this extra monthly payment cost.

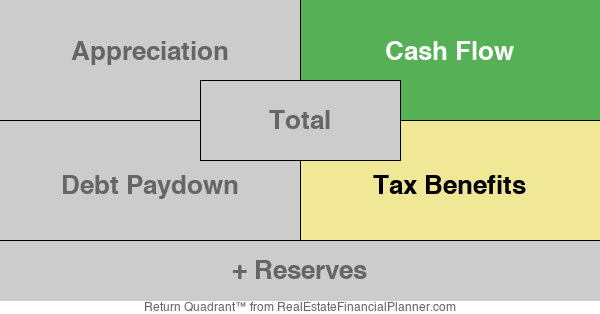

And, in my opinion, ideally the return in the Cash Flow section (shown below) of the Return Quadrants™ exceeds the extra cost of the loan. These are purists that want the new cash flow from their new investments to fully cover the cost to access the cash to purchase the new investments.

One step below the purists, some real estate investors will also consider the cash flow and Cash Flow from Depreciation™ (what we call True Cash Flow™) covering the cost of the cash out refinance to be acceptable.

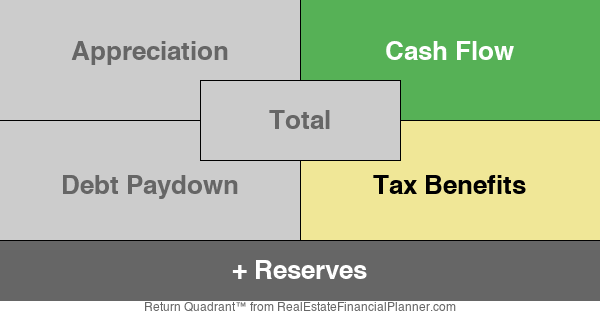

Fewer folks still might even consider the cash flow from reserves in this as well.

However, for a even smaller number of folks, the combined returns from all sections of the Return Quadrants™ will be so attractive that they would consider the overall returns received by acquiring new assets to outweigh having some negative cash flow or negative True Cash Flow™.

For example, if it costs you -5% (the annual difference in payments/amount of cash out) but the overall return from buying a new rental property with the money is going to exceed 30% per year… even if the True Cash Flow™ could not cover the difference in monthly payments… some real estate investors would sacrifice cash flow (presumably in the short-term) to get that net 25% return.

For astute math folks, yes… we’re NOT taking into account that the payments will eventually end (when the mortgage is paid off) and the payments might be ending at different times. The Real Estate Financial Planner™ software does model this correctly.

If you’re rolling the costs of the refinance into the refinanced loan balance (or less cash back), you are taking into account the cost in the new monthly payment. However, the cost to refinance including buying down your interest rate will reduce your equity and, consequently, your net worth.

Model A Refinance Using the Real Estate Financial Planner Software

To model a refinance:

- Make a copy of the

Scenario

Scenario - Make a copy of the Already Owned

Property

Property - Edit the copy to change the:

- Mortgage interest rate for the property

- New (probably higher… if a cash out refinance) loan balance, and

- New (probably higher… if a cash out refinance) monthly payment

- Add the “refinanced” version of the

- REMEMBER: Change any other

Rules

Rules - If you’re modeling a “cash out refinance” add the amount of cash you received to your

Account

Account - If you’re going to re-invest the cash out refinance proceeds into another investment, be sure to add the purchase of that new investment to your

- Rerun the

Charts

Charts

Refinance Tips

The following is a class I taught about tips when refinancing: