It seems like every week there is a new article about whether it is cheaper to rent than to buy a home. They cite studies that sound impressive. They explain how they compare the cost of rent to the mortgage payment, taxes and insurance payments. They obfuscate the truth by talking in terms of percentage of your income that you use when renting versus buying.

It seems like every week there is a new article about whether it is cheaper to rent than to buy a home. They cite studies that sound impressive. They explain how they compare the cost of rent to the mortgage payment, taxes and insurance payments. They obfuscate the truth by talking in terms of percentage of your income that you use when renting versus buying.

All of it is utter hogwash!

Don’t believe a word of it; it is always cheaper to buy than to rent, regardless of your market, regardless of what percentage of income you’re paying for rent or a mortgage… it doesn’t matter.

The latest Federal Reserve data suggests that the typical net worth of the average renter is estimated to be $5,000 while the net worth of the typical homeowner is pushing $225,000. That’s not a typo.

If you think you’re “saving” money renting, you’re either a fool or haven’t been shown all the math.

Here’s An Extreme Example of Buying Versus Renting

For example, let’s saying buying a home is 50% more expensive than renting a home. In this example, we’ll say you can rent a property for $1,000 a month and that buying a home costs you $1,500 per month with principal, interest, taxes, and insurance.

If it seems like a clear choice to rent versus buy, you should have your eyes checked; it is not.

If you paid $1,000 per month you paid $12,000 to your landlord and got nothing more than a place to live for a year.

If you paid $1,500 per month towards your mortgage, taxes and insurance you got a lot more than just a place to live. A $1,500 payment would cover about a $225,000 property with minimal down, a 5% interest rate over 30 years with $100 for property taxes each month, and $100 for insurance each month.

Property Values Tend To Go Up Over Long Periods of Time

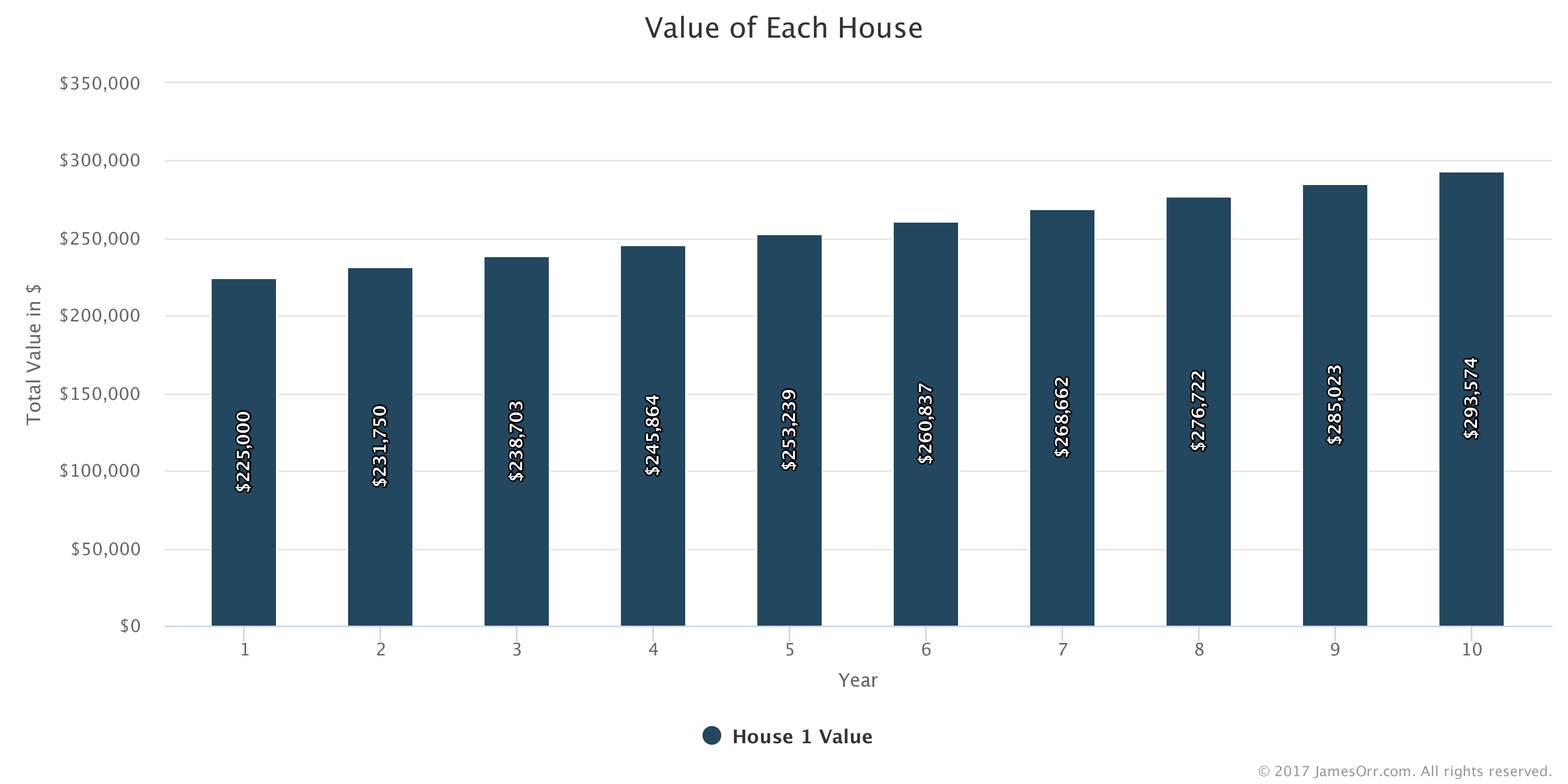

Three economists from Yale studied home appreciation rates spanning a period of over 100 years and showed that real estate values tended to keep pace with inflation. Inflation fluctuates but the long term average is 3%. That means the $225,000 property you’re buying, is likely to go up between $6,750 to $8,807 per year that you live there. Here’s a chart showing what 3% appreciation per year is on a $225,000 property.

That means that the $225,000 property you purchased grows to be worth $293,574 over 10 years.

That’s an increase of $68,574… now you can start to see why the Federal Reserve numbers show the wide discrepancy between the renter’s net worth and the homeowner’s.

You Pay Down Debt on the Property Each Year

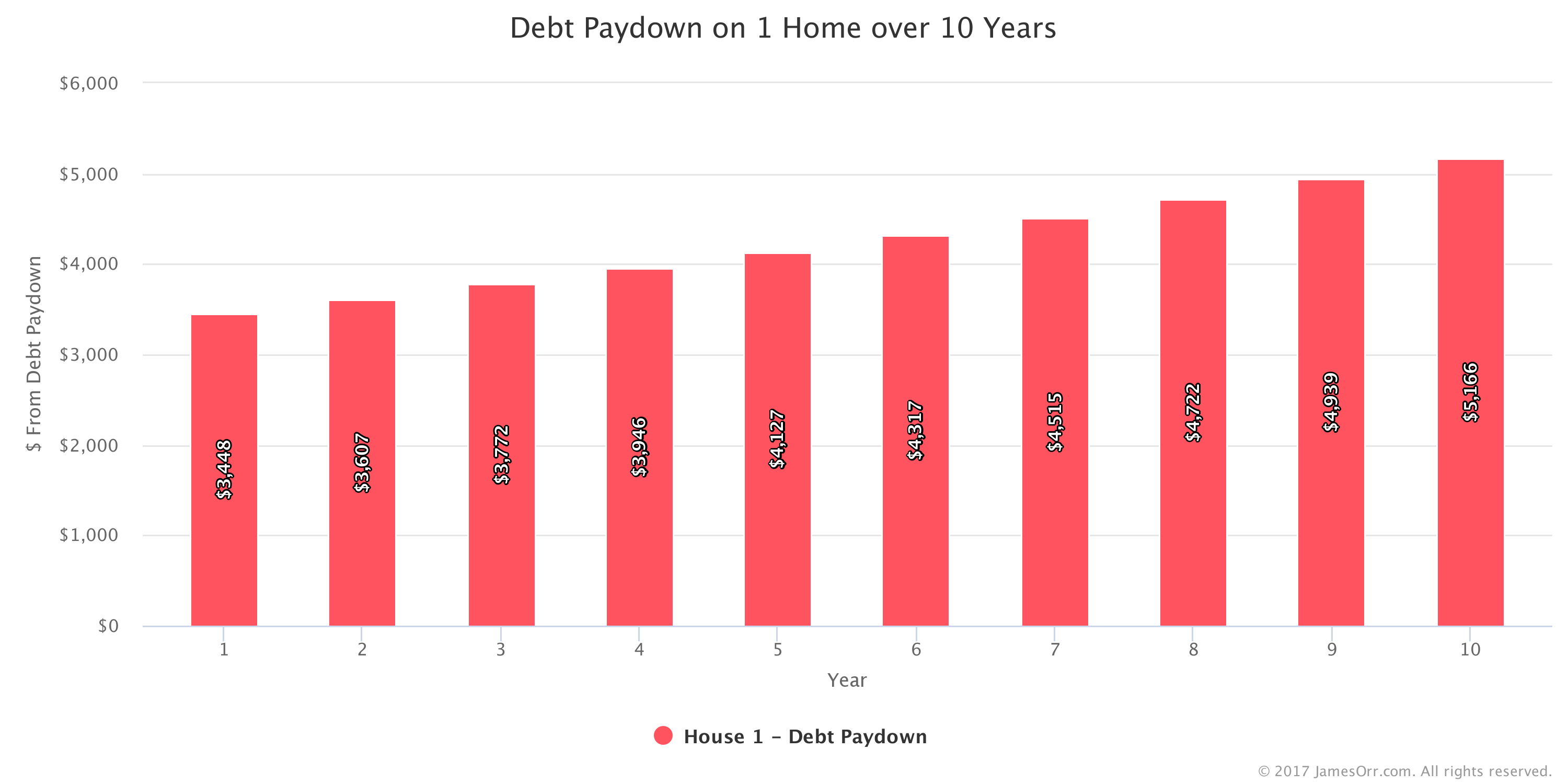

But an increase in property value is not the only difference between renting and owning. You also pay down the mortgage on the property with each monthly payment, and it is not trivial. In fact, it is a good way towards making up the difference between your rent and mortgages, taxes and insurance on your property.

In the first year, you would have paid $500 more per month to buy in our example… that’s $6,000 per year. But with rent you have nothing to show for that. When you have a mortgage, you paid down $3,448 in the first year and by the time you’re at year 10, you’re paying down $5,166 on your mortgage each year.

I like to think of this as a forced savings… or a rebate on your monthly housing payment.

Add the appreciation and the debt pay-down together and you’re more than $10,000 in favor of buying a home than renting. It is never better to rent than to buy.

Plus, You Lock In The Largest Part of Your Monthly Payment

As a landlord, I want to raise rents every year. So, as a renter, you’re seeing rent increase each year.

Not as true as a homeowner… your payment may be $1,500 per month in the first year, but the only parts of the payment that are increasing are the $100 per month in taxes and the $100 per month in insurance. The $1,200 per month mortgage payment stays fixed for 30 years. Go ahead and ask your Landlord if they’ll fix your rent for 30 years… go ahead, I’ll wait…. did they laugh at you? Probably. It doesn’t make sense for them to do it.

And looping back to the $100 for taxes and $100 for insurance per month that does go up… let’s even assume that those go up by 10% per year each… which is not realistic… they’re much more likely to go up at the inflation rate of about 3% per year. But, if they did go up 10% per year each, that means that your total payment would go up by $20 per month in year 2. If it was a more realistic 3%, that means that your total payment with taxes and insurance on a property would go up $6 per month in the first year. Minimal. Rent is much more likely to increase by 3% each time your lease is renewed to keep up with inflation… that means that your $1,000 rent would go up $30 per month.

Each year that you do this the gap between rent and mortgage payment widens in favor of buying a home.

Tax Benefits

One of the things that the news does not really take into account which furthers my point about buying being better than renting are the tax benefits, such as being able to deduct interest on your loan, property taxes and private mortgage insurance (if you have it). Factor those in and it is always a clear win to buy a home.

Qualifying For Buying

Sometimes the news will argue that it is hard to qualify for loans… that’s also nonsense… there are government backed loans like the FHA loan that allows people with past credit challenges buy a home with credit scores as low as 620 easily. You do need a job, but if you’re renting from me you need a job too, so that’s not different at all.

Always Better To Buy, Yes… Always

So, as you can see, even if it costs you 50% more to buy than to rent, you’re still better off buying a property than renting. Anyone who says otherwise is not really doing the math.

And if buying one home is good, buying more than one is probably better. The Nomad strategy shows normal people how to buy a home as an owner occupant, live there for a year, then covert the property to a rental. It generates both wealth and passive income with minimal investment and maximum returns.