When I sit down with clients to run numbers, capital gains taxes are often the biggest blind spot. They know a property has appreciated. They know a sale will produce a large check.

But they rarely understand how much of that check actually belongs to the IRS.

When I was rebuilding my own portfolio after bankruptcy, I learned you cannot judge a property’s performance without understanding what taxes will do to your proceeds. Capital gains taxes shape when you sell, what you sell, how you refinance, how you plan your retirement, and even where you choose to live.

This is the part most investors skip… until it’s too late.

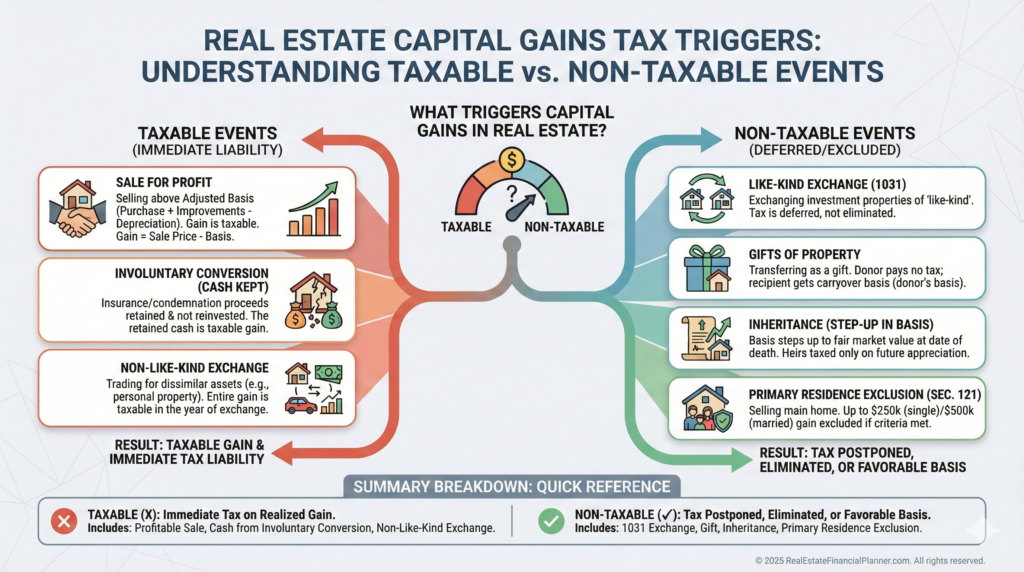

What Really Triggers Capital Gains Taxes

Capital gains taxes appear whenever you dispose of a property for more than your adjusted basis.

Most investors assume: “I sold the property, so I owe taxes.”

But it’s more nuanced.

Inherited properties receive a step-up in basis. Gifts transfer your low basis (and your embedded tax liability) to someone else.

If you misunderstand basis, you misunderstand everything.

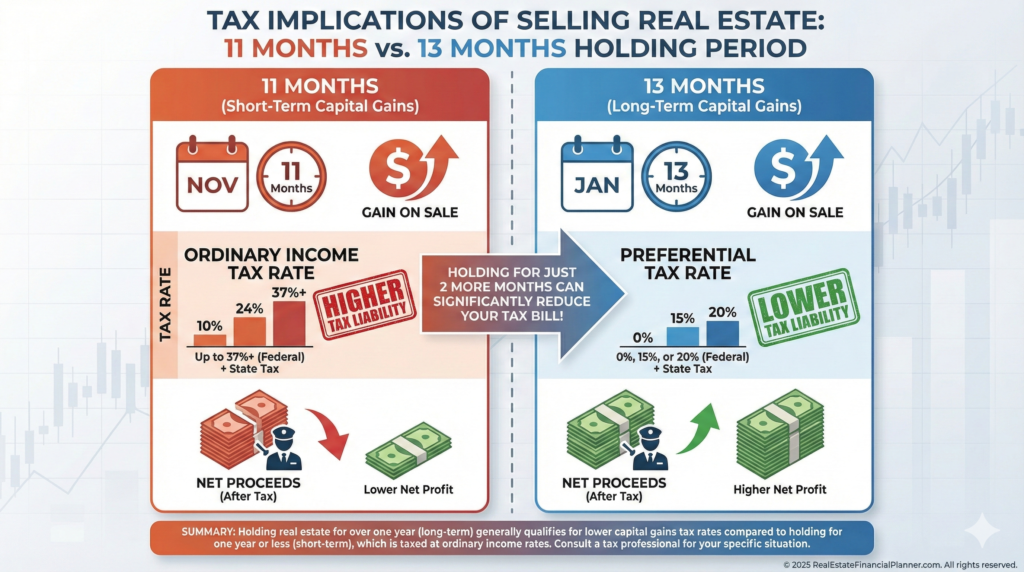

The One-Year Rule That Saves or Costs Tens of Thousands

Short-term capital gains are taxed like ordinary income. Long-term gains receive favorable treatment.

I’ve had clients ready to sell in month eleven. When they see the projected tax bill modeled inside the Real Estate Financial Planner™, they immediately understand why waiting a few weeks could save them five figures.

Your holding period is a tax lever. Use it intentionally.

How Capital Gains Rates Actually Work

Capital gains rates seem simple—0%, 15%, or 20%—but your true rate depends entirely on your income and whether you’re subject to the Net Investment Income Tax.

Sell in a high-income year, and your tax bill skyrockets. Sell in a low-income year, and you might pay nothing.

This is why I help clients plan multi-year disposition strategies instead of one-off sales.

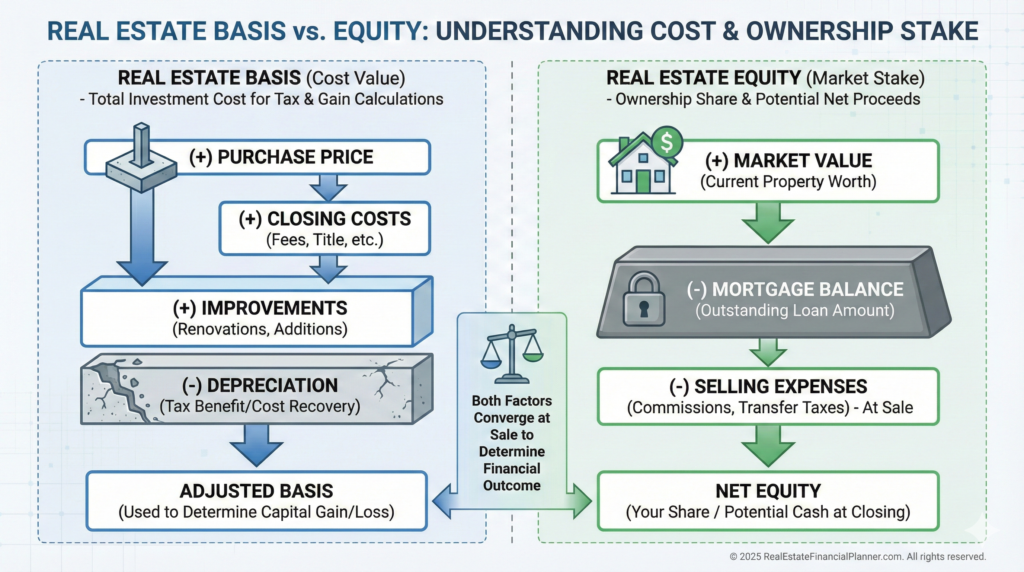

Understanding Basis: Where Most Investors Get Lost

Your basis is not your equity. It’s not your down payment. It’s not your mortgage balance.

Basis equals purchase price, closing costs, capital improvements, and depreciation adjustments.

A missing improvement record or forgotten closing cost can dramatically inflate your tax bill.

Accurate basis tracking is wealth preservation.

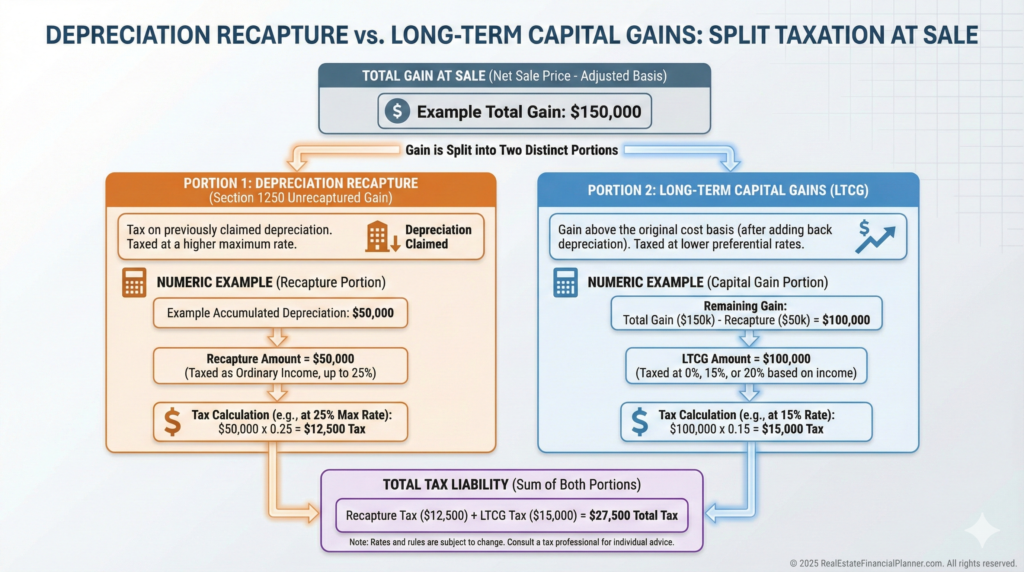

Depreciation Recapture: The Tax Almost Everyone Forgets

Depreciation recapture blindsides more investors than anything else. Every dollar you depreciate increases your future taxable gain.

When I walk clients through a sale, their biggest shock is discovering that their gain isn’t one tax—it’s two.

True Net Equity™ exists only after both taxes are removed. Otherwise, the numbers lie to you.

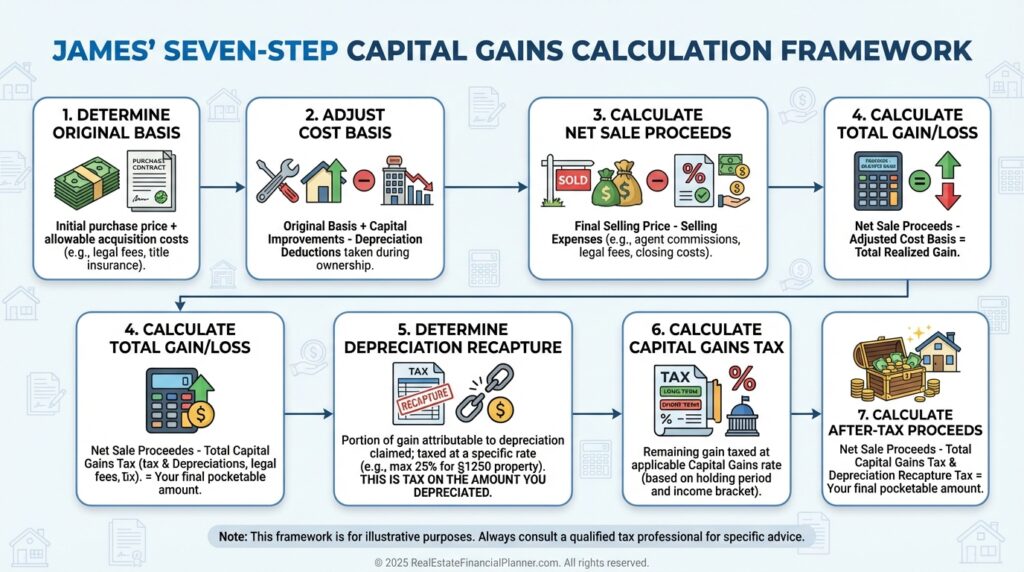

The Calculation Every Investor Should Know

When evaluating a sale, I run clients through the same sequence:

- Your adjusted basis

- Total depreciation taken

- Selling expenses

- Total gain

- Recapture portion

- Long-term portion

- After-tax proceeds

- Return on True Net Equity™ (hold vs sell)

When investors see their after-tax proceeds instead of raw equity, the correct decision almost always becomes clear.

Special Rules Every Investor Should Understand

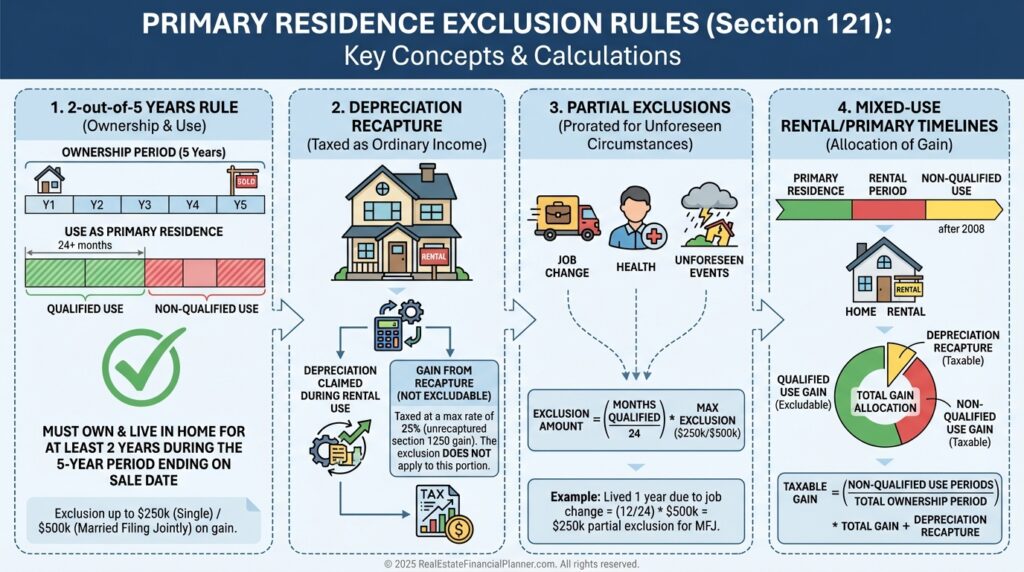

The Primary Residence Exclusion

Live in a property two of the last five years, and you may eliminate up to $500,000 in gains.

Depreciation still must be recaptured, but the remaining gains may be tax-free.

Installment Sales

Useful for spreading income across years and reducing bracket impact.

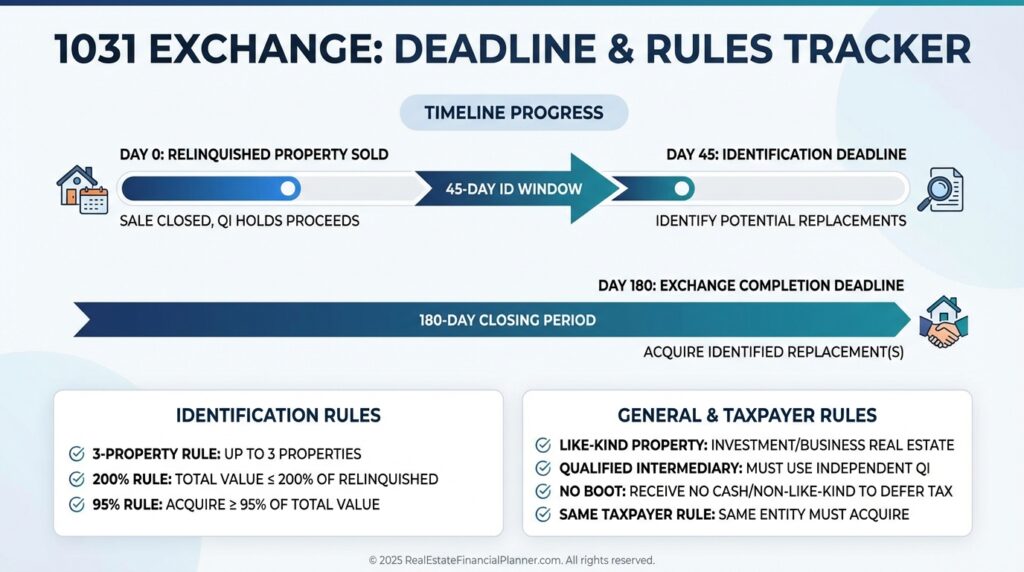

1031 Exchanges

Powerful when used correctly, disastrous when executed sloppily.

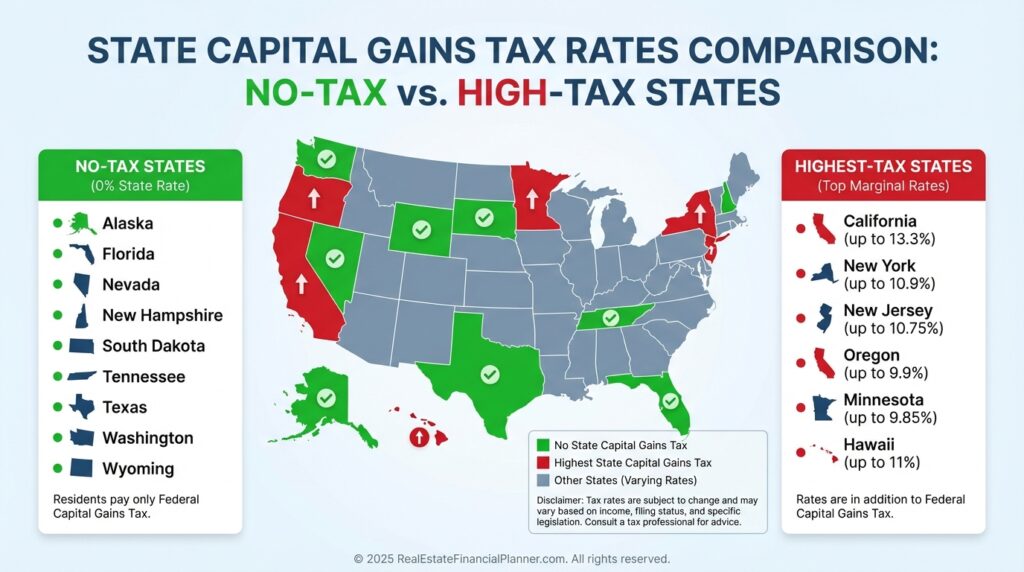

State Taxes: The Silent Multiplier

Some states double your tax bill. Others eliminate it entirely.

Strategic relocation can save six figures.

How Capital Gains Taxes Fit Into Your Bigger Strategy

Raw equity is meaningless. Only True Net Equity™ matters.

A rental with mediocre cash flow may be an exceptional investment once tax consequences of selling are modeled.

- Sometimes the right move is to sell.

- Sometimes the right move is absolutely not to sell.

You only know when you model it.

Common Mistakes That Cost Investors Money

Here are some of the most common mistakes that I’ve made and I’ve seen clients of mine make:

- Forgetting recapture

- Miscalculating basis

- Losing documentation

- Breaking a 1031

- Selling too early

- Ignoring state taxes

- Guessing instead of modeling

In my opinion, I suspect these mistakes destroy more wealth than bad deals.

Now that you now about them, you can avoid making them.

Planning and Documentation

- Pros track basis annually.

- Pros document improvements.

- Pros model disposition scenarios years ahead of time.

- Pros know their tax bill before listing.

Capital gains taxes are something you plan around, not react to.

Adopt this mindset, and your entire investing strategy improves.