Copy Scenario

Copy this new  Scenario to your Real Estate Financial Planner™ software:

Scenario to your Real Estate Financial Planner™ software:

APPR 10 5% Nomads, Work 10 Years Then Sell Properties for Cash Flow

APPR 10 5% Nomads, Work 10 Years Then Sell Properties for Cash Flow

16.87% Effective Income Tax Rate is based on being married earning $60K per year in Fort Collins, Colorado.

The Scenario you want to copy into your Real Estate Financial Planner™ software has the following:

- 2

Accounts (including

Accounts (including  Default Cash Account

Default Cash Account - 1

Properties

Properties - 4

Rules

Rules

Please register for a Forever Free Account or Login to your existing Real Estate Financial Planner™ software to copy this Scenario into your account.

Once it is in your account, you can view detailed  Charts for dozens of variables and edit any of the assumptions for Accounts, Properties, and Rules to run your own what-if Scenarios.

Charts for dozens of variables and edit any of the assumptions for Accounts, Properties, and Rules to run your own what-if Scenarios.

You can change things like:

- Adjust how much money you start with in any Account

- Model variable stock, bond and real estate rates of returns

- Change how many

Properties you buy and when you buy them

Properties you buy and when you buy them - Set your own personalized target monhtly income in retirement to indicate when you reach financial independence

- Model receiving social security payments when you reach a certain age

- See what happens if there is a market crash or correction for your stocks, bonds and/or your real estate

- Tweak price and rent appreciation rates for individual Properties or all your Properties

- Find out what happens if you pay off your mortgages early... with cash flow each month or only when you have enough to pay off the Property in full

- Use equity in

- Model buying more Properties than you need then selling off any extras to pay off the remaining Properties to achieve your own user-defined financial independence number

- Evaluate your own safe withdrawal rate and see how it impacts your investment plan

- And much, much more...

Scenario

- Modeled for 720 months (60 years)

- 16.87% effective income tax rate

- 3% inflation rate

- 4.125% mortgage interest rate

- 4% yearly safe withdrawal rate (SWR)

- $5,000 minimum target monthly income in retirement (MTMIR) in today's dollars

- $20,000 ideal target monthly income in retirement (ITMIR) in today's dollars

Accounts

Summary of assumptions for the Account in this Scenario.

- Account Name: $300K in Savings at 7%

- $300,000 starting account balance

- 7% yearly rate of return (at start)

- Asset Type: Cash

Properties

Summary of assumptions for the Property in this scenario (at the start of the Scenario).

Property Address/Description: Appreciation Nomad

- This

Rules

Rules - This

- This

- Account for down payment, income and expenses for this

- $350,000 property value and purchase price and it goes up at a rate of 3% per year.

- 5% of purchase price for down payment.

- 1% of purchase price in closing costs at time of purchase.

- No seller concessions.

- 3.75% is the mortgage interest rate with a term of 360 month mortgage term.

- Private Mortgage Insurance (PMI) at a rate of 0.71% of the initial loan balance until the loan-to-value drops below 78%.

- $1,905.23 per month in rent but rent increases at a rate of 1% per year.

- 3% of the monthly income is the assumed vacancy rate.

- 10% of the monthly income is the assumed maintenance rate.

- 0.65% of the value of the property each year is the assumed property taxes rate. Based on the initial value of $350,000 that's about $2,275 per year in property taxes at the start and it changes as the property value changes.

- 0.4% of the value of the property each year is the assumed property insurance rate. Based on the initial value of $350,000 that's about $1,400 per year in insurance costs at the start and it changes as the property value changes.

- This is a residential property and 15% of purchase price is considered the value of the land (when doing our depreciation calculation).

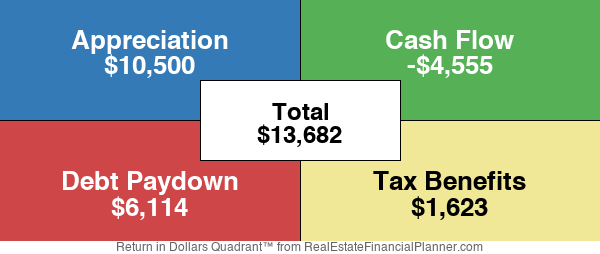

Return in Dollars Quadrant™

The following is the estimated Return in Dollars Quadrant™ for this property based on its original assumptions for the first year.

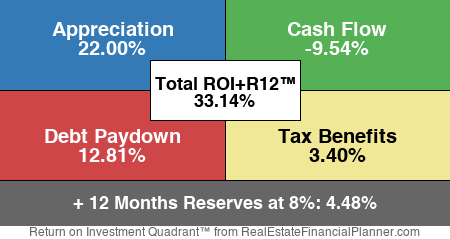

Return On Investment Quadrant™

The following are the estimated Return on Investment Quadrant™ for this property for year 1. We take the returns for each component and divide by the "Total Cost to Close" (down payment, rent ready costs, closing costs - seller concessions). This first one ignores reserves.

How to Calculate

See the steps walking you through how to calculate various metrics for this property.

Walkthrough how to calculate...

- Gross Potential Profit

- Gross Operating Income

- Operating Expenses

- Net Operating Income

- Cap Rate

- Cash Flow

Rules

These are the Rules included with this Scenario.

Paycheck and Personal Expenses - Personal Expenses

- This

- No paycheck, but pulling expenses out of $300K in Savings at 7%.

- Paycheck will be Inflation Adjusted.

- Assuming a tax rate of 16.87% on your paycheck.

- Net paycheck (after taxes) is $0 Inflation Adjusted per month.

- This paycheck will not stop at retirement.

- Personal expenses are $3,657.73 Inflation Adjusted per month.

Paycheck and Personal Expenses - Paycheck From Job

- This

- Depositing paycheck into $300K in Savings at 7% but no personal expenses with this

- Personal expenses will be Inflation Adjusted.

- Gross paycheck is $5,000 Inflation Adjusted.

- Assuming a tax rate of 16.87% on your paycheck.

- Net paycheck (after taxes) is $4,156.50 Inflation Adjusted per month.

- The paycheck will stop when they reach "Financial Independence" (goal of Minimum Target Monthly Income in Retirement achieved).

Buy Property When Account Has Down Payment - Buying 9 Nomad Properties

- This

- This

- Plus at least $10,000 Inflation Adjusted left over in the Account

- This

- This

Sell Rental Properties Based on Account Balance - Sell Properties If I Need Cash When Account Drops Below $10K

- This

- If $300K in Savings at 7% drops below $10,000 Inflation Adjusted then sell RENTAL properties.

- Paying 6% of the sale price as a Real Estate Commission on each sale.

- Paying 1% of the sale price in your share of the Closing Costs on each sale.

- Paying 25% of the Depreciation you've taken (or could have taken) on each sale as a Depreciation Recapture Tax.

- Paying 15% of the net capital gains in Capital Gains tax on each sale.

Significant Events

These are the  Significant Events Scenario.

Significant Events Scenario.

- Month 1 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 13 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 25 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 37 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 49 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 61 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 73 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 85 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 97 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 109 Bought New Dynamic Property Based On Rule Buy Property When Account Has Down Payment

- Month 120 End Income Source

- Month 145 Sold Property Based on Low Account Balance

- Month 176 Sold Property Based on Low Account Balance

- Month 213 Sold Property Based on Low Account Balance

- Month 258 Sold Property Based on Low Account Balance

- Month 314 Sold Property Based on Low Account Balance

- Month 387 Sold Property Based on Low Account Balance

- Month 433 Paid Off Mortgage

- Month 445 Paid Off Mortgage

- Month 457 Paid Off Mortgage

- Month 469 Paid Off Mortgage

- Month 577 Sold Property Based on Low Account Balance