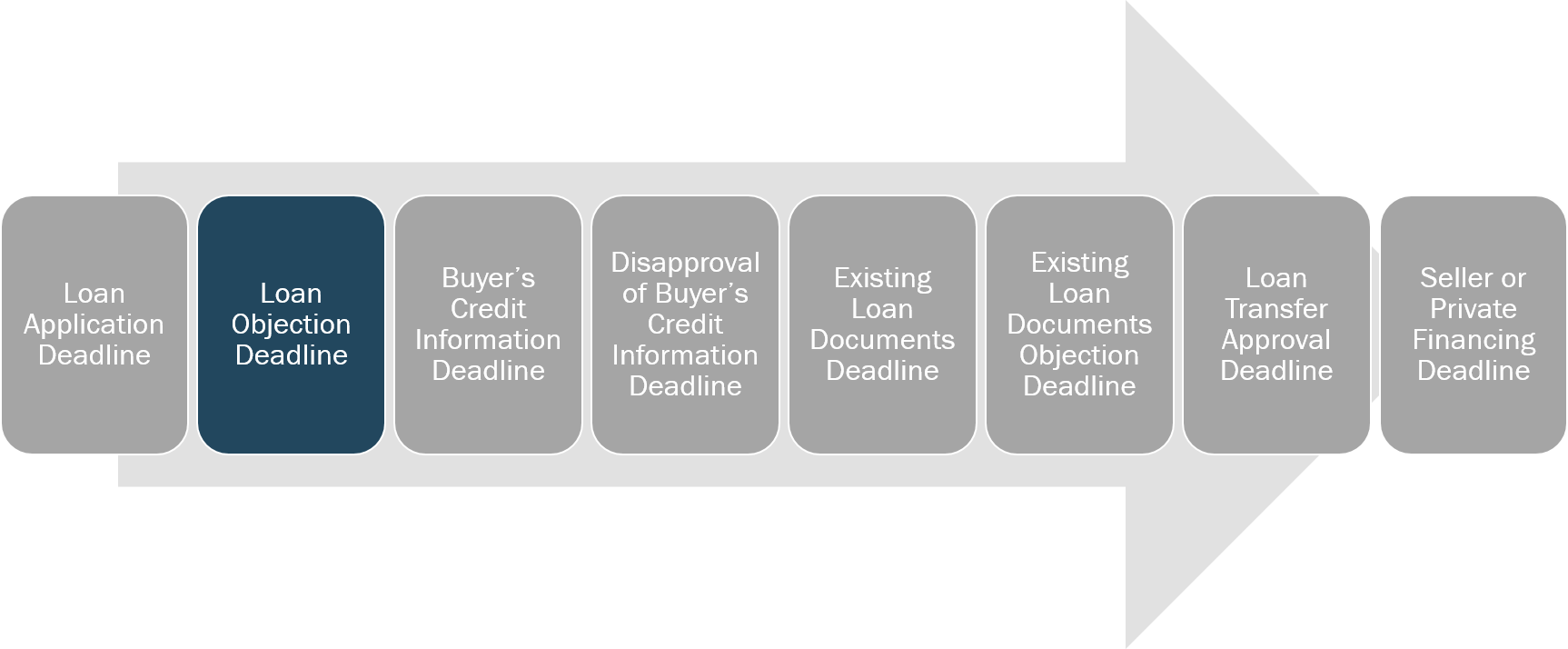

These are the checklists related to Contract Deadline: Loan Objection Deadline.

This deadline relates to your right to be able to terminate if you're not able to get an acceptable loan.

https://RealEstateFinancialPlanner.com/loan-objection-deadline/

When you click on the task, you can also see the tags that task is filed under. You can also click on the tag to see other tasks with that tag.

- Complete "Loan Objection Deadline" checklist

Complete the "Loan Objection Deadline" checklist:

https://RealEstateFinancialPlanner.com/loan-objection-deadline/

Contract Deadline: Loan Objection DeadlineContract To Close: Loan and CreditFinancingUltimate Nomad ChecklistWeek 10Week 11Week 12Week 13

- Provide Lender all financial documents

Your Lender will undoubtedly want a plethora of financial documents.

Mark this task complete once you've provided them all to your Lender.

Contract Deadline: Loan Objection DeadlineFinancingUltimate Nomad ChecklistWeek 9

- Consider ARM versus fixed-rate mortgages

In all but a small number of cases, we recommend fixed-rate 30 year mortgages for Nomads.

However, there are two situations we'd consider ARMs.

First, if you're buying the property and are 100% positive you're going to be putting a Tenant-Buyer in the property and you will be out of the property before the mortgage will adjust, then you can consider using an ARM.

Second, if you're buying the property with partners and the only loan you can get with the partnership is an ARM then you can also consider an ARM. However, in this case you probably should be putting a Tenant-Buyer in the property so it probably still falls under the first reason above.

Interest rates for ARMs (Adjustable Rate Mortgages) tend to be a little lower than the interest rates on fixed-rate 30 year mortgages. But the ARM interest rates can adjust over time causing much higher monthly payments and significant negative cash flow after the interest rate adjusts. This adds additional risk that you could have opted not to take on.

Mark this task as complete if you have decided to get fixed-rate mortgage or an ARM.

Analyzing DealsCash FlowContract Deadline: Loan Objection DeadlineFinancingNet Operating IncomeOptionalTenant-BuyersUltimate Nomad ChecklistWeek 10

- Discuss monthly PMI versus up-front PMI with Lender

Often for Nomads it is better to pay a one-time up front PMI (Private Mortgage Insurance) payment instead of monthly PMI on their loans.

This may mean coming to Closing with a little more cash.

Sometimes it means voluntarily raising your interest rate with your Lender to get a credit to pay for some or all of the up-front PMI.

Discuss these two scenarios with your Lender to see which one makes more sense to you.

Mark this task complete once you've discussed this with your Lender and decided which you'll pick.

Analyzing DealsCash FlowContract Deadline: Loan Objection DeadlineFinancingInterest RateNet Operating IncomeOptionalPrivate Mortgage InsuranceUltimate Nomad ChecklistWeek 10

- Consider buying down interest rate

Talk to your Lender to see if buying down your interest rate makes sense in your specific situation.

Sometimes, especially if you have extra cash and you plan to hold the property for a long time, it makes sense to pay additional points to get a lower interest rate.

Mark this task complete once you've talked to your Lender about these options, analyzed them yourself and decided to buy down your interest rate or not.

Analyzing DealsCash FlowContract Deadline: Loan Objection DeadlineFinancingInterest RateNet Operating IncomeOptionalUltimate Nomad ChecklistWeek 10

- Consider increasing down payment

Sometimes if you have extra cash for down payment it might make sense to increase down payment.

We often consider this as an alternative to to paying up-front PMI or buying down the interest rate. If we're putting less than 20% down, one way to lower our monthly payment is to put more down to get rid of PMI instead of paying the PMI up-front.

Mark this task as complete when you've talked to your Lender about using a larger down payment and decided whether you will or not.

Analyzing DealsCash FlowContract Deadline: Loan Objection DeadlineDown PaymentFinancingInterest RateNet Operating IncomeOptionalUltimate Nomad ChecklistWeek 10